Climate Risks Series, Part 3: Aloha v AIG - Liability Cover for Reckless Environmental Harm

Aloha v AIG - Liability Cover for Reckless Environmental Harm

Increasing numbers of claims are proceeding around the world alleging that the public were misled about the risks associated with climate change, resulting from fossil fuels and greenhouse gas (“GHG”) emissions.

A recent decision in the Supreme Court of Hawaii, Aloha Petroleum Ltd v National Union Fire Insurance Co. of Pittsburgh and American Home Insurance Co. [2024], held that an “occurrence” in this context included the consequences of reckless conduct, and GHG emissions were a “pollutant” for purposes of a pollution exclusion under a commercial general liability policy.

Background

The Appellant, Aloha Petroleum Ltd (“Aloha”), was insured with two subsidiaries of AIG under a series of liability policies, in respect of its business as one of the largest petrol suppliers and convenience store operators in Hawaii.

The counties of Honolulu and Maui sued several fossil fuel companies, including Aloha, claiming that the defendants knew of the effects of climate change and had a duty to warn the public about the dangers of their products. It was alleged that the defendants acted recklessly by promoting climate denial, increasing the use of fossil fuels and emitting GHGs, causing erosion, damage to water infrastructure and increased risks of flooding, extreme heat and storms.

Aloha sought indemnity under the policies and AIG refused to defend the underlying claims, alleging that the harm caused by GHGs was foreseeable and therefore not “accidental”; and alternatively, seeking to rely upon an exclusion to cover for losses arising from pollution.

Aloha issued proceedings seeking a declaration that the policies would respond, and the District Court of Hawaii referred the following questions to the Supreme Court, to assist with determining the parties’ motions for summary judgment:

- Does an “accident” include recklessness, for purposes of the policy definition of “occurrence”?

- Are greenhouse gases “pollutants” within the meaning of the pollution exclusion?

Policy Wording

The policies provided occurrence-based coverage, with two different definitions of “occurrence” for the relevant periods:

- “an accident, including continuous or repeated exposure to substantially the same general harmful conditions”, or

- “an accident, including continuous or repeated exposure to conditions, which results in bodily injury or property damage neither expected nor intended from the standpoint of the insured”

The pollution exclusion clauses varied across the policies, but the differences were immaterial for purposes of the issues before the Supreme Court.

The 2004-2010 policy excluded cover for:

“Bodily injury” or “property damage” which would not have occurred in whole or part but for the actual, alleged, or threatened discharge, dispersal, seepage, migration, release or escape of “pollutants” at any time.

. . . .

“Pollutants” [mean] “any solid, liquid, gaseous or thermal irritant or contaminant, including smoke, vapor, soot, fumes, acids, alkalis, chemicals and waste.”

Is Reckless Conduct Accidental?

Aloha argued that it was entitled to indemnity, as the allegations of recklessness were sufficient to establish an “accident” and therefore an “occurrence” under the policies. Aloha relied on Tri-S Corp v Western World Ins. Co. (2006), which held - in the context of unintentional personal injury resulting from proximity to high voltage power lines - that reckless conduct is accidental, unless intended to cause harm, or expected to with practical certainty.

AIG claimed that Aloha understood the climate science, and the environmental damage was intentional, not fortuitous. It relied on AIG Hawaii Ins. Co. v Caraang (1993), which held - in the context of torts involving obvious physical violence - that an “occurrence” requires an injury which is not the expected or reasonably foreseeable result of the insured’s own intentional acts or omissions.

The Supreme Court agreed with Aloha, ruling that:

“when an insured perceives a risk of harm, its conduct is an ‘accident’ unless it intended to cause harm or expected harm with practical certainty … interpreting an ‘accident’ to include reckless conduct honors the principle of fortuity. The reckless insured, by definition, takes risk.”

Are GHGs “Pollutants”?

Aloha argued that GHGs are not pollutants, because they are not “irritants” (applicable in the context of personal injury, not property damage) or “contaminants”. The drafting history was said to indicate that the exclusion should be limited to clean-up costs for traditional pollution caused by hazardous waste from the insured’s operations, not liability resulting from its finished products.

The Supreme Court held that a “contaminant”, and therefore “pollutant” for purposes of the exclusion, is determined by whether damage is caused by its presence in the environment. Although a single molecule of carbon dioxide would not be viewed as pollution, a fact-specific analysis is required, and the Supreme Court was satisfied that Aloha’s gasoline production is causing harmful climate change. This approach was supported by the regulation of GHG emissions in Hawaii and the federal Clean Air Act.

Not all of the policies contained a pollution exclusion clause, however, and the question of whether AIG is required to indemnify Aloha for that policy period (covering 1986 to 1987) will now be considered by the District Court.

Impact On Policyholders

The finding that reckless conduct is covered by liability policies in the context of climate harms is highly significant and will be welcomed by energy companies.

While the issues are yet to be fully explored in European jurisdictions, it is interesting to compare the UK Supreme Court decision in Burnett v Hanover [2021], where merely reckless conduct was insufficient to engage a ‘deliberate acts’ exclusion in a public liability policy; and the recent decision in Delos Shipping v Allianz [2024], confirming that a defence based on lack of fortuity requires the insurer to establish that consequences of the insured’s actions were inevitable, i.e. “bound to eventuate in the ordinary course”.

The precise wording of any pollution or climate change exclusion should be carefully considered prior to inception of the policy period. The causative language used can significantly alter the scope of coverage and prospects of indemnity (see, for example, Brian Leighton v Allianz [2023]).

Authors:

Climate Risk Series:

Part 1: Climate litigation and severe weather fuelling insurance coverage disputes

Part 2: Flood and Storm Risk – Keeping Policyholders Afloat

A “WIN WIN” for Policyholders

Background

Delos Shipholding S.A. v Allianz Global Corporate and Specialty S.E. [2024] EWHC 719 (Comm) is one of several recent judgments to consider the scope of an insured’s duty of fair presentation under the English Insurance Act 2015 (the “Act”) and helpfully applies that duty in a manner likely to favour policyholders; also noteworthy are the Commercial Court’s observations on the concept of fortuity and on the duty to sue and labour. The Court additionally considered and rejected the insureds’ claim under section 13A of the Act for damages arising from late payment, which is not covered in this article.

Facts

The bulk carrier ‘WIN WIN’ (the “Vessel”) was insured under a policy (the “Policy”) incorporating an amended form of the American Institute Hull War Risks and Strikes clause.

In February 2019, the Master unknowingly anchored the Vessel in Indonesian territorial waters without permission. Some days later, the Indonesian Navy detained the Vessel for having done so illegally. The Master was prosecuted for contravening Indonesian shipping law, with the Vessel only being redelivered to the insureds in January 2020. The insureds alleged that the Vessel had become a constructive total loss and served several Notices of Abandonment on insurers, all of which were rejected. The insureds then commenced suit to claim for total loss of the Vessel under the Policy, as well as damages for late payment of their claim under section 13A of the Act.

At trial, insurers accepted that the conditions for a total loss had had been met, but alleged that (i) they were entitled to avoid the Policy for material non-disclosure, (ii) the detainment was not fortuitous, and (iii) the delay in release was materially caused by the insureds’ unreasonable conduct in breach of their duty to sue and labour. None of the defences succeeded and the Court allowed the insureds’ claim. The insureds’ claim for damages under section 13A of the Act was, however, dismissed.

Material non-disclosure

At the time the Policy was renewed on 29 June 2018, one Mr Bairactaris, who was the sole director of the first claimant (the shipowner), was being prosecuted by the Greek authorities on charges relating to a shipment of heroin (the “Charges”). Mr Bairactaris was also at all material times a nominee director of the first claimant. In other words, he exercised no independent judgment as director and instead acted on the instructions of other persons, who in this case where the second claimant (the Vessel’s commercial managers) and its owner.

Insurers sought to avoid the Policy on the basis that the insureds had breached their duty of fair presentation. Accordingly, Insurershad to establish that:

- the insureds had actual or constructive knowledge of the Charges;

- the Charges were a material circumstance that should have been (but was not) disclosed at the time of renewal; and

- the relevant underwriter had been induced by the non-disclosure of the Charges to write the risk.

(i) Knowledge

So far as actual knowledge was concerned, since Mr Bairactaris was the only individual within the claimants who knew of the Charges, the key issue was whether the first claimant had been fixed with knowledge of the Charges via section 4(3)(a) of the Act, which attributes to an insured “what is known to ... the insured’s senior management”. Section 4(8)(c) of the Act defines senior management as “those individuals who play significant roles in the making of decisions about how the insured’s activities are to be managed or organised”.

Notwithstanding his position as nominee director, the Court found that Mr Bairactaris was not part of senior management. It was the substance of the role played by him which was determinative, and since his responsibilities as sole nominee director were confined to executing administrative formalities (rather than the organisation of the first claimant’s activities), he could not be regarded as senior management.

This case thus demonstrates the key principles regarding the “knowledge” of a corporate policyholder and re-states the balance under English insurance law between the rights of the insurer to be provided with the material facts prior to inception of a policy against the practical challenges faced by those responsible for the insurance of corporate policyholders in ensuring they are in possession of the material facts in the first place.

As the Court also found that the insureds also did not have any constructive knowledge of the Charges, the defence of material non-disclosure failed at the first hurdle. The Court nevertheless continued to consider the remaining issues

(ii) Materiality

The parties agreed that the test for materiality was substantively unchanged by the Act, i.e. it was whether a prudent underwriter would have wanted to take the undisclosed circumstances (here, the Charges) into account.

The more controversial issue was whether the hypothetical prudent underwriter could also take into account exculpatory circumstances under the test for materiality. These consisted of information that the insureds would also have made known to insurers had the Charges been disclosed, including in this case:

- Mr Bairactaris’ firm belief that the charges were without foundation; and

- the fact that Mr Bairactaris was a nominee director fulfilling only an administrative function and had no role in the operation of the Vessel.

The Court observed that, had it been necessary to decide, it would have held that that exculpatory circumstances could be taken into account; were it otherwise, an insurer “could … be as selective as it liked in how it defined the circumstances which it alleged could be disclosed”. On the facts, the Court observed that the Charges (considered with the said exculpatory circumstances) would have been material and would have led a prudent underwriter to consider imposing a condition, e.g. that Mr Bairactaris should be replaced as a nominee director.

(iii) Inducement & Remedy

The Court found that, had the Charges been disclosed, the actual underwriter would have imposed a condition requiring replacement of Mr Bairactaris as nominee director. The test for inducement under section 8(1)(b) of the Act would thus have been satisfied – the situation was one where, but for the non-disclosure of the Charges, insurers would only have entered into the Policy on different terms.

Insurers would thus have been entitled to treat the Policy as though it included the above condition (per paragraph 5 of Schedule 1 of the Act). The more interesting issue was whether, in this case, it was equally open to the insured to then prove that it could and would have complied with the condition. The Court, accepting that “sauce for the goose [was] … equally sauce for the gander”, opined that insureds could, and that on the facts the insureds would, have complied with a condition requiring replacement of Mr Bairactaris in any event; as such, insurers would have been without a remedy even if they had successfully proved knowledge of the Charges.

Other issues

This wide-ranging judgment covered several other issues, two of which are dealt with below.

(i) Fortuity

Insurers relied on the proposition set out in The Wondrous [1991] 1 Lloyd’s Rep 400, that the ordinary consequences of an assured’s deliberate and voluntary conduct are not fortuitous and do not fall within the cover provided by all risks policies. Insurers argued that, by anchoring in Indonesian waters, the Vessel had voluntarily exposed herself to the operation of local law. The consequent detention was simply an ordinary consequence of that voluntary conduct.

These arguments failed. The Court declined to read the proposition in The Wondrous so widely and instead clarified that the proposition had two aspects:

- First, there must be some choice by the insured. This implies awareness that a decision is being made between two or more options which are different in some relevant sense.

- Second, the consequences must be such as to flow in the ordinary course of events. This requires the consequence to be “inevitable in the sense that it is bound to eventuate in the ordinary course”.

Neither aspect was satisfied on the facts. Since the Master did not realise that the Vessel was in Indonesian waters to begin with, there was no conscious choice by the Master to anchor there. Further, since at the time of detention the Indonesian navy had only just begun to arrest vessels that had been anchored in Indonesian waters without permission (whereas previously there no reported cases of such detention), the detention was neither inevitable nor an ordinary consequence of the Vessel’s conduct.

(ii) Sue and Labour

Both the terms of the Policy and section 78(4) of the Marine Insurance Act 1906 imposed on the insureds a duty to sue and labour. In simple terms, this duty is analogous to a contract party’s duty to mitigate its losses caused by a breach of contract and in the same way, the duty to Sue and Labour requires the insured to make every attempt to reduce the possible exposure to loss.

Insurers argued that, by being side-tracked into discussions with the Navy which involved considerations of a bribe or something similar (which the insureds were ultimately not prepared to do), the insureds had unreasonably protracted Indonesian Court proceedings against the Master and delayed the release of the Vessel.

The Court reiterated the well-established principle that an alleged breach of the duty to sue and labour would only afford insurers a defence where the breach breaks the chain of causation between the insured peril and the loss. This required the insured to act in a way in which no prudent uninsured would have acted; a mere error of judgment or negligence would not suffice. On the facts, there was no breach of the duty – given the uncertain circumstances faced by the insureds, there was no way of their knowing that engaging in discussions with the Navy would “slow things down”, so it could not be said that the insureds had acted in a way that no prudent uninsured would have acted.

Comment

The Court’s policyholder-friendly reading of both the elements of the duty of fair presentation, as well as of the meaning of the “ordinary consequences of an assured’s deliberate and voluntary conduct”, are welcome developments for policyholders. That said, many of the Court’s observations – particularly in relation to the issues of materiality and insurers’ remedies – were obiter, and it remains to be seen if future judgments will follow the lead established here.

Authors

Climate Risks Series, Part 1: Climate litigation and severe weather fuelling insurance coverage disputes

The global rise in climate litigation looks set to continue, with oil and gas companies increasingly accused of causing environmental damage, failing to prevent losses occurring, and improperly managing or disclosing climate risks. Implementation of decarbonisation and climate strategies is subject to scrutiny across all industry sectors, with claims proceeding in many jurisdictions seeking compensation for environmental harm as well as strategic influence over future regulatory, corporate or investment decisions.

Evolving risks associated with rising temperatures have significant implications for the (re)insurance market as commercial policyholders seek to mitigate exposure to physical damage caused by severe weather events; financial loss arising from business interruption; liability claims for environmental pollution, harmful products or ‘greenwashing’; reputational risks; and challenges associated with the transition towards clean energy sources and net zero emissions.

Litigation Trends

Cases in which climate change or its impacts are disputed have been brought by a wide range of claimants, across a broad spectrum of legal actions including nuisance, product liability, negligence, fiduciary duty, human rights and statutory planning regimes. Approximately 75% of cases so far have been commenced in the US, alongside a large number in Australia, the EU and UK.

Science plays a central role and can be critical to determining whether litigants have standing to sue. The emerging field of climate physics allows for quantification of greenhouse gas (“GHG”) emitters’ responsibility, with around 90 private and state-owned entities found to be responsible for approximately two-thirds of global carbon dioxide and methane emissions. Recent advances in scientific attribution may provide evidence for legal causation in claims relating to loss from climate change or severe storms, flooding or drought.

Directors of high-profile companies may be personally targeted in such claims as liable for breach of fiduciary duties to the company or its members, in failing to take action to respond to climate change, or approving policies that contribute to harmful emissions.

Recent Cases

An explosion of ‘climate lawfare’ has kicked off in recent years, with the cases highlighted below indicative of key themes.

Smith v Fonterra [2024]

The New Zealand Supreme Court reinstated claims, struck out by lower courts, allowing the claimant Māori leader with an interest in customary land to proceed with tort claims against seven of the country’s largest GHG emitting corporations, including a novel cause of action involving a duty to cease materially contributing to damage to the climate system. This was an interlocutory application and the refusal to strike out does not mean that the pleaded claims will ultimately succeed on the merits. However, the judgment is significant in demonstrating appellate courts’ willingness to respond to the existential threat of climate change by allowing innovative claims to be advanced and tested through evidence at trials.

R v Surrey County Council [2024]

In a case brought by Sarah Finch fighting the construction of a new oil well in Surrey, the UK Supreme Court (by a 3:2 majority) ruled that authorities must consider downstream GHG emissions created by use of a company’s products, when evaluating planning approvals. The Council’s decision to grant permission to a developer was held to be unlawful because the environmental impact assessment for the project did not include consideration of these “Scope 3” emissions, when it was clear that oil from the wells would be burned.

Verein KlimaSeniorinnen [2024]

An association of over 2,000 older Swiss women complained that authorities had not acted appropriately to develop and implement legislation and measures to mitigate the effects of climate change. The Grand Chamber of the European Court of Human Rights held that Article 8 of the European Convention encompasses a right for individuals to effective protection by state authorities from serious adverse effects of climate change on their life, health and wellbeing. Grand Chamber rulings are final and cannot be appealed: Switzerland is now required to take suitable measures to comply. While not binding on national courts elsewhere, the decision will be influential.

ClientEarth v Shell [2023]

The English High Court dismissed ClientEarth’s attempt to launch a derivative action against the directors of Shell plc in respect of their alleged failure to properly address the risks of climate change, indicating that claims of this nature brought by minority shareholders will face significant challenges. The Court noted that directors (especially those of large multinationals) need to balance a myriad of competing considerations in seeking to promote the success of the company, and courts will be reluctant to interfere with that discretion, making it harder to establish that directors have breached their statutory duties.

US Big Oil lawsuits

Following lengthy disputes over forum, proceedings against oil and gas companies in the US are gaining momentum, paving the way for the claims to be substantively examined in state courts. Many actions against the fossil fuel industry seek to establish that defendants knew the dangers posed by their products and deliberately concealed and misrepresented the facts, akin to deceptive promotion and failure to warn arguments relied upon in other mass tort claims in the US, arising from the supply of tobacco, firearms or opioids.

Implications for Policyholders

With increasing volatility and accumulation risk, insurers will look to mitigate exposures through wordings, exclusions, sub-limits and endorsements. The duty to defend is the first issue for liability insurers, given the number of policyholders affected and the potential sums at stake in indemnity and defence costs.

In 2021, the Lloyd’s Market Association published a model Climate Change Exclusion clause (LMA5570). Property policies exclude gradual deterioration, with express wording or impliedly by the requirement of fortuity, and liability insurance typically excludes claims arising from pollution.

Lawsuits have been filed in the US over insurance coverage for climate harm, including Aloha Petroleum v NUF Insurance Co of Pittsburgh (2022), arising from claims by Honolulu and Maui, and Everest v Gulf Oil (2022), involving energy operations in Connecticut. Policy coverage may depend on whether an “occurrence” or accident has taken place, as opposed to intentional acts or their reasonably anticipated consequences (Steadfast v AES Corp (2011).

Policyholders should review their insurance programmes with the benefit of professional advice to ensure adequate cover for potential property damage, liability exposures and legal defence costs.

In the following instalments of our Climate Risks Series, we will examine the impact of reinsurance schemes and parametric solutions, and coverage for storm and flood-related perils in light of recent claims experience.

Authors

Amy Lacey, Partner

Ayo Babatunde, Associate

Queenie Wong, Associate

Fenchurch Law announces Singapore expansion plans

Fenchurch Law, the UK’s leading firm working exclusively for insurance policyholders and brokers, plans to offer its specialist legal support outside of the UK for the first time, announcing plans for the opening of a new office in Singapore.

Through its new hub, Fenchurch Law will be working with policyholders and brokers from across Singapore and the wider Asia-Pacific region to provide first-class support on high value, complex, commercial insurance coverage disputes, as it has done in the London Market since 2010.

The firm’s international expansion follows the recent announcement that it had transitioned to an employee-owned business model through the launch of an Employee Ownership Trust (EOT), which saw 60% of its shares awarded to its people. Fenchurch Law will be the first EOT business to operate in Singapore.

Managing Partner at Fenchurch Law, David Pryce, commented: “As a purpose driven organisation, we exist in order to help level the playing field between policyholders and their insurers. This is a need that exists in all insurance markets around the world, and we’re delighted to be taking the first step in furthering our purpose internationally with the opening of our Singapore office."

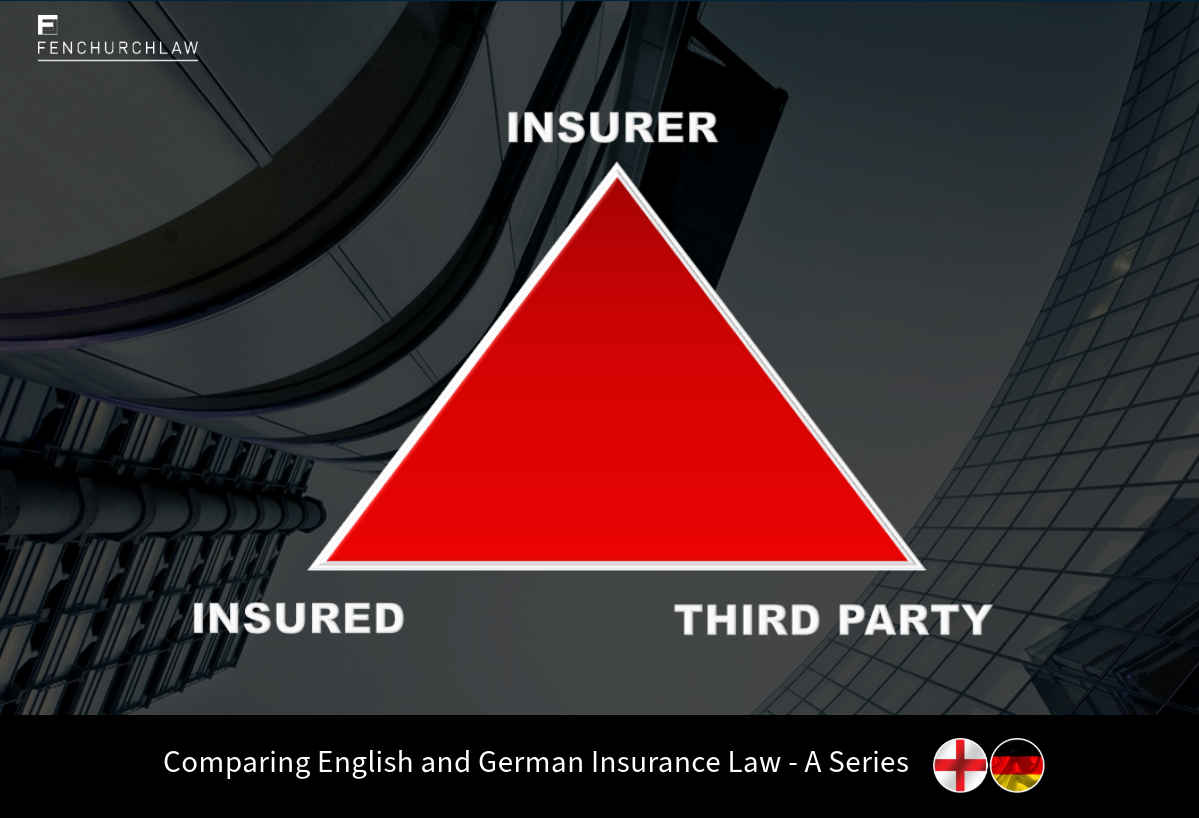

Comparing English and German Insurance Law - Part 2: A Third Party’s Right to Claim Directly Against Insurers

Insurers have deep pockets, while the average person on the street is incapable of paying claims for significant damages. That makes insurers, in most cases, a far more attractive target to claim against compared to the person that caused the damage. This article will give an overview of the different positions in England and Germany with respect to a third party’s right to claim directly against insurers. It focuses on the direct rights which result from statutory law, and does not cover the possibilities to claim against an insurer following a contractually agreed assignment of rights from the insured to the third party.

Insurance and Third Parties

In considering this issue, it is worth looking at the aim of an insurance contract. Typically, insurance is taken out by a policyholder to avoid a situation where it cannot afford to make good what was lost. For example, fire insurance is purchased because the insured wants the insurer to provide the money that is needed to rebuild the home that was burnt down. A doctor takes out professional indemnity insurance to be protected from the financial ruin which would follow if they had to pay compensation for a serious error.

The latter example is different from the former. In the first example, the only parties affected by the insurance contract are the insurer and the homeowner. In the second example, there is another person who has an interest that insurance is taken out: the patient, i.e., the third party.

Thus, depending on the nature of the insurance contract, there might be more than just the insured who has an interest that there is insurance in place. Therefore, it can be said that in some cases, in addition to the obvious purpose of protecting the policyholder from financial ruin, the insurance contract is also meant to provide protection for a third party. This is why in some cases the legislature has decided to make insurance compulsory, with motor insurance being the prime example.

The relevant legislation

There are essentially two pieces of legislation in England which are relevant to this issue: The Third Parties (Rights against Insurers) Act 2010 and the European Communities (Rights against Insurers) Regulations 2002. The latter remains in force following Brexit.

In Germany, the relevant provision is § 115 Versicherungsvertragsgesetz (VVG, “Insurance Contract Act”).

Motor insurance

In both England and Germany, the law provides the victim of a motor accident with a right to claim directly against the liable person’s insurer.

In England, a victim of a motor accident has a direct claim against the driver’s insurers pursuant to regulation 3(2) of the European Communities (Rights against Insurers) Regulations 2002. The right arises when the conditions of the regulations are met. Importantly, the victim must be a resident of one of the EEA states (regulation 2(1)) and the accident must have happened on a road or public place in the UK. Furthermore, the vehicle must be insured according to the requirements of section 145 of the Road Traffic Act 1988 as well as normally based in the UK (regulation 2). As a result, the third party has the exact same rights against the insurers as the insured itself.

The position is in essence the same under German law. Pursuant to § 115 I 1 Nr. 1 VVG, an injured person can directly claim against the liable person’s insurer.

Other liability insurance

For liability insurance other than motor, the laws of both countries differ fundamentally.

England

In England, the relevant Act for other liability policies is the Third Parties (Rights against Insurers) Act 2010. Prior to this Act’s predecessor (the similarly named 1930 Act), it was seen as unjust that a third party that had a valid claim against the insured was left in a vulnerable position in cases where the insured became insolvent: in these instances, any insurance monies went into the general pool for the insured’s general creditors,[i] and often the third party was left without any remedy. The 1930 Act provided, as does the 2010 Act, that the insured’s rights against its liability insurers are transferred to the third party.

The sole trigger for the direct claim against the insurer is that the insured becomes a “relevant person” pursuant to section 1 of the 2010 Act. This term is defined in the Act, but it essentially applies when the insured becomes insolvent. Consequently, in England, a person that suffered loss through the conduct of an insured that has valid liability insurance cover in place can directly claim against the insurers if the insured is insolvent.

Germany

Pursuant to § 115 I 1 Nr. 2 and Nr. 3 VVG, a third party may sue the insurer directly in two additional cases.

First, where the insured is insolvent (Nr. 2) and, secondly, where the insured’s whereabouts are unknown (Nr. 3). However, and this is crucial, § 115 VVG only applies to compulsory liability insurance. A prime example of this in Germany is professional indemnity insurance for lawyers, architects, notaries and doctors. However, there is no obligation to take out PI insurance for construction companies, for example.

As a consequence, a third party that is injured by an insured cannot claim directly against the insurer if the insurance is not compulsory. This differs considerably from English law, where the third party can claim against any liability insurer.

Conclusion

Obviously, the English position is significantly more advantageous to third parties than the German one. The English law is understandable from the point of view of fairness towards injured third parties. Where insurance is in place, why should the third party not be able to assert its claim for damages just because the insurance was not compulsory?

On the other hand, the German position is understandable from a plainly legal perspective: the reason for granting a direct claim reflects the fact that compulsory insurance is ordered for reasons of victim protection. It secures the injured third party a debtor who is willing to negotiate and pay and who is largely insolvency-proof.[ii] Outside of compulsory insurance, the German legislature saw no reason to establish a direct claim by the injured party because a non-compulsory liability insurance policy is taken out by the policyholder solely to protect his own assets in the event that claims for damages are made against him.[iii]

Isabel Becker is a Foreign Qualified Lawyer at Fenchurch Law

[i] Rob Merkin, Lowry, Rawlings and Merkin’s Insurance Law: Doctrine and Principles (4th edn, Hart 2022), 415.

[ii] Official justification of the Federal Government's draft bill on the Insurance Contract Reform Act of 20 December 2006, Bundestagsdrucksache 16/3945, pp. 50, 88 f.; see also Regional Court of Nuremberg-Fürth, judgement of 21.08.2010, 4 O 2987/09.

[iii] Rüffer/Halbach/Schimikowski, commentary on the VVG, § 115 Rn. 1.

Archer v Ace (or, The Demise Of LEG3?)

Introduction

In the London Market there is, by and large, a common understanding about how LEG3 and the other defects exclusions operate, and what they are intended to do. That doesn’t mean that disagreements don’t arise about how a particular defects exclusion might apply to a particular set of facts, but those disagreements tend to be relatively rare, and the London Market tends to deal with what we call Construction All Risks claims (or what would be known in the US as Builders’ Risk claims), quite well on the whole.

As a result, those using the defects exclusions in the London Market, whether that is insurers, brokers, or the more sophisticated policyholders, tend to overlook the fact that several of the clauses, in both the LEG and DE suites of exclusions, are actually very difficult to understand for those who come to the clauses with the (surely reasonable) aspiration of wanting to determine the meaning of the clauses from the words that they contain.

Towards the end of last year I wrote about the potential impact of the first Court decision anywhere in the world which considered the meaning of the defects exclusion which (along with DE5, which is much less commonly used outside the UK) is intended to preserve the most generous coverage for damage to works under construction, LEG3, in the case of South Capitol Bridgebuilders v Lexington. That case was decided by a Court in the District of Columbia, but applied the Law of Illinois. Now, like buses, a second decision has been handed down in the US which considers LEG3, this time applying the Law of Florida, in the case Archer Western - De Moya Joint Venture v Ace American Insurance Co.

The decision in SCB sounded alarm bells for the Builder’s Risk community in the US, and presumably also for the LEG Committee, who are responsible for the LEG defects exclusion clauses. It raised at least two questions of significance: what constitutes damage for the purpose of triggering a Builder’s Risk policy; and what is the meaning of the LEG3 clause? Its answers to those questions were striking: property that from an English law perspective would have certainly been regarded as merely being in a defective condition was held by the Court in SCB to have suffered damage. With regard to the meaning of LEG3, the Court in SCB appeared to be unable to form a view, and held that the clause was ambiguous: “egregiously so”.

The big question for those who, like me, have an interest in the health of the Builder’s Risk market, was whether SCB would come to be regarded as an outlier decision, or one that would have a meaningful impact? Archer v Ace suggests the latter.

The judgment in Archer concerns an application for summary judgment by the insurer which was denied, and so the issues in the case will continue towards a substantive trial in due course. However, the judgment runs to some 66 pages, and so the issues were considered in some detail. I am not going to try to cover all of the detail but, as with my article on SCB, am going to focus instead of what the most important elements might mean for the Builder’s Risk market.

The facts

Again, I’ll start with a very brief description of the facts, which up to a point may create a sense of Deja Vu for those familiar with the SCB decision. Once more we have a Builder’s Risk claim relating to inadequate concrete in a bridge under construction. We have a disagreement about whether the works under construction were damaged (so as to trigger the Builder’s Risk policy), or whether the works were merely defective (which would not trigger the policy). We have a policy that contains a LEG3 defects exclusion. And we have disagreements about what LEG3 means, and about how one might establish what constitutes the “improvements” with which LEG3 is concerned.

In Archer the policyholder was a design and build contractor for the snappily titled “I-395/SR 836 Reconstruction / Rehabilitation Project” in Miami, Florida, which included the construction of a “signature bridge”. The design of the bridge involved batches of concrete, the production of which included the addition of “fly ash” from a pressurised fly ash silo, which had a mechanical system which was intended to allow specified amounts of fly ash to be added to the concrete batches. At some point between August and November 2020 the pressure relief valve of the silo failed, so that certain batches were “adulterated by an excessive amount of fly ash”.

I am not my firm’s expert on concrete (the “I ❤️ concrete” mug on my colleague Joanna Grant’s desk probably tells you who is) but, as the Court explained in Archer, although cement and concrete are terms that are often used interchangeably, they aren’t the same. Rather, cement is one of the ingredients of concrete, with the other common ingredients of concrete being fly ash, water, and aggregates. So, the presence of fly ash in concrete is not a problem in and of itself. In fact, in one sense, the more fly ash there is in the concrete, the better, as long as using additional amounts of fly ash does not come at the expense of the amount of cement used. High proportions of both fly ash and cement “generally increases the overall compressive strength of the concrete”. The problem comes when, as in Archer, additional amounts of fly ash are used at the expense of the amount of cement used. Then the compressive strength of the concrete is impaired.

When the policyholder became aware that some of the concrete had inadequate compressive strength, it submitted a claim for indemnity for the cost of repairing the concrete. The insurer denied coverage “reasoning the concrete constituted a defective material due to to the excess fly ash, and `because of this defect the material was never in a satisfactory state and therefore was not damaged’”.

Based on the above, the Court was required to address the following questions:

- Did the insured property suffer damage?

- Is LEG3 ambiguous?

In approaching those questions, the Court applied the test for summary judgment under the Law of Florida, which is that “summary judgment is appropriate where there is ‘no genuine issue as to any material fact’, and the moving party is ‘entitled to judgment as a matter of law’” (per Federal Rule of Civil Procedure 56), and that “when deciding whether summary judgment is appropriate, the court views all facts and resolves all doubts in favour of the non-moving party”.

It also applied the test for ambiguity under the Law of Florida, which is that “a policy is ambiguous only when ‘its terms make the contract susceptible to different reasonable interpretations, one resulting in coverage and one resulting in exclusion’”, and that “if there is an ambiguity, then it is construed against the insurer and in favour of coverage”.

As I did in my SCB article, I’ll explain what the Court held in relation to each issue, and add some comments of my own.

Did the insured property suffer damage?

As with SCB, the policy in Archer didn’t define the term “damage”. However, rather than just going to the dictionary, as the judge had done in SCB, the judge in Archer held that the test for damage had been determined by previous cases, and that it “requires a tangible alteration to the covered property”. That test is largely consistent with the test under English law, which requires a change in the physical condition of the insured property, which impairs the value or the usefulness of that property.

On the facts, and based on the high bar required to give summary requirement, the judge was “not prepared to accept the insurer’s argument that damage to the cement did not involve a physical alteration” and so that issue will remain to be determined at trial.

From an English law perspective, the issue is an interesting one, and the correct answer is not obvious. The correct answer will, in my view, turn on what is considered to be the relevant property: the concrete, or the cement?

If I was representing the policyholder, I would be arguing that the relevant property is the cement, and that the cement has become damaged by being overlaid with excessive quantities of fly ash. We know, from cases such as Hunter v Canary Wharf and R v Henderson, that the deposit onto insured property of excessive quantities of benign substances is capable of constituting damage, where the excessive quantities of those substances cost more money to remove than if ordinary quantities of those substances were present. On that basis, I would argue that the cement has undergone an adverse change in physical condition, that impairs both its value and its usefulness by coming into contact with excessive amounts of fly ash: the policyholder started out with cement which had a particular value, and as a result of the change in physical condition that occurred when the fly ash was added, it no longer retains that value.

If, on the other hand, I was representing the insurer, I would be arguing that the relevant property is the concrete, and that it was in a defective condition from the moment it was created (by the mixing of the cement and the fly ash). I would argue that from that point onwards it didn’t undergo any further “tangible alteration”, meaning that the test for damage hasn’t been satisfied. We know from the Bacardi case that, in English law, the creation of a defective finished product doesn’t constitute damage. Although Tioxide tells us that damage does occur when a defective finished product undergoes a change in physical condition that constitutes a further impairment of value or usefulness, that hasn’t happened in Archer, where the concrete was under-strength as soon as it came into existence, and remained that way until discovery.

So, which material should the Court be concerning itself with, the cement or the concrete? Although, as a policyholder representative, I would like to say that the Court should be concerning itself with the cement, I don’t think that’s right. The property which needs fixing is the concrete. The claim is not for the cost of repairing the cement, but for the cost of repairing the concrete.

On the basis of the above, although the insurer wasn’t successful in obtaining summary judgment on the proposition that the insured property hadn’t suffered damage, I expect the insurer to succeed on that issue at trial.

Is LEG3 ambiguous?

As in SCB, the Court in Archer first considered whether it was ambiguous as to whether LEG3 was an extension or an exclusion. The policyholder had argued that LEG3 is “both a coverage grant and an exclusion”, and the Court held that LEG3 “generates a functional extension, or broadening, of coverage”, as compared with the narrower exclusion which LEG3 had replaced by endorsement.

That doesn’t sound right to me, and in my view that doesn’t reflect the position under English Law. Tesco v Constable makes clear that the main insuring clause of a policy can only be widened by other clauses in the policy by using the clearest terms (and ABN Amro then gave an illustration of just how clear those terms needed to be, i.e very).

The second potential ambiguity in LEG3 was what it means to “‘improve’ the original workmanship”. Here, the Court in Archer didn’t develop the arguments any further than in SCB, and simply agreed that LEG3 was ambiguous in that regard.

So, where does that leave us?

In a few short months two different Courts, applying the law of two different States, have both held that LEG3 is ambiguous. In fact that’s being somewhat diplomatic, and it’s probably more true to say that neither Court could work out what on earth LEG3 was supposed to mean. That being the case, if SCB suggested that there was an opportunity for the LEG Committee to take a fresh look at the drafting of LEG3 and the other defects exclusions, Archer suggests that it really has no option, and that it must do so as a matter of urgency.

If LEG3 is going to be amended (as, in my view, it must), then the LEG Committee also has an opportunity to overhaul the other defects exclusions.

Although the DE clauses and the LEG clauses have different origins, it is not helpful for there to be two different suites of clauses which are so similar to each other. In my view it would be much better for there to be a single suite of clauses which captures the best elements of the current clauses.

So:

- There should be a clause which is concerned with causation, and which excludes the cost of repairing any damage caused by mistakes (which would essentially be a re-drafted, simplified, version of DE1 and LEG1, which both do the same thing);

- There should then be two clauses which are concerned with the condition of the relevant property before the damage occurs. One of those clauses would exclude the cost that would have been incurred to repair any defects which were present in property that has become damaged, if those defects had been discovered immediately before the damage occurred (i.e. a re-drafted, simplified, version of LEG2). The other clause would exclude entirely the cost of fixing damage to property which was in a defective condition immediately before the damage occurred (i.e. a re-drafted, simplified, version of DE3, which one might call LEG2A in the new suite);

- The final clause would exclude only the cost of improvements (i.e. a re-drafted, simplified, version of LEG3). My SCB article proposed an amended version of LEG3, and a few months later I would still stand behind that draft.

Those clauses would be made to be bought together. So, a policy with the most limited cover would contain only LEG1. A policy with wider cover would contain both LEG1, and also either LEG2 or LEG2A (whichever is most appropriate for the type of project involved). A policy with the widest cover would contain LEG1, plus one of LEG2 or LEG2A, and also LEG3. Where a policy contains more than one of the new defects exclusions, the policyholder should be able to choose which to apply in the event of a claim, with each exclusion coming with a different deductible. LEG1 would have the lowest deductible. LEG2 or LEG2A would have a higher deductible, and LEG3 would have the highest deductible of all.

That, in my view, would represent a very healthy outcome for insurers, brokers, and policyholders alike, and constitute a positive response to the issues raised by SCB and Archer: a single suite of defects exclusions; which are simply drafted and easy to understand; and which fit together with each other, and are intended to be used in conjunction with each other.

David Pryce is the Managing Partner at Fenchurch Law

Covid “Catastrophe” Triggers BI Reinsurance

The first UK court ruling on the reinsurance of Covid-19 losses has confirmed coverage under excess of loss policies taken out by Covéa Insurance plc (“Covéa”) and Markel International Insurance Co Ltd (“Markel”). Mr Justice Foxton allowed recovery against reinsurers for losses occurring while the underlying policyholders were unable to use their business premises, due to government restrictions, on the basis that the pandemic was a “catastrophe” within the meaning of the reinsurance contracts.

Covéa and Markel paid out a combined total of over £100 million to policyholders for Covid-19 business interruption (“BI”) losses and made claims under their respective reinsurances with UnipolRe Designated Activity Company and General Reinsurance AG. Disagreements arose concerning the scope of cover under the reinsurance contracts, and a consolidated judgment was given in two separate appeals under s.69 of the Arbitration Act 1996, against arbitration awards dated January and July 2023. In summary, the appeals raised the following issues:

- Whether the relevant Covid-19 losses arose out of and were directly occasioned by one catastrophe on the proper construction of the reinsurances. Both arbitration awards found that they did; and

- Whether the respective Hours Clauses in the reinsurances, which confined the right to indemnity to “individual losses” within a set period, meant that the reinsurances only responded to payment in respect of the closure of insured premises during the stipulated period. The Markel arbitral tribunal found that the relevant provision did have that effect, while the tribunal in the Covéa arbitration found that it did not.

The Judge found in favour of the reinsureds on both issues.

Loss Arising from One Catastrophe

Coincidentally, both Covéa’s and Markel’s losses arose through direct insurance of nurseries and childcare facilities, which had been forced to close from 20 March 2020 by the UK government’s Order of 18 March 2020. The reinsurance contracts contained similarly worded Hours Clauses based on the LPO 98 market wording, including a form of aggregation provision operating by reference to a specified number of hours’ cover for any “Event” or “Loss Occurrence” (terms previously held to have the same meaning), defined as “all individual losses arising out of and directly occasioned by one catastrophe”.

For any Event or Loss Occurrence “of whatsoever nature” which did not include losses arising from specified perils (such as hurricane, earthquake, riot or flood) listed in the Hours Clauses, the limit was 168 hours (i.e. 7 days). Infectious disease was not a named peril and the 168 hours limit applied.

In circumstances where the arbitral awards were based on mixed findings of fact and law, it was common ground that the court could not interfere on a s.69 appeal unless the arbitral tribunal either had erred in law or, correctly applying the relevant law, had reached a decision on the facts which no reasonable person could have done.

On general principles of construction, the Judge endorsed the comments of Mr Justice Butcher in Stonegate v MS Amlin [2022] that “in considering whether there has been a relevant ‘occurrence’, the matter is to be scrutinised from the point of view of an informed observer placed in the position of the insured” (per Rix J. in Kuwait Airways [1996]).

Reinsurers argued that the gradual unfolding of the pandemic did not qualify as a “catastrophe” under the reinsurance policies, taking account of the historical development of property excess of loss market wordings, which was said to implicitly demonstrate the requirement for a sudden and violent event or happening, which could not be established on the underlying facts. Further, reinsurers claimed that a catastrophe is a species of occurrence or event that must satisfy the “unities” of time, manner and place, applied by Lord Mustill in Axa v Field [1996].

The Judge concluded that terms of the reinsurance contracts supported a generous application of the unities test, given the requirements for losses under multiple policies, with a duration potentially exceeding 504 hours (the period specified in relation to flood perils, i.e. 21 days), within broad geographical limits, indicating that a covered catastrophe could have a potentially wide field of impact.

While acknowledging the difficulties inherent in distinguishing between a “catastrophe” properly so-called, as an appropriate basis for aggregation, and a series of discrete losses sharing some common point of ancestry, the Judge held for purposes of the reinsurance claims under consideration that a catastrophe:

- Must be capable of directly causing individual losses, likely in most cases to exclude “states of affairs”.

- Is a coherent, particular and readily identifiable happening, with an existence, identity and “catastrophic” character arising from more than the mere fact that substantial losses have occurred.

- Will be identifiable, in a broad sense, as to its time of coming into existence and of ceasing in effect.

- Involves an adverse change on a significant scale from that which proceeded it.

Applying these principles to the findings in each award, the Judge noted that both tribunals had referred to the outbreak of Covid-19, and the resulting disruption of life in the UK, leading up to and necessitating the 18 March Order, as a catastrophe. In circumstances where the various government directives, including the 18 March Order, were rational and considered measures taken in the public interest, it was not necessary to explore the issue of whether a government order in isolation could be viewed as a catastrophe, since “the pandemic and the response thereto could not be disentangled”, an approach consistent with the decisions in Star Entertainment v Chubb Insurance Australia [2021] and Gatwick Investment v Liberty Mutual [2024].

Interpretation of the Hours Clauses

Covéa and Markel argued that all BI losses arising from the 18 March Order were reinsured, notwithstanding the BI losses continuing after expiry of the 168 hour period. The Covéa arbitral award endorsed this approach, determining that the reference to “individual loss” meant “a loss sustained by an original insured which occurs as and when a covered peril strikes or affects insured premises or property”. However, the Markel tribunal found in favour of the reinsurer, reasoning that it was “natural to think that BI losses occur day by day”, and therefore construing the relevant words as not “dealing with causation but with the occurrence of a particular loss”, since the “subject matter of an ‘Event’, its duration and extent, and its occurrence, are all referenced to losses not perils.”

The effect of the Markel tribunal’s finding was that only 168 hours of BI losses could be recovered from the reinsurer (although the BI had in fact extended until at least June 2020, when the relevant restrictions were first lifted), so that most losses fell outside the scope of cover and Markel was unable to reach the specified attachment point under the reinsurance policy.

In reconsidering this issue on appeal, the Judge was not persuaded that a clear line could be drawn between damage and non-damage BI, as contended by reinsurers, since even the former might continue to manifest after the specified hours period, for example by damage worsening over time. Further, the Court concluded that the “wait and see” analysis applied by the Markel tribunal, premised on the occurrence of BI losses on a day-by-day basis, may lead to “uncommercial consequences” and does not sit easily with the findings in Stonegate and Various Eateries v Allianz [2022], which treated the closure orders as having immediate impact on the insured property with continuous effect, analogous to physical damage to buildings; or with the Supreme Court’s decision in FCA v Arch [2021], which suggested that the correct causal sequence for non-damage BI approximates that of damage-related BI.

The Court therefore dismissed the reinsurers’ appeals as to the meaning of “catastrophe” and allowed Markel’s appeal against the conclusion of the arbitral tribunal as to the effect of the Hours Clause.

Practical Implications

Figures published by the Financial Conduct Authority in March 2023 indicate that, since conclusion of the Test Case in 2021, insurers have paid around £1.4 billion in BI claims. The Commercial Court’s decision in this case provides comfort for cedants with ongoing recoveries, significantly restricting reinsurers’ ability to challenge the presentation of Covid-19 losses under similarly worded excess of loss property policies. It will be interesting to see how the decision may be applied in subsequent cases involving aggregation of losses across multiple jurisdictions. Given that reinsurance contracts typically provide for resolution of disputes by way of (confidential) arbitration proceedings, this clear judgment in favour of the cedants is particularly illuminating.

UnipolSai Assicurazioni SPA v Covea Insurance PLC [2024] EWHC 253

Amy Lacey is a Partner at Fenchurch Law

Comparing German and English Insurance Law – A Series

Introduction

Germany and England have two fundamentally different legal systems – Civil Law, which is based on codified provisions, and Common Law, where court judgments create legally binding precedent to be followed by lower courts in subsequent cases. Does this automatically lead to fundamentally different insurance laws? Or will we be surprised by many similarities? This article will be the first of a series where some peculiarities of English insurance law shall be compared to German insurance law.

The most relevant Acts for private insurance contract law in Germany are the Versicherungsvertragsgesetz (VVG), which can be translated to Insurance Contract Act, and the Bürgerliches Gesetzbuch (BGB), which contains the central provisions of German private law.

English insurance law was codified by several pieces of legislation, such as the Marine Insurance Act 1906 (MIA), the Insurance Act 2015 (IA) as well as the Consumer Insurance (Disclosure and Representations) Act 2012 (CIDRA). Additionally, English insurance law is supplemented by a wide variety of case law.

This first article will look at the difference in provisions dealing with the pre-contractual presentation of the risk by a prospective business insured under the new law. English insurance law was significantly reformed by the IA in 2015. The German VVG was amended in 2008. These changes were made with the intention to make the respective laws, amongst other things, more policyholder-friendly.

The Provisions

Under English law, a prospective business insured must, before it enters into a contract of insurance, make a fair presentation of the risk to the insurer, s.3(1) IA – it has a “duty of fair presentation”. The scope of the duty is set out in the following subsections of the Act and requires, in principle, that the prospective insured discloses every material circumstance which it knows or ought to know. Alternatively, it must disclose in a way which gives the prudent insurer sufficient information to put it on notice that it has to make further enquiries. The disclosure has to be made in a reasonably clear and accessible manner, and every material representation has to be substantially correct, while an expectation or belief has to be made in good faith. There is a “fresh” duty of fair presentation when the contract is renewed or amended.

Importantly, this means that prospective business insureds have to disclose material facts even where the insurer has not expressly asked questions, unless it concerns a circumstance which diminishes the risk, a circumstance which the insurer knows, ought to know or is presumed to know, or where the insurer waives the requirement to disclose information (s.3(5) IA). In substance, the legislator decided that prospective business insureds require less protection as compared to prospective consumer insureds, to which s.3(1) IA is not applicable. Prospective business insureds are therefore burdened with the responsibility to decide which information they have to disclose.

This is – at least for so called “non-large risks” – different under German law. According to § 19 I 1 VVG, which is applicable to both business and consumer insureds, the prospective policyholder must notify the insurer of the circumstances known to it which are material for the insurer's decision to conclude the contract – if the insurer asked about it in writing. The provision is applicable to business insureds which do not fall under the scope of the provision of § 210 VVG, which ensures that insurance sectors dealing with so-called “large risks”, mainly transport, credit and indemnity insurance, are granted wider contractual freedom.

Both English law and German law utilised the same arguments for their respective amendments: the old law did not sufficiently take into account the legitimate interests of prospective policyholders because they were burdened with the responsibility of having to disclose all known relevant circumstances, as well as with the difficult assessment of what was material to the risk. In England, the duty to disclose information where the prospective insured had not been asked was, in light of the consequences of a possible breach, seen as a potential trap (at least for consumers). The German legislator decided to remove this burden from both consumer and business insureds, while the English approach makes a clear distinction between the two. Under German law, the risk of misjudging whether a circumstance is relevant to the risk therefore no longer lies with the prospective policyholder. The German provision mirrors the English provision applicable to consumer insureds under s.2 CIDRA, which imposes a duty on consumer policyholders to take reasonable care not to make a misrepresentation to the insurer.

It is worth noting that German courts are reluctant to accept questions by the insurer that require an assessment by the prospective policyholder, e.g. the question whether there were any “anomalies”. German insurers are therefore prevented from relying on any alleged mis-statement by the policyholder in relation to such questions and cannot decline cover on these grounds. Moreover, insurers can only ask for information that is material to the risk.

According to the explanatory notes to § 19 VVG, the situation differs where the prospective policyholder acts in bad faith: then, the insurer can contest the contract even when he has not asked for the information. However, the German courts set high expectations by requiring evidence of circumstances obviously relevant to the risk which must be so unusual that a question aimed at the circumstances cannot be expected. As a consequence, the number of cases where insurers can actually contest the contract on the grounds of bad faith are significantly limited.

Another noteworthy difference arises with regards to the scope of the duty. Under German law, the prospective policyholder only has to reveal material circumstances of which it actually knows. When the prospective policyholder has forgotten facts, it is obligated to attempt to recall them. The provision does however not indicate that the policyholder must reveal what it should have known, based on a reasonable search (including information held by agents), as required under English law.

Conclusion

Regarding non-consumer insureds, the German provision differs considerably to the law as set out under the IA (while the provisions applicable to consumer-insureds show great similarity). In this respect, Germany’s law can be regarded as more policyholder-friendly than the provision applicable to business insureds under English law. The rationale behind the requirement of having to ask the policyholder in writing is to decrease the risk of misunderstanding as well as to give the policyholder the opportunity to read the enquiries made by the insurers. Obviously, the written requirement also serves as evidence. It is made very clear to the prospective insured what is material to the insurer and what must be done to fulfil obligations. Moreover, the scope of the duty is smaller than under English law, where the prospective insured also has to disclose deemed knowledge.

Isabel Becker is a Foreign Qualified Lawyer at Fenchurch Law

The world’s first LEG3 Court decision, and what it means for the Builders’ Risk market

Introduction

27 years after the London Engineering Group (“LEG”) introduced its suite of defects exclusions, a Court in the District of Columbia in the USA has delivered the world’s first Court decision on the most generous of the three LEG clauses, LEG3, in the case of South Capitol Bridgebuilders v Lexington Insurance Company, No. 21-cv-1436, 2023 US Dist. LEXIS 176573 (D.D.C. Sep 29, 2023). That fact that the Builders’ Risk market (or what we in the UK would call the Construction All Risks, or “CAR” market) has been waiting for a LEG3 decision for this long means that SCB v Lexington was always going to receive a lot of attention. However, the unrestrained and intemperate language used by the Judge means that there is a risk that the decision will create more heat than light, and has the potential to lead to a reaction by Builders’ Risk insurers, particularly in the US, which could negatively affect the interests of policyholders. That would be a great shame, as the availability of appropriate Builders’ Risk insurance is essential for the global construction community. This article therefore attempts to take a step back from the eye-catching language used by the Judge in SCB, and to discuss what a constructive response to the case might look like.

The facts

I’ll start with a very brief description of the facts. The policyholder, SCB, was hired to build the new Frederick Douglas Memorial Bridge, which is a stunningly designed bridge which crosses the Anacostia River in Washington DC, and which is the biggest public works project in the history of the District of Columbia. The design involves three consecutive steel arches on either side of the bridge, which are supported by concrete abutments on either side of the river, and by two v-shaped concrete piers which provide support towards the centre of the river.

The concrete was placed in each of the abutments and piers in separate pours, with workers standing within the formwork and vibrating the concrete in order to achieve even placement. Due to the vibration being carried out inadequately the concrete never achieved even placement, and when the concrete had dried and the formwork was removed, the policyholder saw that the concrete contained voids, referred to as “honeycombing”. The honeycombing diminished the concrete’s weight bearing capabilities, and meant that the concrete had to be repaired so that an even distribution of concrete, without honeycombing, could be achieved.

The policyholder had the benefit of a Builder’s Risk insurance policy issued by Lexington, which contained the 2006 version of the LEG3 defects exclusion. The policyholder submitted a claim to the insurer on the basis that the honeycombing of the concrete constituted “damage” which triggered the main insuring clause of the policy, which was not excluded by LEG3. The insurer refused indemnity on the basis that, in order for there to be damage which triggered the policy it was not sufficient for the honeycombed concrete components to have been in a defective condition from time they were made. Rather, for there to be damage, a subsequent alteration in the physical condition of the concrete components was required.

The insurer also argued that, even if the concrete was damaged, the LEG3 clause excluded coverage because the whole of the remedial works constituted an improvement, on the basis that “if something broken gets fixed, hasn’t that thing been improved?”.

Based on the above the Court (which, although it was in the District of Columbia was applying Illinois Law) was required to address the following questions:

- Did the honeycombing of the concrete components constitute damage, so as to trigger the main insuring clause of the policy?

- Is the meaning of the LEG3 clause unambiguous?

- If the meaning of the LEG3 clause is ambiguous, how should that ambiguity be resolved?

I’ll explain what the Court held in relation to each issue, and add some comments of my own, in turn.

Did the honeycombing comprise damage?

Lawyers from common law jurisdictions who work regularly with policies which are triggered by property damage, whether in relation to works under construction, completed works, or products, will be familiar with the extensive body of authority from around the world in relation to the question of what constitutes “damage”. In this respect it is common for the Courts of a variety of different jurisdictions to look to decisions in other jurisdictions to help inform that issue, not because decisions from other jurisdictions are binding, but because they can be helpful in understanding an issue which has received a significant amount of prior judicial attention.

The insurer in SCB appears to have drawn a significant amount of authority to the Court’s attention, but the Judge could not have been less interested in it (“Lexington does not bother to explain how these non-binding cases are analogous, or why the Court should consider them persuasive”). Ouch. Had the Judge taken the view that the damage authorities were persuasive then the outcome of the case would almost certainly have been different, because most common law jurisdictions clearly do regard damage as a “happening” (which requires a change in physical condition), as opposed to a “condition” (which does not require a change in physical condition). In SCB’s case, there was no change in physical condition, as the concrete components contained honeycombed voids from the outset. According to the authorities in most common law jurisdictions, and certainly in England & Wales, the honeycombing would therefore have meant that the concrete components were in a defective condition from their creation, and the lack of a subsequent change in physical condition would therefore have meant that they didn’t suffer damage.

However, the Judge in SCB not only took the opposite view, but did so in the clearest terms. Asking himself the question of “whether ‘damage’ is properly understood to include the costs of fixing the concrete flaws that weakened the bridge”, he found that “the answer is unambiguously, yes”. So, how did he reach a view that for lawyers in other jurisdictions would find so surprising?

The reason starts with the fact that “damage” was not a term that was defined in the policy issued by Lexington. That meant that under Illinois Law the way to understand the meaning of the term was not to consider any authorities, but to look instead to “plain, ordinary, and popular meaning of the term”. To determine that meaning the Judge looked at Black’s Law Dictionary (10th ed., 2014), which defined damage as “loss or injury to person or property” or “any bad effect on something”.

Applying the above definition, the Judge found that the policyholder’s inadequate vibration of the concrete “caused a decrease in the weight bearing capacity of the bridge and supporting structures”, and that “a decreased weight bearing capacity is surely an injury, or at the very least a bad effect, on the bridge and its support structures”. That analysis may be true as far as it goes, but it can only be justified on the basis that the “decreased capacity” exists in comparison with the intended capacity, and not as compared with a capacity which existed before a change in physical condition which resulted in the decrease. The problem with that approach, is that a decreased capacity as compared with an intended capacity is describing contract works which are in a defective condition, and Builders’ Risk policies are not intended to cover the cost of repairing defective but undamaged property. That is a commercial risk for builders which the Builders’ Risk insurance market isn’t, and never has been, prepared to insure.

That problem is not a small one, in practice. If it is right that, under Illinois Law, property which is in a defective condition triggers an insuring clause which requires “damage”, it gives rise to a risk that Builder’ Risk insurers in that jurisdiction (and other similar jurisdictions) will use another way to ensure that they aren’t required to pay for the cost of repairing defective but undamaged property. One way to do so would be to withdraw the availability of the more generous LEG clauses (LEG2 & LEG3), and restrict cover to LEG1, which excludes the cost of repairing any damage which is caused by mistakes of any kind. That would be a significant backward step for the Builders’ Risk market, and would be a terrible development for affected policyholders.

Fortunately, there is a simple fix, which is that if a Builders’ Risk policy is issued in a jurisdiction which, like Illinois, looks to the dictionary definition of damage if it isn’t defined by the policy, rather than to any of the damage authorities, then insurers and brokers need to ensure that their policies do include a definition of damage. I would suggest the following (other formulations are available):

“Damage means an accidental change in physical condition (whether permanent and irreversible, or transient and reversible) of insured property, which impairs either the value or the usefulness of that property”.

Is the meaning of LEG3 unambiguous?

Both policyholder and insurer argued that LEG3 was unambiguous. The policyholder argued that LEG3 unambiguously provided cover for the cost of repairing the honeycombed concrete components, and the insurer argued that LEG3 unambiguously excluded cover. The Judge disagreed with both parties, finding that “LEG3… is ambiguous, egregiously so”. Ouch (again). Is it, though?

Again, it is important to remember that the Judge was applying Illinois law to the question of ambiguity, and Illinois Law in this respect isn’t necessarily going to be the same as other jurisdictions. It certainly isn’t the same as the approach that would be taken by the English Courts, which only find that a clause is ambiguous if there are competing interpretations which the Court is unable to choose between. According to the Judge in SCB, however, under Illinois Law a clause is ambiguous if it is “subject to more than one reasonable interpretation”. That is a very low bar, and the Judge may well have been right that the low bar was met in this case. Of course, that does not mean that a Judge applying a different test, with a higher bar for ambiguity, wouldn’t have been able to make a finding about what LEG3 does actually mean. However, the SCB Judge’s (too) scathing comments about the drafting of LEG3 may have the positive effect of prompting a re-draft of the clause which addresses an issue with the clause which clearly exists in theory, but which thankfully I haven’t yet seen in practice.

The specific problem with the way in which LEG3 is drafted is that it mixes up causation on the one hand, and the condition of the relevant property, on the other. Defect exclusions should be concerned with either causation (which is the intended focus of LEG1 and DE1) or with the condition of the relevant property (which is the intended focus of DE2, DE3, and DE4), but not with both. The problem with LEG3 is that the exclusionary words which begin the clause (“all costs rendered necessary by [mistakes]…”) are concerned with causation. That part of the clause is a full exclusion for the cost of fixing mistakes of all types, whether workmanship, design, materials, specification, or plan, just as with LEG1 or DE1. There is then a write back (“should damage … occur to any portion if insured property containing any of the said defects…”) which brings back cover for the cost of fixing damage to insured property where the mistakes have been built into the works (with the end of the clause limiting the write back so that it only excludes improvement costs). The problem with that is that the write back is not expressed to extend to cover the cost of repairing damage caused by mistakes which are sustained by property which is not in a defective condition prior to the occurrence of the damage. A literal reading therefore suggests that LEG3 provides greater cover for the cost of fixing damage to defective insured property than it does for the cost of fixing damage to un-defective insured property. That was clearly not the intention of the LEG committee when drafting LEG3, and it is not how CAR insurers in the UK approach LEG3, but unfortunately it is what LEG3 actually says.

Given that damage is required to trigger the insuring clause of a Builders’ Risk policy then, as long as damage is properly defined, the cost of fixing defective but undamaged property should never trigger the insuring clause, and so does not need to be excluded. That being the case, the intention of the current LEG3 clause (which is to only exclude improvement costs) could be achieved by the following much simpler formulation:

“The insurer shall not be liable for that cost incurred to improve the original material workmanship design plan or specification”.

Wouldn’t the above formulation be much easier for policyholders to understand? Clearly yes. In my view nothing useful from the current clause would be lost, but I would be very interested to hearing from anyone who takes a different view (david.pryce@fenchurchlaw.co.uk).

Resolving the “ambiguity”

Having found that LEG3 was ambiguous, the consequence under Illinois Law was that the clause must be “construed against its drafter”, which in this case meant that the clause needed to be construed against the insurer, Lexington. That was the case notwithstanding that, of course, LEG3 is a standard clause that wasn’t in fact drafted by either of the parties in SCB, but by the LEG committee in London, and has been commonly used by parties to Builders’ Risk insurance policies across the world for more than a quarter of a century.

Outcome & final comment

Given the above, the Judge found wholly in favour of the policyholder. As a policyholder representative I can only applaud the effectiveness of the arguments made by SCB’s attorneys, but I am concerned about the potential for the outcome to have a negative effect on Builders’ Risk policyholders in the future. I hope the suggestions above can help those who, like me, want to ensure that doesn’t happen.

I’d like to finish with a final comment on a point that didn’t ultimately affect the outcome in SCB, but which touches on a point of general importance, which is the issue of how to assess improvement costs, which the Judge addressed in an interesting, and quite neat, way. What constitutes improvement costs is an issue that comes up frequently in practice, and there remains no clear guidance from the Courts on how improvement costs should be determined.