For better(ment) or for worse?

Allegations of “betterment” arise frequently in property claims, particularly where roofs, façades, cladding or other structural elements are ageing or incapable of repair on a strict like-for-like basis. Insurers often contend that replacement will leave the policyholder better off than before the loss, and that a deduction is therefore justified. That contention is not always well-founded.

In this article, Chloe Franklin of Fenchurch Law’s Property and Real Estate team considers how betterment issues commonly arise and, if so, how they should be addressed, with the answer turning on the policy wording, necessity, and evidence.

The Legal Starting Point

Property policies are rooted in the principle of indemnity. This principle was neatly described by Popplewell LJ in the Court of Appeal judgment in Sky UK Limited & another v Riverstone Managing Agency Limited & Others; “A contract of insurance against damage to property is a contract of indemnity, which is often described as a contract to hold someone harmless… in the sense that the insurer promises that the assured will not suffer the insured damage”

However, many operate on a reinstatement (replacement cost) basis, under which the insurer agrees to meet the reasonable cost of repairing, reinstating or replacing insured property damaged by an insured peril.

Betterment sits at the intersection of those principles. The insurer is not required to fund improvements, but equally, indemnity does not require reinstatement to replicate the damaged property in age or condition.

The critical question is whether the proposed works result in a material enhancement beyond that reasonably required to restore the property to its pre-loss position.

What Betterment Means in Practice

In property claims, insurers typically invoke betterment where reinstatement works are said to:

- increase value, durability, strength or useful life;

- introduce a higher specification than existed pre-loss; or

- go beyond what is required to reinstate the damaged property.

However, betterment is not established simply because:

- the damaged element was old;

- replacement produces something new; or

- modern materials or methods are required.

Those features are often inherent in reinstatement and, without more, do not justify a deduction.

Policy Wording: Typical Betterment Provisions

Betterment is ordinarily addressed within the Basis of Settlement provisions. While wordings vary, three common formulations arise.

- Reinstatement basis with “no betterment” proviso

The insurer will pay the cost of repair, reinstatement or replacement, but not any amount representing improvement beyond the condition immediately prior to the loss. - Express betterment deduction clause

A deduction may be made where reinstatement results in increased value, durability or useful life. - “Nearest equivalent” wording

Where identical materials are unavailable, the insurer will fund replacement using the nearest equivalent necessary to restore the property to substantially the same condition.

These provisions must be read together. A prohibition on betterment is frequently qualified by an acceptance that modern or equivalent materials may need to be used where like-for-like reinstatement is not possible.

What Betterment Is Not

Disputes framed as “betterment” often arise from a failure to distinguish between separate legal issues.

Pre-Existing Defects, Inherent Vice Or Deterioration

First, pre-existing defects, inherent vice or deterioration are matters of causation and scope of cover, not quantum. Where proposed works address deficiencies unrelated to the insured peril, those costs may fall outside cover. Where insured damage necessitates works which also address underlying defects, the correct approach is one of identification and, where possible, apportionment. It does not follow that the entire cost can be characterised as betterment.

Wear And Tear

Secondly, wear and tear exclusions operate at the coverage stage. They do not provide a mechanism for adjusting the measure of indemnity. Where an insured peril causes damage to property in a deteriorated state, the claim (if otherwise covered) proceeds on a reinstatement basis. Wear and tear cannot be reintroduced as a betterment deduction.

Unavoidable Replacement

Thirdly, unavoidable replacement does not constitute betterment. Where repair will not achieve a durable or functional reinstatement, replacement is the minimum necessary response. For example, where a flat roof is leaking and a simple repair would not resolve the issue, the only way to ensure the property is watertight is to replace the flat roof entirely. The fact that the insured receives a new asset with a longer remaining life is an inherent feature of reinstatement and does not, of itself, amount to a material enhancement.

Regulatory Compliance

Fourthly, compliance-driven works are often mischaracterised. Where compliance with current regulations is a necessary precondition to reinstatement, those costs form part of the reinstatement exercise (subject to policy wording). They are not elective improvements.

Modern Materials and Methods

Finally, modern materials and methods will often deliver improved performance relative to older systems. Where those materials represent the nearest reasonable equivalent, their use is contemplated by the policy and does not justify a deduction.

Properly analysed, betterment is a narrow concept, confined to cases where the insured obtains something materially beyond that required to reinstate the property to its pre-loss condition and function.

Practical Guidance for Brokers and Policyholders

Early engagement is critical. Insurers should be required to articulate their position clearly and with reference to the policy wording, but that unfortunately doesn’t always happen.

In order to reduce the risk of betterment arguments being raised by insurers, it is key that policyholders ensure that:

- pre-loss condition is evidenced through surveys, maintenance records and photographs;

- replacement (as opposed to repair) is properly justified;

- pricing distinguishes between core reinstatement and any enhanced specification; and

- elective improvements are clearly separated from insured works.

Conclusion

Betterment is a legitimate but limited concept in property claims. It is not a default consequence of age, replacement or the use of modern materials.

The distinction between reinstatement and improvement is critical. Only the latter engages betterment, and it is for insurers to identify and evidence it with precision.

Properly approached, betterment should remain a focused issue of quantum, not an obstacle to effective reinstatement

Author

Chloe Franklin, Associate

Aggregation in Cargo and Logistics Insurance Claims: What insurers must prove when aggregating by accident, occurrence or event

In our experience, aggregation clauses are among the most heavily contested provisions in cargo and logistics insurance. They govern whether multiple losses are treated as a single claim for the purposes of applying limits, deductibles, and sub-limits, often making the difference between meaningful recovery and severe underinsurance.

While insurers frequently assert aggregation where there is a run of thefts, shortages or logistics failures, English law does not permit aggregation by default. The outcome turns on policy wording, causation, and the factual coherence of the losses said to aggregate.

The Central Importance of Wording

Aggregation is not governed by a single legal test, but depends on the policy wording selected. English law distinguishes between:

- Event/occurrence wording, which is construed relatively narrowly; and

- Originating cause/source wording, which allows a much broader backward search in the causal chain.

Courts have repeatedly emphasised that an “event” is something that “happens at a particular time, in a particular place, and in a particular way” (see AXA Reinsurance (UK) plc v Field [1996] 1 WLR 1026 (HL)). By contrast, where a clause aggregates by reference to an “originating cause”, aggregation may extend to a continuing state of affairs or a common operational failure, as considered by Spire Healthcare Ltd v RSA [2022] EWCA Civ 17.

Cargo and logistics policies frequently sit closer to the former category, even when they use hybrid language that permits aggregating a series of accidents or occurrences.

Accident, Occurrence And Event: Distinct Concepts

In logistics policies, theft or loss of cargo is typically treated as an “accident” or “occurrence”, that is, a discrete fortuitous incident, often involving deliberate human conduct.

Where a policy allows aggregation of:

“a series of accidents or occurrences arising out of one event in any one location”

the structure of the clause matters.

In our view, the accident or occurrence remains the primary operative unit. The insurer must first establish that multiple losses can properly be described as arising out of one event (”event” being used here in the same functional sense as an ‘occurrence’, namely a specific happening in time and place) before aggregation can follow.

This hierarchy is critical, and it prevents insurers from eliding multiple independent thefts or interceptions into a single claim by appealing to a high‑level narrative (e.g. “organised crime”, “systemic theft”, “criminal gangs” etc.) divorced from the actual incidents.

Series of Losses

Secondly, on the above wording, insurers must prove that the multiple losses are a “series”; in other words that there is some connection between the thefts and they are not simply a number of unconnected happenings.

What Insurers Must Prove: The Legal Burden

Where aggregation is relied upon in relation to the number of limits applicable, the burden lies squarely on insurers to prove that the losses aggregate. To aggregate multiple cargo losses by reference to accident, occurrence or event wording, insurers must demonstrate the following:

- A Single Identifiable Event

Insurers must identify one event capable of unifying the losses. This cannot be merely a shared background risk or an industry‑wide problem. The courts have consistently rejected attempts to aggregate by reference to general conditions, vulnerabilities or ongoing criminality.

As the Supreme Court held in AIG Europe Ltd v Woodman [2017] UKSC 18, losses must be connected by more than similarity or coincidence; there must be a real inter‑connection such that they “fit together”, rather than being linked only through external background factors.

An assertion that multiple thefts were committed by an organised crime group is not sufficient unless the insurer can point to a specific operative event, for example, a single coordinated operation, decision or execution, rather than a series of similar opportunistic crimes.

- Causation: Losses Must “Arise Out of” That Event

Even if an event is identified, insurers must show that each loss arose out of it. This incorporates orthodox principles of legal causation.

Courts have repeatedly warned against treating the causal language in aggregation clauses as infinitely elastic.

In logistics contexts, where thefts occur:

- days or weeks apart,

- at different depots or distribution centres,

- involving different carriers or routes,

it becomes increasingly difficult for insurers to demonstrate that each loss arose out of the same event rather than out of separate, self‑contained criminal acts.

- Unity of Time, Place and Circumstances

Although not a rigid checklist, the “unities” analysis remains a powerful analytical tool where aggregation turns on event or occurrence wording.

Following Kuwait Airways Corp v Kuwait Insurance Co SAK [1996] 1 Lloyd’s Rep 664, courts typically examine:

- Unity of time – Were the losses contemporaneous or closely proximate?

- Unity of place – Did they occur at the same or related locations?

- Unity of cause – Were they caused by the same operative act or incident?

- Unity of intent – Where human action is involved, was there a single purpose or plan?

Where cargo losses are dispersed across time and geography, and where no single coordinated operation can be demonstrated, these unities are unlikely to be satisfied. Similarity of method, or repetition of thefts along a supply chain, is not enough.

- “One Location” Means What It Says

Many logistics policies restrict aggregation to losses arising from “one event in one location”. This is a significant limiting factor.

Insurers must demonstrate not only a single event, but a single location in a meaningful sense. Attempts to characterise an entire logistics network, route corridor, or regional supply chain as “one location” have little support in English law. Policyholders are entitled to insist on a physical and geographical reality, assessed from the standpoint of a reasonable observer, not by reference to the insurer’s preferred level of abstraction.

Common Insurer Arguments and Their Weaknesses

Insurers frequently argue that multiple cargo thefts form part of:

- a single criminal enterprise,

- a continuing modus operandi, or

- a sustained campaign against the insured.

These arguments may carry more weight under originating cause wording, but under event‑based formulations, they face real difficulty. As the courts made clear in Woodman, similarity is not connection, and a shared background explanation does not establish a unifying event.

Even where organised crime can be shown, that does not compel total aggregation.

English law permits partial aggregation or clustering where appropriate, recognising that separate events may exist within a broader narrative.

Practical Implications For Policyholders

For policyholders facing aggregation assertions in cargo and logistics claims:

- Ensure that insurers identify the specific event relied upon.

- Test whether causation genuinely runs from that event to each loss.

- Scrutinise unity of time, place and circumstances.

- Resist attempts to substitute high‑level descriptions for factual proof.

Aggregation is not achieved by labelling losses as “systemic”. It must be earned by evidence.

Author

Toby Nabarro, Director, Singapore

Mind the Gap: Owners Corporation 1 Plan No. PS 640567Y v Shangri‑La Construction Pty Ltd [2026] VSC 117

Introduction

A recent decision of the Supreme Court of Victoria poses an important question for the construction sector in particular: where statutory and/or strict liability regimes which concern actions taken by directors or officers are not covered by professional indemnity (“PI”) insurance, is directors’ and officers’ (“D&O”) insurance able to plug any gap in cover?

Background

Shangri‑La Construction Pty Ltd (“SCP”) was appointed to design and construct a residential development in Victoria, Australia. SCP’s Managing Director, Mr Naqebullah, recommended that the external façade incorporated expanded polystyrene (“EPS”) cladding, which was later determined to be non‑compliant with applicable building regulations. Following remediation works funded by the State of Victoria (the “State”) (similar to the Building Safety Fund here in England & Wales), it pursued an action to recover such costs under Section 137F of the Building Act 1993 (Vic) (“Section 137F”), which was enacted in 2019. Section 137F is a strict liability provision which grants the State rights of subrogation against officers and/ or directors of contractors for the cost of cladding rectification work.

Pursuant to Section 137F, the State obtained summary judgment against Mr Naqebullah in the sum of approximately $3.17 million plus interest. Mr Naqebullah then sought indemnity under two consecutive “claims made and notified” professional indemnity policies taken out by SCP (the “Policies”).

Key questions

The Court was required to determine:

- Whether Mr Naqebullah was an “Insured” under the Policies;

- Whether a “Claim” had been made and notified within the relevant periods of insurance; and

- Whether the liability fell within the insuring clause, which responded to civil liability incurred in the conduct of the insured’s professional business.

Judgment

Insured status

The Court held that Mr Naqebullah was an insured person under the Policies. Although he was not named individually on the certificates of insurance, the policy documents, read as a whole (including the proposal forms), demonstrated that directors were intended to fall within the class of insureds.

Claims made and notified

The Policies were written on a strict claims made and notified basis. However, the State’s ability claim under Section 137F did not come into force until after the expiry of the Policies. As a result, and unsurprisingly, the Section 137F claim against Mr Naqebullah could not have been made during the relevant periods of insurance. Moreover, attempts to treat earlier proceedings involving SCP as the relevant claim, or to attach the Section 137F claim back to earlier notifications, were rejected as undermining the commercial purpose of claims made insurance.

Scope of the professional indemnity cover

Most interestingly from our perspective, the Court found that the liability imposed on Mr Naqebullah was not incurred in the conduct of professional business. “Professional Business” was defined by the Policies as design, including advice in relation to design in accordance with all relevant building, construction or engineering codes and standards.

It was Mr Naqebullah’s case that providing services as a registered building practitioner in drafting a specification under a design and construct contract constituted the provision of professional services of a skilful character as contemplated by the Policies.

However, no element of the State’s case against Mr Naqebullah involved provision of any design, specification or advice as contemplated by the “Professional Business” definition under the Policies, nor did Mr Naqebullah’s liability to the State depend in any way upon breach of a professional duty by him or by SCP. Instead, his liability arose solely (and strictly) under Section 137F as he was an officer of SCP at the time of the non‑compliant work.

Analysis and implications

This decision highlights an area of tension between statutory and/or strict liability regimes and professional indemnity insurance. Even where the factual background involves professional services, insurers will inevitably look closely at the legal basis on which liability is imposed. Where that basis arises in statute and/or by strict liability, PI insurance policies may not respond.

When that liability concerns actions taken by directors or officers, the question then becomes whether D&O insurance is able to plug any gap in cover.

Whilst there are no analogous strict liabilities directly arising from the design or construction of buildings here in England & Wales, sections 40 and 161 of the Building Safety Act 2022 (the “BSA”) did introduce offences for officers who commit, consent to or negligently fail to prevent breaches of the Building Act 1984 (including contravention of the Building Regulations) and breaches of Part 2 or Part 4 of the BSA (including obstructing building control or failing to manage Higher Risk Buildings).

While liability imposed on an individual by virtue of holding office might ordinarily be expected to fall within the scope of D&O insurance, such policies often contain broad professional services exclusions. This creates a real risk that policyholders may find themselves without cover under either policy.

Conclusion

For policyholders and brokers, the decision underlines the importance of reviewing PI and D&O cover together, rather than in isolation. Particular attention should be paid to the scope of the professional services definition and insuring clause alongside the breadth of professional services exclusions in D&O policies, and the extent to which programmes are designed to respond coherently to building safety liabilities.

Authors

Abigail Smith, Associate

Pawinder Manak, Trainee Solicitor

Ten years on: has the Insurance Act 2015 actually delivered for policyholders?

The Insurance Act 2015 (“the IA 2015”) was introduced to level the playing field for insurers and policyholders, and to move away from outcomes that were perceived as outmoded.

As the IA 2015 approaches its 10-year anniversary, this article will examine whether it has achieved those objectives – with particular focus on property damage claims – as well as the areas where uncertainty remains.

Duty of fair presentation: a shift in framework, as well as insurer behaviour?

One of the central reforms introduced by the IA 2015 was the introduction of proportionate remedies for breaches of the duty of fair presentation, which replaced the previous draconian “all or nothing” regime. In principle, this marked a significant and welcome shift. In practice, however, disputes concerning fair presentation and remedies remain common, particularly in the context of property damage claims.

A common example arises where, for example, following a fire, insurers allege that the policyholder failed to disclose historic alterations to the property, deficiencies with electrical compliance, or that one of its directors had previously been involved with insolvent companies. Had these matters been disclosed, insurers may assert that they would have only agreed to insure the policyholder on different terms or, as is more often the case, that they would not have agreed to insure the policyholder at all.

Insurers have increasingly sought to characterise alleged breaches of this nature as deliberate or reckless, thereby entitling them to avoid the policy outright (as well as keep the premium and refuse all claims), whilst sidestepping a detailed analysis of what they would have done differently. The result is that, rather than reflecting a fundamental change in behaviour, some claims handling practices have adapted tactically to fit within the structure of the IA 2015.

As a matter of law, the evidential burden remains firmly on insurers. It is for them, not policyholders, to prove how the alleged non‑disclosure or misrepresentation influenced their underwriting. In practice, insurers are frequently reluctant to disclose the evidence said to support their position, such as contemporaneous underwriting guidelines, contemporaneous exchanges at the time of placement, or a witness statement from the underwriter involved. In those circumstances, policyholders are left with an invidious choice: they can either accept the insurer’s position at face value, or commence litigation without fully understanding the strength of the case they must meet. Neither outcome sits comfortably with the intended purpose of the IA 2015, particularly in high‑value property damage claims where the consequences of avoidance can be severe.

Section 11 – a causation test, or not?

Section 11 of the IA 2015 (“s.11”) was intended to prevent insurers from declining claims on the basis of technical breaches of policy terms that had no connection with the loss. In straightforward cases, its application is uncontroversial. A breach of a fire alarm warranty should not entitle an insurer to avoid liability for a flood loss, just as a failure to maintain a burglar alarm should not defeat a claim for storm damage.

More complex property damage claims, however, expose the underlying difficulty in applying s.11 ie., where the breach can be shown not to have caused the loss per se, but it is harder to say that compliance could not have reduced the risk of that loss in different circumstances. So, for example, a failure to comply with a condition to store combustible waste in a particular place might not have caused a fire, but it nonetheless could have done. This gives rise to a fundamental question: does s.11 require a strict causation test, or is it sufficient that compliance with the term could theoretically have reduced the risk of the loss occurring?

The Law Commission appeared to favour a non‑causation approach ie., they said that the test is whether compliance could realistically have affected the loss that actually occurred, rather than requiring a strict causation analysis. However, the wording of s.11 focusses on whether the breach “could not have increased the risk of the loss which actually occurred in the circumstances in which it occurred”. That language strongly suggests that there is, in fact, an element of causation, because the emphasis is on the way in which a particular loss occurs. In practice, this shifts the inquiry toward a counterfactual assessment of whether compliance with the relevant term could have made a difference. So, in the context of an alleged breach of a requirement to carry out a 30‑minute fire watch following hot work, it would be open to a policyholder to assert that the breach could not have made any difference if fire did not break out until three or four hours later.

The High Court’s decision in Mok Petro Energy Ltd v Argo (No.2) [2024] EWHC 1935 (Comm) is the first decision on s.11. However, the provision was dealt with only briefly, and no more than a few paragraphs. The court’s observation – that the correct question is whether compliance with the term as a whole could have reduced the risk of the loss – was obiter, and not central to the outcome of the case. While the comments are nonetheless of interest (and are now frequently relied upon by insurers to reject a causation analysis), they fall short of providing definitive guidance. As a result, considerable uncertainty remains.

Damages for late payment: the theory and the reality

Section 13A of the IA 2015 (“s.13A”) introduced a statutory right for policyholders to recover damages for the late payment of insurance claims. For example, following a major fire loss, an insurer may decline cover and take many months to investigate and maintain that position, during which time the policyholder is unable to fund reinstatement and suffers continuing business interruption losses. If it is later established that the insurer had no reasonable basis for its declinature, s.13A would, in principle, entitle the policyholder to claim damages for losses flowing from that delay, such as additional loss of profits, or increased reinstatement costs.

In theory, s.13A represents a significant shift in the balance between insurers and policyholders, with the aim of discouraging unreasonable delays. In practice, however, its impact has been limited so far.

The threshold for a successful claim under s.13A is a demanding one. It is not enough for a policyholder to establish that an insurer was wrong to deny or delay payment of a claim; the policyholder must also prove that the insurer acted unreasonably. Where an insurer can demonstrate that it had “reasonable grounds” for disputing the claim, liability under s.13A will not arise, even if the coverage position is later shown to be wrong. This creates something of an asymmetry: a relatively low bar for insurers to resist liability, and a correspondingly high bar for policyholders seeking to recover losses caused by delay.

That imbalance is particularly acute in property damage claims. Following fires, or escapes of water, insurers often rely on extended investigations into causation, compliance with policy terms, or alleged non‑disclosure as giving rise to “reasonable grounds” to investigate a claim. While some degree of investigation is plainly required, the availability of “reasonable grounds” as a defence under s.13A offers insurers considerable latitude to justify prolonged delay.

There are also significant practical constraints. Claims for s.13A damages are evidence‑heavy, requiring detailed scrutiny of the insurer’s decision‑making process and the reasonableness of the time taken. Policyholders must also continue to comply with their duty to mitigate loss, which can be particularly challenging where reinstatement cannot happen without funding. As a result, the remedy is costly to pursue and, in many cases, commercially unattractive. It also raises the question as to whether well-resourced policyholders, who might be able to mitigate more easily, are able to establish claims for s.13A damages at all.

The case law reflects these difficulties. For example, in Quadra Commodities SA v XL Insurance Co SE [2022] EWHC 431 (Comm), the court suggested that a period of “not more than about a year” was reasonable for a complex claim. While that is helpful in principle (particularly as a benchmark against which delay in straightforward claims might be assessed), the policyholder ultimately lost its s.13A claim because the insurer was found to have had reasonable grounds for disputing coverage.

To date, there have been no successful reported claims under s.13A, and its effectiveness in future claims will depend, amongst other things, on the courts’ willingness to draw firmer lines around what constitutes an unacceptable delay. Until then, damages for late payment claims are likely to remain more of a strategic lever than a routinely deployed remedy.

A developing framework

While there has been meaningful case law in relation to the duty of fair presentation, other aspects of the IA 2015 remain comparatively underdeveloped. In particular, further authoritative case law on s.11 is needed to resolve the continuing uncertainty as to its proper application, especially in complex property damage claims where issues of causation and risk frequently overlap.

Similar uncertainty surrounds s.13A, and in particular the threshold for what constitutes “unreasonable” grounds for refusing or delaying payment of a claim. Absent any successful reported claims under s.13A, its true potential as a remedy for policyholders remains to be seen.

A decade on from its introduction, the IA 2015 has unquestionably reshaped the legal framework governing commercial insurance disputes. However, it has not eliminated all of the underlying tensions between insurers and policyholders. Further case law, particularly in relation to s.11 and s.13A, will be critical in determining how the IA 2015 operates in practice over the next decade.

Author

Alex Rosenfield, Partner

Levelling the Playing Field?: the Impact of Section 13A, almost a decade on

Despite having been introduced almost nine years ago, the impact of section 13A remains to be seen. In this article, we consider whether it has achieved its purpose of levelling the playing field for policyholders, or whether it has fallen short of the reform that was originally promised.

A (brief) history

Section 13A of the Insurance Act 2015 (the “Act”) was enacted by section 28(1) of the Enterprise Act 2016 and came into force on 4 May 2017. It introduced an implied term into every contract of insurance that the insurer must pay claims within a reasonable time (including time to investigate and assess the claim) and marked a significant development in UK insurance law.

To date however, there have been only two section 13A claims heard by the courts, both of which have failed: in Quadra Commodities S.A v XL Insurance Co SE and Others [2022] because the insurer succeeded in presenting a “reasonable grounds” defence, and in Delos Shipholding SA & Ors v Allianz Global Corporate and Specialty SE & Ors [2024] because the insured had failed to establish its loss.

You can read our analysis of Quadra here – Better late than never: the first reported case on damages for late payment - Fenchurch Law.

While limited inferences can be drawn from the outcomes of only two claims, there are some obvious challenges to policyholders wanting to pursue these claims.

We consider those challenges below.

What is a “reasonable time” in which a claim should be paid?

The first issue is that the burden of proof is on the insured to demonstrate that the insurer failed to pay within a reasonable time.

The Law Commission Report, and the Explanatory Notes to the Enterprise Act, make it explicit that a reasonable time will always include a reasonable time for investigating and assessing a claim, that claims under business interruption policies will usually take longer to value than claims for property damage, and that larger more complicated claims will take longer to assess than straightforward claims.

In Quadra the Commercial Court commented that assessing what was a reasonable time was “not an easy one to decide”. The facts involved transport and storage operations across different jurisdictions and there were a number of factors outside of the insurers’ control including the destruction of evidence and the fact that legal proceedings had been issued in another jurisdiction three years prior.

The good news for policyholders was that, even in what the Court termed “complicated circumstances”, it was found that a reasonable time was not more than about a year from notification: the inference being that more straightforward losses should be paid in a number of months.

However, the challenge remains that, in circumstances where the insurer has reasonable grounds for defending the claim (in respect of liability and/or quantum), a section 13A claim may not succeed even in circumstances where an insurer has failed to pay the claim within that period.

When is an insurer both wrong and unreasonably wrong?

It was on that basis that, in Quadra, insurers successfully defended the insured’s section 13A claim, despite the insured’s coverage claim succeeding at trial.

The Commercial Court found that insurers had reasonable grounds for disputing the claim and that their arguments on policy coverage were not unreasonable merely by virtue of being mistaken.

Whilst the court can take into account insurer’s conduct in handling the claim, Quadra makes clear that slow claims handling, unnecessary investigations and improper construction / application of the policy terms will not be enough to deprive an insurer of the “reasonable grounds” defence.

So what kind of conduct would operate to deprive an insurer of a defence?

In Quadra, the Court found that insurers had instructed a loss adjuster, and sought legal advice, within the “reasonable time” for paying the claim, which suggests that not to have done so would be unreasonable. In addition, the Explanatory Notes to the Enterprise Act tell us that it will be unreasonable if an insurer is slow to change its position when further information confirming the validity of the claim comes to light.

Importantly, it is also necessary for the insured to highlight the insurer’s unreasonableness: in Quadra, the Court commented that the insured had not attempted to rebut the insurer’s argument that it had reasonable grounds to defend the claim.

Establishing loss – do pecunious policyholders have poorer prospects of succeeding under s13A?

In Delos, the claimant, who was the registered owner of a detained bulk-carrier, argued that it had suffered a loss of opportunity as a result of the insurer’s failure to pay the claim within a reasonable time, because the insurance funds would have been used to purchase a replacement vessel, which could have been traded at a profit.

The Court noted that no evidence had been adduced to show that the Claimant had been serious about pursuing that opportunity (by way of correspondence or a business plan, for example) and therefore it had not established its loss.

Controversially, Mrs Justice Dias commented that there was force in the argument that, because the Claimant was a profitable group and could have purchased a vessel without the benefit of the insurance proceeds, it had not incurred a loss as a result of the insurer’s alleged failure to pay the claim within a reasonable time.

That begs a further question: do policyholders with deeper pockets (for example, blue-chip companies) have poorer prospects of succeeding under section 13A, because of their ability to mitigate their own loss?

Arguably, yes, although there are no reported decisions on this issue. In Quadra, the Commercial Court emphasised that s13A damages are not automatic and must satisfy strict causation and mitigation standards, meaning that a claimant cannot recover loss which it could reasonably have avoided.

In other words, section 13A may operate most effectively where late payment renders a claimant impecunious, because causation and mitigation is easier to establish in such cases.

Suitability of Section 13A claims for preliminary hearings

Recently in The Members of The Probitas Syndicate 1942 at Lloyd’s -v- Pro 2 Care Limited [2025], the Commercial Court refused to consider a Claimant’s section 13A claim at a preliminary hearing, advising that evidence is crucial to assessing the period of the delay, and any loss.

In presenting its claim under section 13A, the Claimant, a care home business, argued that it had taken about 19 months for the insurer to pay its property damage claim, which was unreasonable by about 11 months (8 months having been sufficient to investigate and assess the claim), causing losses in excess of £2 million. It argued that, had the claim been paid sooner, repair works would have commenced and completed, and revenue would have been earned. In contrast, the insurer argued that the Claimant had not set out the basis for unreasonable delay, and relied on the fact that it had made staged interim payments as and when elements of the claim had been evidenced and accepted by its loss adjuster.

At a summary judgment hearing, the judge commented that, although the Claimant’s claim under section 13A was “clearly arguable”, claims under section 13A are a paradigm example of factual disputes which require evidence, and cannot be resolved summarily.

We query whether arguably this might present a further hurdle for policyholders if it can be inferred from the fact that the case has gone to trial that the insurer must have a reasonable basis to defend the claim, even if that defence ultimately fails, as otherwise the claim would likely have settled.

Conclusion

Almost nine years on, it is hard to see that section 13A has – yet – succeeded in levelling the playing field for policyholders.

Nevertheless, the optimistic view is that, in different circumstances, the path has been laid for section 13A claims to succeed. If the precedent set by Quadra is that even complicated claims should be paid within a period of 12 months, the real challenge lies in contesting an insurer’s “reasonable grounds” defence.

Despite the apparent hurdles, section 13A claims remain a powerful negotiating tool for policyholders in disputes with insurers. No insurer wishes to be the first to be subject to a successful damages claim for late payment, or to risk establishing a precedent which is unfavourable to the market.

For that reason, even almost a decade on, the jury is out; and only time will tell.

Author

Abigail Smith, Associate

The Iran War: Property and Business Interruption Insurance Implications for Policyholders

The ongoing Middle East conflict has significant implications for many insurance issues facing policyholders. In the first of a two-part series, our partners Julian Teoh and Chris Wilkes highlight areas of concern for downstream policyholders outside of the conflict zone, and what these potentially affected policyholders should be looking out for.

Physical Damage Insurance

The effective closure of the Strait of Hormuz and Iranian attacks on energy infrastructure across the Middle East has resulted in a shortage of oil and gas and a spike in energy and related prices.

Energy price spikes are already translating into significant increases in the costs of reinstatement and rebuilding property which has been damaged.

- Petroleum-based materials such as waterproof membranes, paint and sealants have become more expensive as oil prices surge.

- Increased costs of insurance and shipping (due to increased fuel costs and the need to take longer routes to avoid the warzone) will also be baked into the end price of building materials.

- Large cranes consume large amounts of fuel. Coupled with labour shortages, crane hire rates have increased significantly since the start of the conflict.

- Energy costs feed directly into the cost of raw materials e.g. steel and aluminium, not to mention inflation causing a general increase in prices across the board, plus shortages of supply compounding price increases (and delay in supply).

The impact on supply chains is also likely to be severe, leading not only to increased direct costs, but also prolonged time scales for deliveries leading in turn to time inflation and related indirect costs.

It would be prudent for policyholders and their brokers to re-examine their physical damage sums insured under property, machinery and construction policies to reflect these issues. Policy average / under-insurance clauses can be applied even in partial loss situations, proportionately reducing any indemnity due under the policy.

Business Interruption and Increased Costs of Working Cover

Most operational policies contain cover for business interruption following damage and increased costs of working (ICW). In short, ICW are the additional costs incurred by the policyholder to mitigate BI losses (which may be highly relevant if there are delays in the supply of components or materials).

ICW cover is subject to various tests, including the “economic test”: the increase in costs must be less than the reduction in turnover due to the incident (i.e. the saving must exceed the cost of the additional expenses). In other words, uneconomic expenditure will not be covered.

Where the costs of inputs are spiking, it would normally be more difficult to pass this economic test. Policyholders will need to consider the interaction between cost and time-related savings when considering such mitigating measures.

Business Interruption (BI) Insurance

Non-Damage BI Extensions

Many BI policies contain non-damage BI extensions, i.e. they allow the policyholder to make a BI claim even where there has not been damage at the policyholder’s premises. Most relevant to the current conflict would be:

- Suppliers’ extensions: BI resulting from supply chain disruptions at suppliers.

- Denial of access: BI resulting from an inability to access the policyholder’s premises.

- Public authority order: BI resulting from an order from a civil or military authority.

The coverage triggers for these extensions is usually damage, whether at the premises of the supplier, within a certain radius of the policyholder’s premises or which has caused the authority to issue the order. But this is not inevitably the case. Especially in bespoke wordings, the coverage triggers may be far more permissive, and policyholders are encouraged to review their non-damage BI extensions.

Where the coverage triggers are damage-based, the policy’s war risks exclusion will also come into play. While these exclusions can be quite comprehensive, we would encourage policyholders to review the wordings carefully and seek advice on whether or not the exclusion applies.

Adequacy of BI Indemnity Periods

The BI indemnity period is the period for which the insurer agrees to indemnify the policyholder during which the interruption to business is ongoing.

If, for example, the policy BI indemnity period lasts for 12 months but the interruption persists for 18 months, the insurer is required to pay an indemnity for only 12 months. The policyholder would not enjoy any cover for its BI losses for the last 6 months.

If the conflict is prolonged and materials are in short supply and/or cannot be shipped to the premises in a timely manner due to the conflict or the knock-on effects, this may result in the interruption period extending beyond the policy’s BI indemnity period. In situations where critical parts of complex machinery are needed for the business to resume and are difficult to source in a timely manner, the shortfall between the indemnity period and the duration of the interruption will come into sharp focus.

Authors

Julian Teoh, Partner

Chris Wilkes, Partner

Insurance amid uncertainty: Implications of the Iran conflict for Policyholders

On 28 February 2026, the US and Israel launched a coordinated military operation against the Iranian regime. Iran has since responded with missile and drone attacks across the Gulf, creating risk across several major trading centres including Qatar, Bahrain, Oman, Saudi Arabia and the UAE.

In addition to the very real and devastating risk to life, the escalation of the conflict is causing significant disruption to global trade, transport and energy markets alongside extensive physical damage to insured property.

Below, we consider the implications of the conflict for policyholders across key classes of business, and the coverage disputes that may arise as claims emerge.

STANDARD WAR EXCLUSIONS IN PROPERTY INSURANCE POLICIES

Standard commercial property policies typically exclude damage or loss “directly or indirectly” caused by “war, invasion, acts of foreign enemies, hostilities (whether war be declared or not)…military or usurped power”, and whilst the parties to the conflict are yet to formally declare war, whether the conflict amounts to war under the rules of contractual interpretation is a separate question.

Since the 1930s, English courts have said that “war” does not have a technical meaning and should be interpreted in a “common sense way”. Since then, caselaw has provided deliberately wide guidance as to the definition of war, including the presence of opposing sides and the number of combatants involved.

The breadth of that definition, together with standard war exclusions which override the concept of proximate cause (by applying to damage / loss even indirectly caused by war), mean that many commercial insureds are without the benefit of war-related property cover under their standard property insurance policies. An unwelcome consequence of that is that significant business interruption losses following airport closures, port shutdowns, supply chain disruption and government restrictions are likely to fall outside of the scope of cover.

Much will depend on the precise wording of the exclusion and the factual matrix of the loss. We recommend that property and business interruption policies be scrutinised for war exclusions as soon as possible and, in addition, policyholders across the leisure and manufacturing industries assess their force majeure exposure under supply and services contracts.

THE “GRIP OF THE PERIL” DOCTRINE IN AVIATION AND MARINE INSURANCE

In light of the above, policyholders may look to recover under specific political violence / war risk insurance policies and extensions.

In June last year, we reported on the long awaited Russian aviation judgment handed down by the Commercial Court. The trial involved the detention of Western-leased aircraft following Russia’s invasion of the Ukraine in 2022. You can read our analysis of that decision here - Commercial Court grounds War Risks insurers in landmark Russian aircraft judgment - Fenchurch Law.

Of particular concern to policyholders was Mr Justice Butcher’s commentary on “the grip of the peril” doctrine. He held that:

“if an insured is, within the policy period, deprived of possession of the relevant property by the operation of a peril insured against and, in circumstances which the insured cannot reasonably prevent, that deprivation of possession develops after the end of the policy period into a permanent deprivation by way of a sequence of events following in the ordinary course from the peril insured against which has operated during the policy period, then the insured is entitled to an indemnity under the policy.”

He concluded that lessors whose cover had been terminated by insurers prior to the point at which the court considered they had been permanently deprived of the aircraft were entitled to cover, on the basis that the loss of the aircraft arose in a sequence of events that followed in the ordinary course of restraints and detentions that took place in the policy period. In other words, the aircraft were in the grip of the peril by the time the relevant policies were terminated.

That ruling may be of particular relevance to aviation and marine policyholders affected by the present conflict. As a result of the closure of airspace, airline fleets remain grounded across the Gulf. Those fleets are at considerable risk of being permanently lost as a result of missile strikes on airports in Dubai, Abu Dhabi, Bahrain and Kuwait. Whilst the market will no doubt issue review notices to terminate or vary cover in those instances (as they did in the Russian aviation case), its possible that insured aircraft may already be deemed in the grip of the peril depending on the precise factual and temporal sequence of events.

Similarly, in relation to marine insurance, standard hull and cargo policies also exclude war and political perils. As a result, shipowners and charterers trading in high‑risk areas typically rely on separate war risks policies which are cancellable on short notice, requiring vessels to leave designated danger zones within a defined period. We know that cancellation notices have already been issued in respect of the current conflict so, where those vessels are unable to leave for whatever reason (for example, as a result of port closures or government restrictions), the grip of the peril doctrine may become relevant.

Whilst that analysis may offer some comfort to certain policyholders with property in the conflict zone, political violence policies include their own standard exclusions, and losses caused by perils not purchased will be excluded in any event. If, for example, an insured has only purchased terrorism or civil unrest cover, they are likely to be uninsured for war-related losses.

We recommend that political violence and war risks cover be analysed immediately, alongside the delay provisions in any related sale and trade contracts.

AGGREGATION WORDING

Where losses are covered, significant disputes may arise in relation to aggregation. Iran’s missile and drone attacks have, to date, been segmented and geographically dispersed, raising questions as to whether losses arise from a single event, a series of related events, or multiple separate occurrences for the purposes of policy limits, deductibles and excess erosion.

Whilst the outcome of any dispute is likely to be driven by the aggregation wording in a specific policy, insurers are likely to argue for a narrow interpretation and policyholders should be alive to that issue.

POLITICAL RISK AND TRADE CREDIT INSURANCE

Finally, unlike political violence policies, political risk policies do not require physical damage to trigger cover. They insure against, for example, the confiscation or deprivation of assets and are concerned with the permanent or prolonged loss of rights in, or control over, those assets. Outcomes under these policies are likely to be driven by the definition of expropriation, whether the deprivation is permanent for the purpose of the policy terms, and any relevant waiting periods.

Also written within the political risk market is trade credit insurance. As the conflict progresses, disruption to energy sources and supply chains may impact a policyholder’s ability to perform its payment obligations under a contract. In those circumstances, whilst trade credit policies are likely to contain fewer war exclusions than property or marine policies, policyholders may still have challenges to overcome in relation to causation and aggregation.

CONCLUSION

Already, the market is taking steps to limit its exposure to the conflict by making amendments to certain wordings, and issuing cancellation notices in respect of hull and cargo. Policyholders would be well placed to undertake early analysis of policy terms, particularly in relation to relevant exclusions and the likely interpretation of aggregation wording. Early, careful engagement with policy wording and claims strategy will place policyholders in the strongest possible position as the insurance consequences of the conflict continue to unfold.

Author

Daniel Robin, Managing Partner

Abigail Smith, Associate

Legal 500 Insurance Disputes Comparative Guide – 3rd Edition (UK Chapter)

The 3rd Edition of The Legal 500: Insurance Disputes Comparative Guide has now been released. The guide offers a practical overview of insurance disputes law and practice across multiple jurisdictions, highlighting key issues shaping the landscape today.

Fenchurch Law is pleased to contribute once again. Daniel Robin and Chloe Franklin authored the United Kingdom chapter.

Each chapter provides insights into current trends in insurance disputes, covering topics such as insurance policies, dispute resolution, appeals, claims and causation, along with commentary on future developments in the field.

View the UK chapter here: https://www.legal500.com/guides/chapter/united-kingdom-insurance-disputes/

When Policies Collide – Untangling “Other Insurance” Clauses

At our recent London Symposium, Associate Abigail Smith discussed the potential challenges posed by other insurance clauses in insurance policies. The session covered:

- The genesis of these clauses;

- The types of other insurance clauses used to limit an insurer’s liability in the event of double insurance; and

- How competing other insurance clauses are interpreted, in practice.

What is double insurance?

Double insurance occurs when the same party is insured with two or more insurers in respect of the same interest on the same subject matter against the same risk. In other words, it occurs where an insured’s loss is covered under two or more separate policies. Whilst it can be a commercially prudent guard against insurer insolvency, it most often arises inadvertently (for example, where a composite policy overlaps with dedicated cover).

The common law position

Under common law, a policyholder that is double insured for its loss can claim against whichever policy or policies it chooses, in whichever order it chooses, subject to each policy’s limits. Then, to ensure the risk is fairly distributed between insurers, the paying insurer is entitled to claim a contribution from the non-paying insurer (a principle known as rateable contribution – Drake v Provident [2003]).

Industry challenges

Unfortunately, the common law position gives rise to some complicated issues.

The main issue is that, because there is no general rule or common law duty requiring a policyholder to disclose that it is double insured, unless an insurer asks the question directly, or notification of other insurance is a condition of the policy, a paying insurer may not be aware that they are entitled to claim a contribution.

Adding another layer of complexity, the limitation period for bringing a contribution claim is two years from the date that the right accrued under section 10(1) Limitation Act 1980. That date, which is likely to be the date of a judgment, settlement or arbitration award, is not necessarily when an insurer becomes aware that they are entitled to a contribution. In fact, with no duty to disclose, it is possible for limitation to expire without an insurer ever knowing that it had been entitled to a contribution.

Types of “other insurance” clauses

It was in recognising these challenges that the industry came up with a solution: other insurance clauses, which are standard clauses in insurance policies which limit an insurer’s liability in circumstances where another policy covers the same loss.

In The National Farmers Union Mutual Insurance Society Limited v HSBC Insurance (UK) Limited [2011], Gavin Kealey KC identified 3 main types of other insurance clauses, being:

- Escape Clauses – those that exclude cover altogether in the event that another policy covers the same loss.

- Excess Clauses – those that state that the policy will only respond in excess of any other insurance.

- Rateable Proportion Clauses – those that limit an insurer’s liability in proportion to the total cover available.

Abigail explored how each type of clause is interpreted, and how competing clauses interact, in practice.

Escape Clauses

Owing to the fact that Escape Clauses seek to exclude cover altogether in the event of double insurance, there was at the outset the potential for policyholders to be left without any cover at all where two or more policies each included an Escape Clause.

That issue was addressed in Weddell v Road Transport [1932], with the Court ruling that it would be unreasonable to leave a policyholder without any primary cover in circumstances where multiple policies were in place and multiple premiums had been paid. As such, where two or more policies include an Escape Clause, they will cancel each other out so that the policyholder can claim against whichever policy (or policies) it chooses (essentially reverting to the common law position).

Excess Clauses

The same question was more recently considered in Watford Community Housing v Athur J Gallagher Insurance Brokers Limited [2025], this time in respect of Excess Clauses. Ultimately, the Commercial Court held that, because Excess Clauses also seek to avoid primary liability in the event of other insurance, they cancel each other out in the same way that Escape Clauses do.

Escape Clause v Excess Clause

Whilst there’s no English authority addressing a scenario in which two or more policies include competing Escape and Excess Clauses, Australian caselaw does provide some assistance.

In Allianz Insurance Australia Ltd v Certain Underwriters at Lloyds of London [2019] the New South Wales Court of Appeal held that competing Escape and Excess Clauses would also cancel each other out on the basis that both seek to avoid primary liability in the event of double insurance – an Escape Clause seeks to avoid any liability, whilst an Excess Clause recognises only a secondary one.

The New Zealand courts, by contrast Abigail noted, have on one occasion reached the conclusion that an Escape Clause will prevail (albeit relying heavily on the insurance provisions in an underlying contract). As such, the outcome will always come down to the specific policy wording and the wider context; “there is no universal hierarchy that automatically applies.”

Rateable Proportion Clauses

The final type of other insurance clause limits an insurer’s share of the loss in proportion to the policy limit. For example:

- An insured incurred £900,000 of loss covered under two separate policies.

- Policy A with a limit of £1m, and Policy B with a limit of £2m.

- Policy A’s insurer would be liable for 1/3 of the loss (their £1m portion of the total £3m insured), which is £300,000, and Policy B’s insurer would be liable for 2/3 which is £600,000.

If Policy A contained a Rateable Proportion Clause, and Policy B was silent, Policy B’s insurer would have to pay the whole of the loss and then claim a contribution from Policy A’s insurer.

Rateable Proportion Clause v Escape / Excess Clause

Unlike Escape and Excess Clauses, Rateable Proportion Clauses acknowledge that an insurer does have a primary liability in the event of other insurance, albeit a limited one. For that reason, an Escape or Excess Clause will prevail over a Rateable Proportion Clause.

If Policy A included a Rateable Proportion Clause whilst Policy B included an Escape Clause, the effect of the Escape Clause is that there would be no double insurance and Policy A’s insurer would be liable for the loss without being entitled to claim a contribution from Policy B’s insurer.

Whilst there has been some controversy over how an Excess Clauses might compete with a Rateable Proportion Clause (Austin v Zurich [1944]), in NFU v HSBC, Gavin Kealey KC sought to clarify the position. He remarked that, as a matter of construction, an Excess Clause should prevail over a Rateable Proportion Clause because a Rateable Proportion Clause recognises that an insurer has a primary liability in the event of double insurance, whereas an Excess Clause does not.

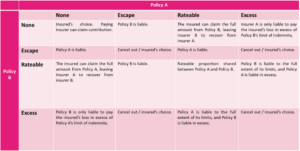

Abigail produced the table below as a starting guide for interpreting competing clauses, but was careful to note that the position will always depend on the policy wording, and the wider context.

Remaining questions

One issue that the courts are yet to address is whether, where an insured has multiple policies forming a horizontal primary layer of cover, followed by an excess layer that sits above, the entire horizontal layer must be exhausted before the excess policy responds.

The issue hasn’t arisen in caselaw to date, but Abigail remarked that it will be interesting to see how the courts approach the question when the times comes.

Key takeaways

The good news, for policyholders, is that the courts have so far refused to entertain any scenario in which an insured is left without primary cover.

That doesn’t mean, Abigail warns, that other insurance is an insurer’s problem. In circumstances where an Escape or Excess Clause prevails, an insured can be left without access to a policy that it paid a premium for, and which may well be preferable on its terms. Similarly, the disadvantage of Rateable Proportion Clauses from an insureds point of view is that the risk of insurer insolvency transfers back to the insured.

For those reasons, it is worth understanding whether there is another policy that responds to a risk and, if so, how any other insurance provisions might be interpreted.

Author

Abigail Smith, Associate

When Clauses Collide: Court of Appeal Backs MRC Over New York Arbitration

A recent Court of Appeal decision, Tyson International Company Ltd v GIC Re, India, Corporate Member Ltd [2026] EWCA Civ 40, provides valuable clarification on the approach taken by English courts when confronted with conflicting jurisdiction and arbitration provisions contained within layered reinsurance documentation.

Background:

Tyson International Company Ltd (“TICL”) is the Bermudan captive insurer for Tyson Foods, a major US‑based global food producer. In 2021, TICL arranged facultative reinsurance for its property risks with several reinsurers, including GIC Re, India, Corporate Member Ltd (“GIC”).

Two layers of facultative reinsurance were first placed on 30 June 2021 by way of a London Market Reform Contract (the “MRC”). The MRC provided for English governing law and contained a clause granting the courts of England and Wales exclusive jurisdiction over all matters relating to the reinsurance.

On 9 July 2021, this placement was supplemented by the execution of a second set of contracts in the form of the Market Uniform Reinsurance Agreement (the “Certificate”). The Certificate, instead, required disputes to be resolved by arbitration in New York under New York law. They also incorporated three amendments, the second of which stated that the MRC would “take precedence over reinsurance certificate in case of confusion” (the “Confusion Clause”).

A fire at a Tyson Foods facility in Hanceville, Alabama on 30 July 2021 gave rise to a claim under the captive policy. TICL accepted coverage and notified GIC. GIC later purported to rescind its reinsurance participation based on alleged misrepresentation relating to property valuations. TICL commenced proceedings in England relying on the jurisdiction clause in the MRC, while GIC sought to compel New York arbitration under the Certificate.

At first instance, the Commercial Court granted TICL a permanent anti‑suit injunction restraining GIC from pursuing the New York arbitration. In response, GIC appealed to the Court of Appeal.

Parties’ positions and key issues:

GIC’s principal argument was that the Confusion Clause was narrow in scope and applied only to internal drafting inconsistencies within the Certificate itself. GIC also maintained that, even if the clause applied more broadly, the English jurisdiction clause in the MRC and the New York arbitration clause in the Certificate should be read together in a manner that gave effect to both, with the English courts assuming a supervisory role over arbitration in New York.

TICL submitted that the Confusion Clause operated as a genuine hierarchy provision intended to resolve inconsistencies between the two documents. Once invoked, it required the English governing law and exclusive jurisdiction provisions in the MRC to prevail, leaving no room for the New York arbitration clause to operate.

Hence, the key issues for consideration were:

- The proper construction of the Confusion Clause; and

- Whether the English jurisdiction clause in the MRC and the New York arbitration clause in the Certificate could operate together

Analysis:

- The proper construction of the Confusion Clause:

GIC submitted that the Confusion Clause applied only where the Certificate itself contained internal inconsistencies and did not extend to conflicts between the Certificate and the MRC. The Court rejected this interpretation. It held that the natural and commercially coherent meaning of the wording was that it addressed inconsistency arising between the two documents. The MRC and Certificate were executed nine days apart and contained materially different provisions; it was, thus, far more plausible that the clause was intended to identify the document that should prevail where such differences arose.

Critically, the Court also commented that GIC’s narrow construction would be commercially unsound in rendering the clause ineffective when the most obvious form of “confusion” occurred; namely, a contradiction between the documents themselves.

- Whether the English jurisdiction clause and New York arbitration clause could operate together?

GIC argued that even if the MRC prevailed, the English jurisdiction clause could be read as supervisory or auxiliary to New York arbitration. The Court, however, rejected this in finding that the MRC conferred exclusive jurisdiction on the English courts in clear and unqualified terms, while the Certificates mandated binding arbitration in New York. To reinterpret the English clause as merely supervisory would invert the contractual hierarchy expressly agreed through the Confusion Clause and substantially distort the meaning of the exclusive jurisdiction provision.

The permanent anti‑suit injunction was, therefore, correctly granted.

Conclusion:

The decision provides clear confirmation that ordinary principles of contractual interpretation remain paramount in resolving disputes arising from inconsistent reinsurance documentation. The Court emphasised that where parties have chosen express language, particularly as to precedence, the courts will give effect to that language according to its natural and literal meaning. It is not the role of the court to retrospectively correct what may, in hindsight, be commercially disadvantageous to one party, nor to remodel the parties’ bargain by reading fundamentally inconsistent clauses together.

Authors

Michael Robin, Partner

Pawinder Manak, Trainee Solicitor