Fenchurch Law – Annual Coverage Review 2025

As the insurance market continues to navigate evolving risks, regulatory frameworks, and geopolitical developments, 2025 has delivered a series of judgments that set important precedents as well as reaffirming established coverage principles. This annual review highlights the key themes emerging from these decisions and their practical implications for those responsible for managing coverage and compliance.

The cases reported this year address critical issues such as the interpretation of policy terms, the scope of notification obligations, the application of fair presentation duties and the classification of policy terms under the Insurance Act 2015. They also explore the impact of third-party rights, insolvency considerations, and principles regarding multiple cover when ‘other insurance’ clauses are in play.

Collectively, these rulings clarify the boundaries of contractual and statutory duties, reinforce the importance of timely and accurate disclosures, and provide guidance on maintaining coverage integrity in complex scenarios.

This round-up aims to equip policyholders and brokers with a clear understanding of the legal trends shaping the insurance landscape, including salutary reminders and pitfalls to avoid.

Unless otherwise stated, the Insurance Act 2015 is referred to as the “2015 Act” and the Third Parties (Rights Against Insurers) Act 2010 as the “2010 Act”.

Insurance Act 2015

- Lonham Group Ltd v Scotbeef Ltd & DS Storage Ltd (in liquidation) (05 March 2025)

In this Judgment, the Court of Appeal issued seminal guidance on how the 2015 Act treats representations, warranties, and conditions precedent. The Court was asked to determine whether the requirements under a Duty of Assured clause were representations or conditions precedent and thus triggering different sections of the 2015 Act.

The policy contained a three‑limb “Duty of Assured Clause” requiring D&S to:

- Declare all current trading conditions at policy inception.

- Continuously trade under those conditions.

- Take all reasonable steps to ensure those conditions were incorporated into all contracts.

The Court was asked to consider whether all three limbs needed to be read collectively (i.e. they would all be classified as either representations or conditions/warranties) or separately (so that each limb was capable of a separate classification). Overturning the decision of the High Court, the Court found that limb 1 was a pre-contractual representation subject to the duty of fair presentation of the 2015 Act, but limbs 2 and 3 were warranties and conditions precedent. As such, in accordance with the 2015 Act, the Insurer had no liability after the date on which the warranty had been breached.

This classification was said to reflect the 2015 Act’s intent: representations allow for proportionate remedies if inaccurate; terms requiring future conduct held to be warranties and/or conditions, by contrast, enable insurers to reject coverage upon breach, provided the terms are clearly drafted.

This decision marked the first major Court of Appeal test of Part 3 of the 2015 Act, and confirms that Duty of Assured clauses can contain both historic representations that go to the Insured’s duty of fair presentation, and warranties as to future conduct, which can have particularly catastrophic consequences if breached. It serves as a reminder to Policyholders and Brokers to scrutinise policy terms and ensure compliance.

Read our full article here.

- Clarendon v Zurich [2025] EWHC 267 (Comm) – Commercial Court Judgment (13 February 2025)

Fenchurch Law acted for Clarendon Dental Spa LLP and Clarendon Dental Spa (Leeds) Ltd, who claimed under a Zurich property damage and business interruption policy after a major fire. Zurich sought to avoid liability, alleging breach of the duty of fair presentation under the 2015 Act for failing to disclose insolvency of related entities.

The Court examined Zurich’s proposal question, “Have you or any partners, directors or family members involved in the business… been declared bankrupt or insolvent…?,” and held that a reasonable policyholder would interpret it as referring only to current directors or partners, not former entities. Consistent with Ristorante Ltd v Zurich (2021), and applying contra proferentem, the Court confirmed that ambiguity in insurer questions is resolved in favour of the insured and that disclosure obligations are shaped by the questions asked at inception.

Overall, the Court concluded Clarendon’s answers were correct and, in any event, Zurich had waived any right to disclosure beyond the scope of its own questions.

Please see our full article here.

- Delos Shipholding v Allianz [2025] EWCA Civ 1019

The Court of Appeal upheld the earlier Commercial Court’s ruling, reinforcing policyholder rights under marine war risks insurance and clarifying the duty of fair presentation under the 2015 Act. The case concerned the bulk carrier WIN WIN, detained by Indonesian authorities for over a year after a minor anchoring infraction. Allianz denied cover, citing an exclusion for detentions under customs or quarantine regulations and alleging non-disclosure of criminal charges against a nominee director.

The Court confirmed the exclusion must be construed narrowly, only detentions genuinely akin to customs or quarantine regulations fall within its scope and the WIN WIN’s detention did not qualify. It also reaffirmed that fortuity remains where the insured’s actions were neither voluntary nor intended to cause the loss. On duty of fair presentation, the Court held the nominee director (who had no decision-making authority) was not part of “senior management” under the 2015 Act, so the Policyholder had no actual or constructive knowledge of criminal charges against him. Further, Allianz had failed to prove that the charges were material and would have induced Allianz to enter into the insurance contract.

Our article on the Court of Appeal Judgment can be found here. Our earlier article on the Judgment of first instance is also here.

- Mode Management Limited v Axa Insurance UK PLC [2025] EWHC 2025 (Comm)

Following a fire on 7 February 2018 at industrial units in Brentwood, Mode (the named insured) and its director (the property owner) sued AXA under a “Property Investor’s Protection Plan” seeking declaratory relief, specific performance (to reinstate/put them back to the pre‑loss position), and other remedies. AXA had avoided the policy ab initio in September 2018 for alleged misrepresentation/non‑disclosure (including questions over insurable interest and planning permission) and applied for summary judgment.

The Commercial Court (Lesley Anderson KC sitting as Deputy High Court Judge) granted AXA’s application. The judge held that the claims were statute‑barred under the Limitation Act 1980, and in any event had no real prospect of success, including the insured’s bid for specific performance of AXA’s alleged secondary liability to reinstate.

The director’s personal claim also failed because he was not a party insured under the policy. The Court emphasised that, on the pleaded facts and policy wording, specific performance was not an available remedy, and the case could be resolved without a trial.

The Judgment can be accessed here.

- Malhotra Leisure Ltd v Aviva [2025] EWHC

During the Covid-19 lockdown in July 2020, a cold-water storage tank burst at one of Malhotra’s hotels, causing significant damage. Aviva, the property damage and business interruption insurer, refused indemnity, alleging the escape of water was deliberately and dishonestly induced by the claimant and that there were associated breaches of the policy’s fraud condition.

The Commercial Court held that Aviva bore the burden of proving, on the balance of probabilities, that the incident was intentional. The Court found that available plumbing and expert evidence supported an accidental explanation, and Aviva’s own expert accepted the escape could have been fortuitous.

The Court also scrutinised Aviva’s allegations of dishonesty in the presentation of the claim, finding that the Fraud Condition must be interpreted in line with the common law, meaning it applies only to dishonest collateral lies that materially support the claim, consistent with The Aegeon and Versloot. Because there was no evidence of dishonesty, and the alleged inaccuracies were either immaterial or inadvertent, the fraud condition did not bite, and Malhotra Leisure was entitled to indemnity.

Please see our full article here.

In a separate costs hearing, the Commercial Court was asked to determine whether costs should be awarded on the standard or indemnity basis. The claimant’s approved costs budget was £546,730.50, but actual costs exceeded £1.2 million, making the distinction significant.

The Court noted that while there is no presumption in favour of indemnity costs where fraud allegations fail, such allegations are of the highest seriousness and, if unsuccessful, will often justify indemnity costs. The Judge found that Aviva’s allegations inflicted financial and reputational harm and were pursued to trial without settlement discussions. As a result, the Court ordered Aviva to pay the claimant’s costs on the indemnity basis, including an interim payment of £660,000, demonstrating the Court’s uncompromising approach towards unfounded fraud allegations.

Please see our full article here.

Effect of Third Parties Rights against Insurers Act 2010

- Makin v QBE [2025] EWHC 895 (KB), Archer v Riverstone [2025] EWHC 1342 (KB), and Ahmed & Ors v White & Co & Allianz [2025] EWHC 2399 (Comm)

This trio of cases highlights the strict approach taken to claims notification provisions in liability insurance policies alongside their impact under the 2010 Act and reaffirms that Claimants under the 2010 Act will have to suffer the consequences of a policyholders breach of conditions.

The Courts confirmed that third-party claimants inherit not only the insured’s rights but also its contractual obligations. Notification clauses were treated as conditions precedent, even where not expressly labelled as such, meaning a breach of these provisions entitled insurers to deny indemnity.

In Makin, Protec Security delayed notifying QBE for three years after an incident that ultimately led to catastrophic injury. The Court held that the obligation to notify arose once Protec reasonably appreciated potential liability which was well before formal proceedings. Ultimately, failure to comply barred recovery.

Similarly, in Archer, R’N’F Catering failed to notify Riverstone promptly and ignored repeated requests for information. The Court rejected arguments that the claimant’s later cooperation could cure the insured’s breach, confirming that rights lost by the insured cannot be revived under the 2010 Act.

Both judgments emphasise that the trigger for notification is not the incident itself but the point at which the insured knows a claim may arise. Excuses such as administrative errors (argument that relevant correspondence had been sent to a spam folder) or insolvency were given short shrift.

By contrast, Ahmed focused on whether notifications made by White & Co to Allianz were sufficiently clear to trigger coverage under a professional indemnity policy. Despite extensive correspondence, the Court found none of the notifications adequately identified the claims or potential liabilities intended to be covered. The judgment underscores that compliance is not just about timing but also clarity and substance, vague or incomplete notices may fail to engage the policy.

The case also illustrates how technical drafting, such as aggregation clauses and endorsements, can compound the consequences of inadequate notification, limiting recovery even where coverage might otherwise apply.

These decisions reinforce several key points for policyholders and claimants:

- Notification clauses, even if unlabelled, may operate as conditions precedent.

- Breaches by the insured cannot be remedied by third-party claimants under the 2010 Act.

- Both timing and clarity of notifications are critical; “can of worms” notifications must be explicit.

- Failure to comply can result in catastrophic loss of indemnity, regardless of claim severity.

Policyholders, with their Brokers' assistance, should adopt a proactive and precise approach to claims notification to avoid disputes and preserve coverage.

Please see our full article on Ahmed here.

The full Judgment on Ahmed is available here.

Aviation

- Russian Aircraft Lessor Policy Claims [2025] EWHC 1430 (Comm).

In a landmark Judgment handed down on 30 June 2025, the Commercial Court determined coverage disputes arising from the grounding and expropriation of hundreds of Western leased aircraft in Russia following the invasion of Ukraine and the imposition of Russian Order 311 in March 2022. The claims, brought by a consortium of lessors including AerCap, DAE, Falcon, KDAC, Merx and Genesis, were the subject of a “mega trial” and resulted in the largest ever insurance award by the UK courts of over £809 million.

The Court held that Contingent Cover responded because the aircraft were not in the lessors’ physical possession and operator policy claims remained unpaid (interpreting, “not indemnified” as “not paid”). Applying a balance of probabilities standard, permanent deprivation was deemed to occur on 10 March 2022, with Russian Order 311 identified as the proximate cause amounting to an effective governmental restraint. This amounted to governmental “restraint” or “detention,” which fell within the Government Peril exclusion under the All-Risks section. Under the Wayne Tank principle, where there are concurrent causes, one covered and one excluded, the exclusion prevails, meaning All Risks could not respond. Consequently, the claims were covered under the War Risks section.

The biggest takeaway for Policyholders from this case, is the guidance that Mr Justice Butcher adopted from the Australian case of LCA Marrickville Pty Limited v Swiss Re International SE [2022] FCAFC 17, which held that:

“The ease with which an insured may establish matters relevant to its claim for indemnity may influence questions of construction … a construction which advances the purpose of the cover is to be preferred to one that hinders it as a factor in construing the policies.”

Please see our full article here.

Building Safety Act 1972

- URS Corporation Ltd (Appellant) v BDW Trading Ltd (Respondent) [2025] UKSC 21

In summary, BDW (being the relevant developer) sued URS (being the design engineers) in negligence for repair costs from structural defects in two development schemes. The Supreme Court was asked to decide whether such voluntarily incurred cost was recoverable and whether section 135 of the Building Safety Act 2022 (“BSA”) extends limitation for such claims.

The Supreme Court unanimously found that once developer knows that defects are attributable to negligent design then remedial works – even on property no longer owned by it – are not ‘voluntary’ in the sense they fall within the ambit of the engineers’ duty. This fortifies the existing common law principles that loss incurred in reliance on professional duty is recoverable, even absent a direct proprietary interest.

The Court clarified that section 135 of the BSA merely extends time for Defective Premises Act 1972 claims and does not revive or extend limitation periods for tortious claims. Policyholders should note that professional indemnity insurers need not cover historic negligence where properly time-barred under the Limitation Act 1980, unless otherwise endorsed.

The Court also held that section 135 of the BSA does not permit developers to treat their negligent repair costs as falling within extended timeframes, preserving clear statutory boundaries between contract/statutory claims and tort claims.

Read our full article on the Supreme Court’s Judgment here.

CAR Policies

- Sky UK Limited & Mace Limited v Riverstone Managing Agency Ltd [2025] EWCA Civ 1567

Insurers sought permission to appeal the Court of Appeal’s December 2024 decision in Sky v Riverstone ([2024] EWCA Civ 1567), which confirmed that deterioration and development damage occurring after the policy period, but stemming from damage during it, was covered under the CAR policy, along with investigation costs and a single deductible per event.

On 30 April 2025, the Supreme Court refused permission to appeal, leaving the Court of Appeal’s ruling intact. This outcome reinforces that insurers cannot restrict recovery to damage physically present at the end of the policy period and affirms a practical approach to progressive damage under CAR policies.

Overall, the refusal cements the Court of Appeal’s interpretation, providing certainty for policyholders on coverage for post-expiry deterioration linked to insured-period damage.

Our article on the Court of Appeal ruling, now confirmed by the Supreme Court’s dismissal is found here.

Latent Defects

- National House Building Council v Peabody Trust [2025] EWCA Civ 932 (CA)

The Court of Appeal resolved a key limitation question over NHBC Buildmark insurance’s “Option 1 – Insolvency cover before practical completion.” Under this extension, insurance is triggered not by the contractor’s insolvency per se but when the employer (Peabody) “has to pay more” to complete the homes because of the insolvency.

The underlying development involved 175 dwellings, including 88 social housing units. The contractor became insolvent in June 2016, and Peabody arranged for completion thereafter, with practical completion in January 2021. The claim for additional completion costs was brought in July 2023. NHBC contended that the cause of action accrued in 2016, when the contractor became insolvent, and was now statute-barred; Peabody argued instead that it accrued when costs were actually incurred.

The Court unanimously agreed with Peabody, affirming the Technology & Construction Court’s view that the policy insured against additional payment triggered by insolvency, so the cause of action only accrued when extra costs became payable. The NHBC appeal was dismissed.

This decision emphasises the importance of carefully identifying the insured event as defined in policy terms and confirms that policies with “pay-when-loss-incurred” triggers should be interpreted on their true wording rather than conventional accrual rules.

The Judgment can be found here.

Other Insurance

- Watford Community Housing Trust v Arthur J Gallagher Insurance Brokers Ltd

This Judgment was a significant ruling clarifying principles concerning multiple cover and a policyholder’s rights following a cyber-related loss. It was a resounding win for policyholders: securing sequential access to multiple policies.

The Court held that Watford had the right to choose which policies to invoke, having the benefit of PI, Cyber and Combined policies, attracting limits of £5 million, £1 million, and £5 million, respectively. Timely notification was made under the Cyber policy, but late notification was successfully raised by the PI insurer to decline indemnity. The Combined insurer confirmed cover despite late notification.

The Court held that the “other insurance” clauses (limiting cover where overlapping insurance exists) effectively neutralised each other, allowing sequential claims rather than enforcing contribution across overlapping policies. This ruling supports the principle that a policyholder can access each policy in turn until the total loss is covered. Having recovered £6 million, Watford also sought recovery of the additional £5 million under the PI policy had timely notification been made. Consequently, Watford was entitled to a total of £11 million.

As to broker liability, the Court found that, but for the broker’s negligence, the PI policy would have been exhausted. Since it was not, the broker was held liable for the £5 million shortfall. The Judgment is a stark reminder that notification conditions should be identified and complied with. It also emphasises a broker’s duty to accurately advise on policy layers and limitations to ensure the policyholder is clearly instructed and that the advice given is documented.

Our full article can be found here.

Authors

Dan Robin, Managing Partner

Catrin Wyn Williams, Associate

Pawinder Manak, Trainee Solicitor

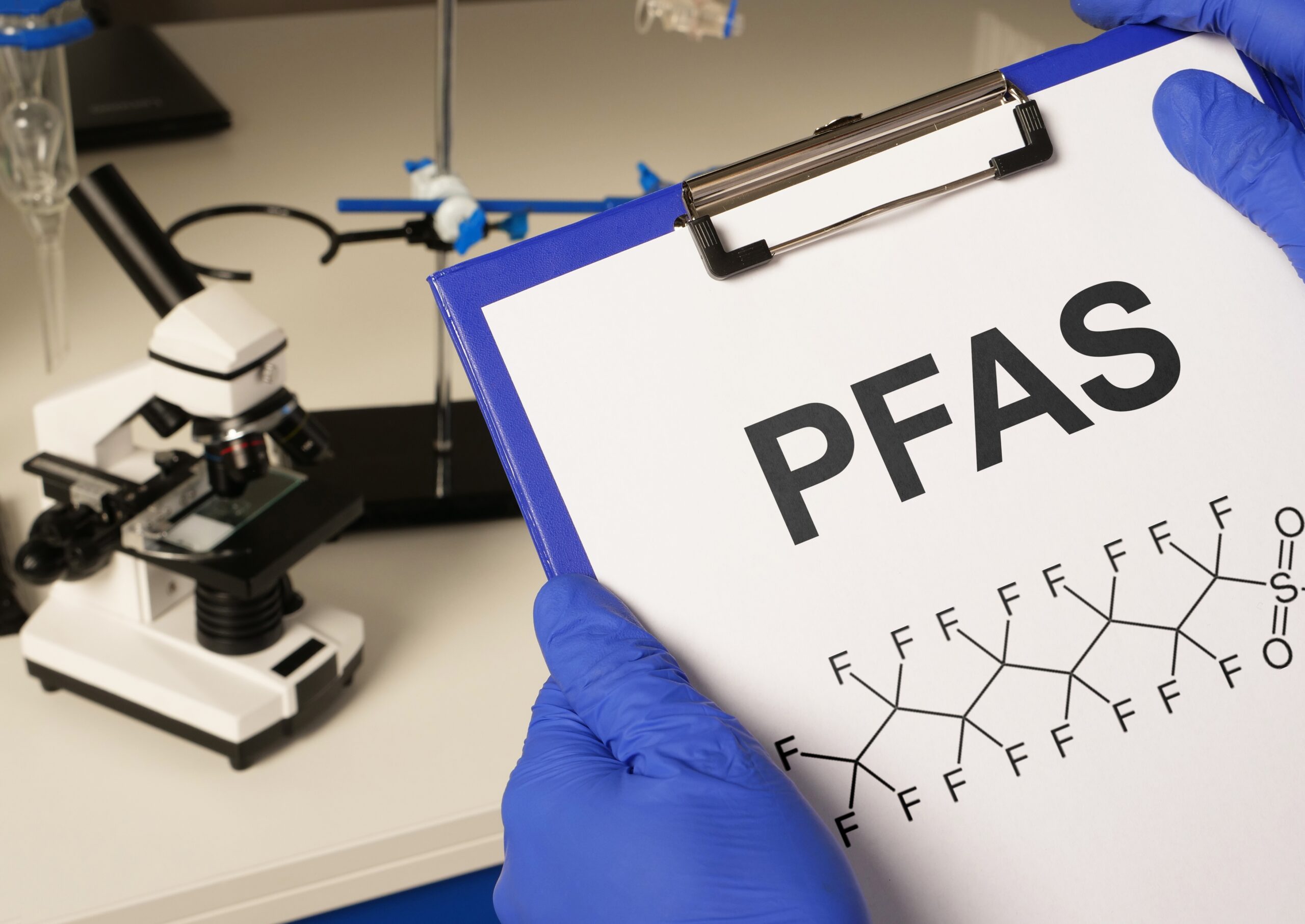

PFAS – Out of the Frying Pan into the Court Room?

Fenchurch Law considers the impact of PFAS on the UK insurance sector, following the rise of litigation progressing through the US courts.

What Are PFAs?

PFAS, or Polyfluoroalkyl Substances, also known as Forever Chemicals, are a group of over 10,000 chemicals that do not readily degrade.

These synthetic chemicals have been utilised in products such as non-stick cookware, waterproof clothing and cosmetics since the 1950s for their non-stick, water- and heat-resistant properties. A concerning aspect of PFAS is that they can accumulate indefinitely in the environment and in living organisms. Their highly durable nature has led scientists to investigate the long-term effects of these chemicals on the body and the environment, with alarming results.

Currently, PFAS are linked to several health issues, including immunosuppression and certain types of cancer. Consequently, and unsurprisingly, regulators are now aiming to tighten the regulation of PFAS chemicals to limit ongoing risks.

Regulatory Landscape in the UK

PFAS are currently regulated under the UK REACH regime (Registration, Evaluation, Authorisation, and Restriction of Chemicals). However, only a limited number of specific PFAS are restricted for use in the UK. For example, PFOA (Perfluorooctanoic acid) and PFOS (perfluorooctane sulfonate) are types of chemicals within the PFAS category and have been listed as Persistent Organic Pollutants (POPs), making it illegal (with limited exceptions) to manufacture or use them in the UK and requiring their removal from products and waste streams.

The emerging risks associated with PFAS use are being closely monitored, with the HSE initiating a six-month consultation earlier this year on the use of PFAS in firefighting foam. UK regulation lags behind other countries; for example, the US has already declared PFAS a critical contamination crisis.

Although the UK regulatory framework for PFAS is still in its early stages, the Environmental Agency has begun assessing the risks. It has identified over 10,000 “high risk” sites believed to contain elevated PFAS levels. Some of the highest-risk sites include firefighting foam manufacturing plants, RAF bases, and airports.

Emerging Risks for the Insurance Sector

PFAS present a complex challenge for insurers. They pose potential long-tail liabilities, similar to claims arising from asbestos or environmental pollution, arising from historic use. Moreover, the increased focus of regulators and claimants on PFAS means insurers must navigate a rapidly changing risk that spans numerous lines of insurance – including general liability, product liability, environmental impairment, directors & officers, as well as property and speciality lines.

Insurers' response to this uncertain risk exposure has been to introduce specific exclusions, often based on existing pollution exclusion clauses. For instance, insurers may add a clause excluding any claims “arising out of, resulting from or relating to PFAS of any kind”. Of course, such exclusions will not be relevant to the extent cover attaches to expired policies.

Lloyd’s has also issued standard PFAS exclusion wordings, LMA5595A and LMA5596A[1].

Types of Claims

- Nuisance Claims: arising from contamination of public drinking water and environmental cleanup.

- Personal injury Claims: resulting from exposure to PFAS in everyday products.

- Property Damage/Diminution of Value Claims: caused by PFAS seeping into the ground from industrial manufacturers.

- False Advertising & Product Labelling: Due to products failing to identify the dangers of PFAS.

The New Asbestos?

The insurance market has been questioning whether PFAS will become the “next asbestos”, as both are similar in that they were once widespread, marketed as safe, and only later revealed to be potentially dangerous.

However, a key difference between PFAS and asbestos is that exposure to many different types of PFAS is unavoidable in the modern world, whereas asbestos exposure can usually be traced back to a specific place and time to establish a cause. This causal link is likely to be far more difficult to establish in the context of PFAS exposure.

Currently, unlike in asbestos claims, no disease has been solely linked to PFAS exposure. This complicates the process of directly attributing the development of diseases such as cancer to PFAS, requiring substantial expert evidence to support the claim that the claimant would not have developed the disease without specific PFAS exposure.

UK PFAS Litigation

Although PFAS litigation is advancing through US courts with multimillion-dollar settlements already reached, UK litigation remains in the early stages. So far, there have been no PFAS cases litigated in UK courts, but two British law firms have announced investigations into PFAS contamination cases. While formal proceedings may take time, we might soon see the first UK group action application for PFAS.

Similarly, to date, there have been no regulatory actions; however, the UK Environment Agency or local authorities could designate contaminated sites for remediation in the future. Companies might then face clean-up costs and seek insurance coverage for those expenses.

Furthermore, the lack of UK personal injury claims may stem from the difficulty in proving a causal link between exposure and injury. While legal systems in countries like the US are more claimant-friendly in this regard, the UK requires evidence that a defendant’s actions caused the harm. The widespread presence of PFAS compounds further complicates this issue. There is no precedent in the UK for relaxing causation standards for PFAS, unlike asbestos, where English law permits more lenient rules for mesothelioma causation.

If and when PFAS claims arise, several key coverage questions will need to be answered, including whether PFAS claims constitute “pollution” and whether the contamination was sudden or gradual. When did an “occurrence” of contamination or injury happen (continuous trigger or not)? Can a claimant’s blood PFAS levels amount to an “injury” within the policy period?

Conclusion

PFAS present an increasing challenge across various sectors due to their persistence, health hazards, and complex liability concerns. Their extensive use, environmental durability, and potential health effects have led to heightened scrutiny and regulatory measures. However, the UK’s response via regulators and the Courts is still in its early phases compared to other jurisdictions.

As UK regulation and litigation evolve, proactive risk management and continuous vigilance will be essential to navigate the uncertainties associated with these “forever chemicals.”

[1] https://lmalloyds.imiscloud.com/LMA_Bulletins/LMA23-035-TC.aspx

Chloe Franklin is an Assoicate at Fenchurch Law

New Zealand’s Contracts of Insurance Act 2024 – What to Expect for Policyholders

The Contracts of Insurance Act (the “Act”), which received royal assent in 2024 and will come into force at the latest by November 2027, will overhaul and rationalise insurance law in New Zealand while harmonising it with existing law in other common law jurisdictions. In some respects, the Act should be celebrated as a win for policyholders, as it adopts some of the policyholder-friendly approaches taken in the UK Insurance Act 2015 (the “UK Act”).

The Act is intended to provide greater clarity for both consumers and commercial parties, replacing the previously fragmented law that was contained in multiple statutes and common law principles.

Key Provisions

The Act distinguishes between consumer and non-consumer (ie, commercial) policies. This article focuses only on the latter.

- Disclosure Duties

Previously, an insured’s duty of disclosure was based on the principle of utmost good faith. Under the Bill, this is amended to a duty of fair presentation of the risk, mirroring the UK Act. This requires that a policyholder:- Discloses every “material circumstance” that the policyholder knew or ought to have known, or provides sufficient information to put a prudent insurer on notice to make further inquiries;

- Gives disclosure in a reasonably clear and accessible manner; and

- Makes every “material representation” of fact substantially correct.

Here, “material” means anything that would influence the judgment of a prudent insurer.

For our thoughts on how the English courts have applied the principle of fair presentation, please see A “WIN WIN” for Policyholders - Fenchurch Law APAC.

- Proportionate Remedies

The Act also introduces proportionate remedies where the duty of fair presentation is breached, again mirroring the UK Act,. This is a departure from the previous “all or nothing” position, which meant the insurer could avoid the policy for breach of duty. The Bill now provides that the insurer can either:- Avoid the policy but return the premium (where the breach is not deliberate or reckless);

- Amend the policy terms where the insurer would still have underwritten the policy but on different terms; or

- Where the insurer would have charged a higher premium, it can either raise the premium for the term of the policy or proportionately reduce the indemnity.

- Damages for Late Payment of Claims

Another import from the UK Act, the Act establishes a new cause of action for damages where insurers fail to process claims within a “reasonable time”.- Whether the insurer has reasonable grounds for disputing the claim is a relevant factor in determining whether the obligation has been breached, as is the case under the UK Act.

- An insured will only be entitled to damages if it can establish that the insurer’s breach caused a loss, and those losses will be subject to the usual principle that they must not be too remote.

Aims

The above changes should allow policyholders to understand their obligations, and those of insurers more clearly and allow more efficient resolution of claims disputes.

The Act is designed to provide clarity and address historical imbalances between policyholders and insurers, and levels the playing field for policyholders by making their obligations and rights of recourse easier to understand.

What can be learnt from the UK market?

The coming into force of the UK Act has resulted in relatively few reported cases, making it more challenging to predict how New Zealand courts will interpret the provisions of the Act.

However, market feedback to the UK Act has shown that it has had a positive influence, fostering better communication before a policy is taken out, and fairer treatment of policyholders during the claims process.

Qualitative research suggests that Risk Managers have changed how they approach disclosure following the UK Act, with survey respondents reporting greater engagement with insurers.

While the introduction of damages for late payment has not so far resulted in any successful claims in the UK, the mere presence of the rule may be a motivator for insurers to handle claims diligently.

Most importantly, surveyed risk managers reported that the impact of the 2015 Act has overall been positive. Further, the data shows that, contrary to some initial fears, the introduction of the UK Act did not lead to a spike in disputes. The same result should be hoped for, and expected, in New Zealand.

Matthew King is an Associate at Fenchurch Law.

The Good, the Bad & the Ugly: #26 The Good: The Seashell of Lisson Grove Ltd v Aviva

Welcome to the latest in the series of blogs from Fenchurch Law: 100 cases every policyholder needs to know. An opinionated and practical guide to the most important insurance decisions relating to the London / English insurance markets, all looked at from a pro-policyholder perspective.

Some cases are correctly decided and positive for policyholders. We celebrate those cases as The Good.

In our view, some cases are bad for policyholders, wrongly decided and in need of being overturned. We highlight those decisions as The Bad.

Other cases are bad for policyholders but seem (even to our policyholder-tinted eyes) to be correctly decided. Those cases can trip up even the most honest policyholder with the most genuine claim. We put the hazard lights on those cases as The Ugly.

#26 The Good: The Seashell of Lisson Grove Ltd & Ors v Aviva Insurance Ltd & Ors [2011] EWHC 1761

Introduction

In the Good, the Bad and the Ugly series, we look at recently decided cases but occasionally – as in this piece – we like to revisit an older decision which frequently crops up in negotiations with insurers.

This High Court judgment from 2009 relates to a Non-Invalidation Clauses (NIC), which are important clauses routinely found in property and construction policies.

Insurers often allege that a policyholder is in breach of a policy term or obligation and that provides them with an entitlement to decline a claim.

In responding, the policyholder and its lawyers will consider all of the usual points: Is the policyholder in fact in breach, what is the status of the term, what are the consequences of breach and the extent to which it may be possible to argue that any breach did not increase the risk of loss which occurred (so that the policyholder is saved by s.11 Insurance Act 2015).

However, even if the prospects are looking gloomy in relation to all of those points, the policyholder’s claim may nevertheless be saved by an NIC.

For these reasons, The Seashell is a very Good case from the policyholder perspective.

The claim arose from a fire at The Seashell Restaurant in Marylebone, London, in 2009. The restaurant operator and trustees of a pension scheme, who held the building's freehold, claimed against their insurers, Aviva, under two policies. In this article, we consider only the insureds’ claim under the Restaurant Policy, where Aviva denied liability, citing breaches of a Frying Range Warranty.

The Restaurant Policy

The Restaurant Policy contained the NIC below, which is a fairly typical NIC, as well as other relevant clauses as follows:

NIC

“The Insurance by Section A [Buildings] and B1 [Contents] will not be invalidated by any:

1) act; or

2) omission; or

3) alteration

either unknown to You or beyond Your control which increases the risk of Damage.

However, You must:

- a) notify Us immediately You become aware of any such act, omission or alteration; and

- b) pay any additional premium required".

Clause 5(c)

"5. Rights and Responsibilities"

(c) Any Section of this Policy will cease to be in force if after the commencement of this insurance there is any alteration in respect of such Section which results in

(i) the risk of loss damage or injury or disease being increased”

A preliminary issue was whether the NIC protected the insureds in the event they were found to have acted in breach of warranty.

The insureds argued that the “act, omission or alteration” referred to in the NIC could include a breach of warranty, and that “The Insurance” meant the insurance cover in respect of the claim, and not the entire insurance policy. In this regard, the insureds relied on the decision in Kumar v AGF [1999] where, in a different context, a bar on repudiation of “this insurance” was held to apply not only to repudiation of the policy, but also to being discharged from liability for reason of a breach of warranty.

In short, the insureds argued that, if there was a breach of warranty, they would be protected by the NIC.

The insurer argued that the NIC did not ameliorate the effect of a breach of warranty; it was instead only to ameliorate the effect of clause 5(c), such that an alteration which increased the risk of damage – which was unknown to or beyond the insured’s control – would not give the insurer any remedy under clause 5(c).

Findings

The Court agreed with the insureds and found that:

1. Clause 5(c) was triggered in the event there was an "alteration" which increased the risk of damage, whereas the NIC applied where there was "any act, omission or alteration" which increase the risk of damage. The inclusion of the words "act [or] omission", in addition to “alteration”, indicated that the NIC's application was not limited to ameliorating the effect of clause 5(c);

2. The words "act or omission" were capable of applying to a misrepresentation, non-disclosure or breach of warranty. Thus, if the insured was inadvertently in breach of any of these different types of obligation, the NIC might alleviate the consequences of breach. Interestingly, the decision did not mention whether the words “act or omission” were capable of applying to a condition precedent although, in another case with an identically worded NIC where an insured has breached a condition precedent, there is no reason to consider that the NIC may not come to the policyholder’s rescue for the same reasons discussed in The Seashell.

3. The insureds could still rely on the NIC notwithstanding damage had already occurred, provided it notified the insurer immediately on becoming aware of the breach and paid any additional premium required. Whilst not part of the decision in The Seashell, in other cases any discretion that an insurer has to charge additional premium must be exercised in good faith (subject to the wording of the policy), meaning an insurer is unlikely to be entitled to arbitrarily charge exorbitant premium post-damage where an insured seeks the protection under an NIC; any premium charged should bear some correlation to the increase in the risk of damage caused by the act/omission/alteration.

Conclusion

The precise effect of an NIC will, of course, always turn on its interpretation and that of the wider policy. The judgment in The Seashell is a useful decision in showing how the Court interpreted the NIC in that case.

As we say, the wording of the NIC was not untypical of the wordings which we see in many other policies so the decision may assist policyholders in arguing that they are relieved from the consequences of a breach of obligation; potentially any obligation.

In each case, the policyholder will also need to satisfy the constituent factual elements of the NIC in question, e.g. that the policyholder was unaware of the breach or that it was beyond their control, that they provided immediate notification and have paid additional premium.

All of these elements can present difficult challenges to policyholders in their own right.

For example, in relation to the requirement to provide notice on becoming aware of the increased risk, whose knowledge is relevant in the case of a corporate policyholder? If “head office” have no actual or constructive knowledge of an increase in risk, will this trigger an obligation to notify or might it be possible for a policyholder to argue that it is only the knowledge of “senior management” that counts for the purposes of the NIC (relying on what s.4 of the Insurance Act 2015 says about the knowledge of a corporate insured in the different context of the duty of fair presentation).

Further, an obligation to provide “immediate” notice is clearly more onerous than one required “as soon as reasonably practicable” or similar so brokers with the gift of amending policy wordings will want to consider points like this so as to put their policyholder clients in the strongest position when claims arise.

Finally, co-insured lenders to real estate and construction projects will also want to ensure policies include a suitably drafted NIC, which may be the difference between a claim being paid or not, given such parties often have no knowledge or control over increases in risk.

Chris Ives is a Partner at Fenchurch Law

Timing is everything Part II – Archer v Riverstone and (a reminder of) the cost of not complying with a condition precedent

In our article on Makin v QBE last month, we highlighted the importance of complying with conditions precedent, and noted that claimants pursuing claims under the Third Parties (Rights Against Insurers) Act 2010 (“the 2010 Act”) inherit both the rights and obligations of the insured. This case serves as yet another clear reminder of that principle, underlining the risks claimants face when policy conditions are not strictly observed.

Background

The Claimant, Hannah Archer, issued proceedings against R’N’F Catering Limited (“R’N’F”) on 5 July 2022, seeking damages for personal injury following a meal at R’N’F’s restaurant (“the Proceedings”).

R’N’F filed a defence in December 2020 and then entered into a members’ voluntary liquidation in February 2023 (“the Insolvency”). It played no active role in the Proceedings thereafter.

By a consent order dated 9 July 2024, Riverstone Insurance (Malta) SE (“Riverstone”), the successor to ArgoGlobal SE, which insured R’N’F under a restaurant insurance policy from 18/09/18 – 17/09/19 (“the Policy”), was added to the Proceedings.

The Proceedings

Miss Archer claimed that she was entitled an indemnity from Riverstone by virtue of the 2010 Act. Specifically, she said that:

- The Insolvency meant that R’N’F’s rights under the Policy had automatically transferred to her; and

- By reason of s.9(2) of the 2010 Act – which stated that anything done by a third party which, if done by the insured, would amount to fulfilment of the condition as if done by the insured – she complied with the Policy.

The question of Riverstone’s liability to Miss Archer was disposed of at a preliminary issues trial. There were two issues to be determined:

- Could Riverstone prove that R’N’F was not entitled to an indemnity under the Policy (“Issue 1”)?

- Could s.9(2) of the 2010 Act assist Miss Archer to render Riverstone liable on proof of R’N’Fs liability (“Issue 2”)?

Issue 1

The breaches of condition precedent

Riverstone asserted the following breaches of condition precedent by R’N’F:

- A failure to “On the happening of any event which could give rise to a claim … as soon as reasonably possible give notice to the insurer” (“the First Breach”)

- A failure to “supply full details of the claim in writing together with any evidence and information that may be reasonably required by the Insurer for the purpose of investigating or verifying the claim … within … 30 days of the event or circumstances …” (“the Second Breach”).

- A failure to “take all reasonable precautions to prevent or diminish loss destruction damage or injury” (“the Third Breach”).

- A failure to “provide all help and assistance and cooperation required by the Insurer in connection with any claim” (“the Fourth Breach”).

(Collectively, “the Breaches”).

The Breaches were all largely based on the same facts.

In a nutshell, Miss Archer first contacted R’N’F on 29 November 2019 to advise that she had become seriously unwell following a meal at its restaurant. Her solicitors then wrote to R’N’F on a several occasions, which included their sending a Claim Notification Form (“CNF”) and a letter on 10 January 2020 which requested R’N’F’s insurance details. R’N’F did not respond.

Miss Archer’s solicitors then sent a letter of claim to R’N’F on 30 October 2020. That prompted R’N’F belatedly to notify Riverstone on 17 November 2020.

Sedgwick, Riverstone’s claims handlers, thereafter emailed R’N’F asking for information about the claim. That included, notably, a chaser email on 20 July 2021 which stated: “failure to assist us with this matter is a breach of policy terms so if we fail to receive your response your insurer may take the decision to decline indemnity”. Indeed, it was not until October 2022 that R’N’F’s Director, Mr Ali, engaged with Sedgwick, at which point he blamed the delay on the fact that emails had gone into a spam folder.

The parties’ positions

Riverstone said there was no case for R’N’F to answer in respect of the Breaches. It described R’N’F as “burying its head in the sand for months and indeed years, before coming up with a ‘dog ate my homework’ series of excuses’.

Miss Archer, perhaps unsurprisingly, did not advance a positive case as to R’N’F’s actions. She simply said that Sedgwick took only limited steps to contact R’N’F for information, and that “alarm bells should have rung” when R’N’F did not respond.

The decision

The court had no difficulty in finding that Riverstone was right.

As to the First Breach, it said that any and all of the initial communications from Miss Archer and/or her solicitors to R’N’F were “circumstances” which should have prompted R’N’F to notify Riverstone, and that R’N’F was “thoroughly disengaged with the threatened claim, maybe hoping that by ignoring it, it will go away”. So, because R’N’F did not notify Riverstone of the “circumstance” until 17 November 2020, the First Breach was made out.

As to the Second Breach, the court agreed with Riverstone that R’N’F repeatedly ignored Sedgwick, and had no good reason for doing so. Further, the timing of its belated engagement was redolent of a policyholder that “panicked that its prior tactic of ignoring the threatened claim had failed”. The court also rejected Mr Ali’s “spam folder” explanation; that lacked any sort of cogency, and even if it did, the court found that R’N’F ought to have had proper procedures in place for checking important emails.

Based on the same factual matrix, the court found that the Third and Fourth Breaches were also made out.

As R’N’F was in breach of conditions precedent to liability, Riverstone was entitled to refuse to indemnify it.

Issue 2

Miss Archer asserted that even if R’N’F was in breach of condition precedent, she was nonetheless entitled to an indemnity. The gist of her argument was that R’N’F only became a ‘relevant person’ within the meaning of the 2010 Act at the point of the Insolvency. Thereafter, she “stood ready” to comply with the Policy, as shown by the fact that notifying and corresponding with Sedgwick and Riverstone’s solicitors. So, her position was that anything done by her was to be treated as done by R’N’F, thus entitling her to an indemnity.

She also argued that it was impossible for her to comply with the conditions precedent in the Policy before the Insolvency, as her rights only arose at that stage. That was also consistent, she said, with the 2010 Act’s policy of protecting third parties in circumstances where an insured becomes insolvent.

Riverstone disagreed. It said that any actions taken by her after the Insolvency, however reasonable, were too late, and were incapable of leading to a conclusion that she complied with the Policy.

Although the court had considerable sympathy with Miss Archer, it found that she was nevertheless wrong. In short, it was not possible to “resurrect” her right to an indemnity in circumstances where that same right had already been invalidated by R’N’F. If it was, that would effectively mean that the conditions precedent to which was subjected were entirely different from those to which R’N’F were subjected. The court found no authority for such a proposition.

The court was also unpersuaded by Miss Archer’s impossibility argument. It noted that over three years passed between the first circumstance in November 2019 and the Insolvency, and no impossibility prevented R’N’F complying with its obligations in that time. So, as R’N’F had already lost its rights under the Policy when it was not faced with an impossibility, Miss Archer could not take the benefit of them now.

Summary

The decision in Archer is another important illustration that where an insured has already lost its rights under a policy, a claimant pursuing a 2010 Act claim stands in no better a position. Even if the failure was not of the claimant’s making, that is of no consequence – the claimant does not get a second chance.

Finally, although the judgment does not explore the point in detail, it reinforces the principle that conditions precedent, and particularly notification requirements, must be complied with strictly.

The full judgment can be found here:

https://www.bailii.org/ew/cases/EWHC/KB/2025/1342.html

Author:

Timing is everything – Makin v QBE and the cost of not complying with a condition precedent

This recent decision from the High Court provides a powerful reminder of the consequences of not complying with a condition precedent to liability, and that a claimant pursuing a claim under the Third Parties (Rights Against Insurers) Act 2010 inherits both the rights – and the pitfalls – of the insured’s policy.

Background

The Claimant, Daniel Makin, attended a Bar and Restaurant on 6 August 2017. At around 08:30pm he threw a glass on the floor while apparently in “high spirits”, and was then forcibly ejected by two door supervisors (“the Incident”).

Although Mr Makin was seemingly unaffected by the Incident (he walked away and took a taxi home), he later suffered a stroke rendering him unable to work and requiring long-term care.

The Proceedings

Acting by his mother and litigation friend, Mr Makin issued proceedings against (1) the Restaurant Muse Limited (“the Restaurant”); (2) Protec Security Group Limited (“Protec”), the employer of the two doormen; and (3) QBE Insurance (Europe) Limited (“QBE”), who insured Protec under a “Security and Fire Protection” insurance policy (“the Policy”). QBE was joined to the proceedings under the Third Parties (Rights Against Insurers) Act 2010 (“the 2010 Act”).

At a preliminary issues hearing (which Protec did not attend, having entered into administration on the preceding day), the Judge, HHJ Sephton KC, gave judgment that Protec were liable to Mr Makin for assault and his consequent injury (“the Judgment”).

At trial, the parties agreed that pursuant to the 2010 Act: (1) Mr Makin was entitled to claim against QBE directly; and (2) Mr Makin’s rights were no better than those of Protec ie., if QBE had a good defence to a claim for indemnity by Protec, it would also have a good defence to Mr Makin’s claim.

QBE asserted that it had no liability to Mr Makin because Protec breached the claims condition in the Policy – a condition precedent – which required it to notify, “… as soon as practical but in any event within thirty (30) days in the case of other damage, bodily injury, incident accident or occurrence, that may give rise to a claim under your policy …” (“the Condition”).

Mr Makin disagreed. He contended that even if there was a breach of the Condition, it was not a condition precedent which entitled QBE to automatically refuse cover. Rather, it only gave QBE only the discretion to decline the claim, which it could not exercise “arbitrarily, irrationally or capriciously”.

Finally, an issue arose as to whether the Judgment was binding in these proceedings.

The issues to be decided, therefore, were:

- Did Protec breach the Condition? (“Issue 1”)

- If so, was QBE entitled to refuse cover for a breach of a condition precedent, or did it merely have a discretion to decline the claim? (“Issue 2”)

- If QBE was not automatically entitled to refuse cover, was it nevertheless entitled to do so on the facts? (“Issue 3”)

- Was the Judgment binding on QBE? (“Issue 4”).

Issue 1

Following the incident in 2017, neither the correspondence passing between the Restaurant and Protec, the Police’s investigations, nor the Letter of Claim sent in 2020 were disclosed to QBE contemporaneously. In fact, there was no suggestion that QBE were aware of the Incident at all before July 2020. Against that background, QBE said that Protec breached the Condition.

Mr Makin argued that a reasonable person would not have thought that the Incident, on its own, might give rise to a claim. He also argued that any suggestion that Protec may have come under an obligation at a later point to notify the Incident was contrary to the proper meaning and effect of the Condition. He relied in that regard on Zurich v Maccaferri [2016], in which the Court held that the likelihood of a claim eventuating is assessed at the time the event occurs.

QBE, by contrast, held that it would have been apparent to a reasonable person in Mr Lucas’ position that a claim might be made against Protec arising out of the Incident. It also distinguished the present case from Zurich v Maccaferri, because the requirement in that case was to notify a circumstance that was “likely” to give rise to a claim, whereas the Condition required Protec to notify a circumstance “might” give rise to a claim, which was a much lower threshold.

Although the Court accepted that the Incident, in isolation, would not have led a reasonable insured to form the view that there might be claim, there was nevertheless “a clear point in time” when the matters known to Mr Lucas, which included the police investigation, and that Protec were potentially open to criticism for injuring a customer, gave rise to an obligation to notify. Having not done so, Protec was in breach of the Condition.

Issue 2

On Mr Makin’s case, the Condition was not a condition precedent. That is because, he said, it was not expressed in that way (by contrast, there were other terms in the Policy that were so expressed), and if there was any doubt as to the correct interpretation, the Condition should be construed contra proferentem in his favour.

QBE disagreed. It said the Condition did not need to be labelled as a condition precedent in order to have that effect. It also referred to the introductory section of the Condition, which stated: “The following conditions 1-10 must be complied with after an incident that may give rise to a claim under your policy. Breach of these conditions will entitle us to refuse to deal with the relevant claim”. So, QBE said, the Condition made clear at the outset that its obligation to meet a claim was conditional upon Protec’s compliance. Further, and importantly, QBE contended that the use of the word “will” was consistent with an absolute right, not a contractual discretion.

As with Issue 1, the Court agreed with QBE. The true meaning of the Condition was clear, even without the label of “condition precedent”. The Court also agreed with QBE’s analysis that the word “will”, in the introductory section of the Condition, did not merely import a discretion to decline indemnity. To hold otherwise, in the Court’s view, would do an injustice to the language used. There was also good commercial sense in that conclusion: an early notification enables an insurer to investigate claims at a time when witnesses will be easier to contact and memories are likely to be better, as well as to consider the early settlement of the claim, minimising any delays.

So, on the basis that the Condition was indeed a condition precedent to QBE’s liability, and in circumstances where that condition was breached, QBE was entitled to refuse indemnity under the Policy.

Issue 3

Given the Court’s earlier findings, this point was academic: QBE had already prevailed in light of the Protec’s breach of a condition precedent to liability. However, had the Court found that the Condition did not have that status, then, applying the well-established Braganza principles – namely, that a decision must be lawful, rational and made in good faith – it would have found that QBE was not entitled to refuse cover. The breaches in this case were trivial and of no meaningful consequence for QBE’s ability to deal with the claim.

Issue 4

The final issue was whether the Judgment establishing Protec’s liability was binding on QBE in circumstances where it was given (a) at a hearing which Protec did not attend; and (b) before QBE were a party to the proceedings.

Mr Makin contended that the Judgment was binding on QBE as establishing Protec’s liability. He relied in particular on Scotland Gas Networks plc v QBE UK Ltd, in which the Court of Session held that where a policyholder’s liability was established by way of a judgment of the court in previous proceedings, “it is not open to the [insurer] to require either the existence or the amount of that liability to be proved in the present action”.

QBE argued the contrary. It referred to AstraZeneca Insurance Co Ltd v XL Insurance (Bermuda) Ltd and Omega Proteins Ltd v Aspen Insurance UK Ltd, both of which established that neither a judgment nor an agreement are determinative of whether a loss is covered by a policy – it is open to an insurer to dispute that the insured was in fact liable.

The Court agreed with Mr Makin. The present case was distinct from Omega Proteins and AstraZeneca v XL Insurance, because those cases did not involve the 2010 Act, which was focussed on placing a claimant in the same position as the insolvent insured. It would therefore be incongruous with that objective if an insured’s liability could be determined definitively, only for the insurer to later challenge it.

Summary

There are a number of salutary lessons from Makin:

Firstly, the decision provides a convenient reminder of the distinction between “likely to” and “may / might” wordings in the context of notification conditions. Whereas the former requires an insured to notify circumstances which are at least 50% likely to lead to a claim, the latter requires only a real, as opposed to fanciful, risk of a claim eventuating. Policyholders would be well advised to check which wording appears in their policies, and to ensure that the requirements are met.

Secondly, the decision reinforces that a condition precedent need not be labelled as such in order to have that effect. Where the consequences of breaching a condition are clearly spelt out, namely, that an insurer will not be liable for a claim, the courts will likely treat the condition as a condition precedent to liability. It should never be assumed, therefore, that a condition precedent does not have that status simply because the words “condition precedent” are not included.

Thirdly, and finally, although the Court’s application of the 2010 Act did not assist Mr Makin on the facts, it is likely to be helpful for policyholders generally: where an insured’s lability is definitively determined in earlier proceedings, then, applying Makin, it will not be open to an Insurer to unravel that Judgment later down the line.

Author:

Court pours cold water on insurer’s fraud claims: Malhotra Leisure Ltd v Aviva

Court pours cold water on insurer’s fraud claims: Malhotra Leisure Ltd v Aviva

During the Covid-19 lockdown in July 2020, water escaped from a cold-water storage tank at one of the Claimant’s hotels causing significant damage.

Aviva, the Claimant’s insurer under a property damage and business interruption policy, refused to indemnify the Claimant on the basis that:

1. the escape of water was deliberately and dishonestly induced by the Claimant; and

2. there were associated breaches by the Claimant of a fraud condition in the policy.

The Commercial Court dealt with each of the issues as follows.

Was the escape of water accidental or deliberate?

Aviva bore the burden of proof and had to show that, on a balance of probabilities, the escape of water was the result of an intentional act carried out either by, or at the direction of, the Claimant or its agents.

In considering whether the escape of water was accidental or deliberate, the Deputy Judge, Nigel Cooper KC, held that there was a distinction to be drawn between whether the Claimant’s witnesses were credible, and the question of whether they were sufficiently dishonest that they were prepared to deliberately cause the incident and thereafter lie about their involvement both during the investigation and then throughout the litigation. In reaching that view, he considered the following established principles:

a) if fraud is to be made out, the evidence must exclude any substantial plausible explanation for how the escape of water may have occurred accidentally; and

b) when assessing the evidence, the Court should take into account as probative tools the following factors:

i) whether there is evidence of a plausible financial motive for the Claimant to damage its own property;

ii) the fact that owners of property do not generally destroy their own property and an allegation that they have done so is a serious charge to make;

iii) instances of lesser wrong-doing may not be probative of an allegation that an insured has deliberately destroyed property to defraud insurers; and

iv) in considering where the balance of probabilities lies, it is important to consider the evidence as a whole, putting the available evidence as to the physical cause of the escape of water into the context of the surrounding circumstances and commercial background.

In considering (a) the Judge was satisfied that it was possible, based on the plumbing evidence and the fact that Aviva’s own expert accepted that the escape of water could have been accidental, that the incident was fortuitous.

Evidence of a plausible financial motive

In circumstances where there was no direct evidence as to how the escape of water was caused, the question as to whether there was a financial motive became correspondingly more significant. Aviva submitted that there was a “preponderance of evidence” that the Claimant was struggling financially in the lead up to the incident, and that from March 2020 onwards the Claimant and its wider group had been placed under significant financial pressure as a result of the pandemic. To the contrary, the evidence showed that the Claimant’s group had extensive cash reserves (£7.5 million in cash and £150 million in tangible assets at the time of the incident) with a turnover of £38 million.

The Court held that the cash reserves represented a substantial hurdle to Aviva’s case that the Claimant’s controlling shareholder, Mr Malhotra, had motive to commit fraud to obtain a payment in relation to damage to the hotel. To that end, the Judge pointed out that any payment made would have been diminished in covering the immediate clean-up costs (which had already been incurred by the Claimant) and the costs of repair and refurbishment. There was therefore no evidence of a financial motive sufficient to explain why the Claimant would have caused the incident. In fact, all necessary steps to reinstate the hotel had been taken, without the benefit of an interim payment from Aviva.

The proper approach to the construction of fraud conditions

The Fraud Condition

The policy included a fraud condition, which read:

"If a claim made by You or anyone acting on your behalf is fraudulent or fraudulently exaggerated or supported by a false statement or fraudulent means or fraudulent evidence is provided to support the claim, We may:

(1) refuse to pay the claim”

(the “Fraud Condition”).

In addition to the allegation that the escape of water was deliberately induced by the Claimant, Aviva made various submissions in respect of statements made by the Claimant’s employees and associates to Aviva’s loss adjusters. Those allegations included:

1. That the Claimant’s Estates Manager, Mr. Vadhera, who discovered the escape of water, was not an honest witness and had good reasons to be willing to lie in order to support the Claimant's insurance claim, including that:

a) he had been the Claimant’s Estates Manager since 2019, overseeing 20 members of staff, and was responsible for 20 - 30 properties;

b) there was a close personal relationship between Mr Malhotra and Mr. Vadhera dating back nearly three decades;

c) Mr Vadhera was personally and financially indebted to the Claimant, due to various substantial loans;

d) Mr Vadhera was the sole director of a construction company owned by Mr Malhotra;

e) his testimony was that, upon discovery of the escape of water, he saw the cold water tank overspill, which on Aviva’s case, would not have occurred without the connected tanks also overspilling (when in fact, the Judge found that the tank in question did overspill); and

f) he told loss adjusters that he had apologised to Mr Malhotra for disturbing his birthday on the day of the incident, when in fact it was not Mr Malhotra’s actual birthday (incidentally, it was found that Mr Malhotra was indeed celebrating his 60th birthday on that day).

2. That Atul Malhotra, Mr Malhotra’s son and the sole director of the Claimant, had lied about the whereabouts of the valve that had caused the escape of water (when in fact, he had simply not appreciated what the plumbers had handed him during the cleaning works, it being in a dissembled state and in a plastic bag).

3. That Mr Malhotra lied to loss adjusters about Mr Vadhera finding insulation in the overflow of the cold-water tank (when in fact, the evidence supported that there was indeed insulation in the overflow, there was no benefit to the Claimant in it being Mr Vadhera who discovered it, and in any event who discovered it was immaterial to the claim).

4. That Mr Malhotra told loss adjusters that Mr Vadhera told him of what he had discovered on 12 July 2020, when it must have been 11 July 2020 (which was immaterial to the claim and provided no benefit to the Claimant).

Regardless, Aviva’s position was that the Fraud Condition had been breached such that it was entitled to refuse the claim.

An extension of the common law position

The common law has long prohibited recovery from an insurer where the insured’s claim has been fabricated or dishonestly exaggerated, a principle known as the fraudulent claims rule. In The Aegeon [2002] EWHC 1558 (Comm) Mance LJ extended that rule to apply to ‘collateral lies’ (i.e. fraudulent statements made in support of claims which are otherwise valid) which are material in that they:

a) directly relate to the claim;

b) are intended to improve the assured’s prospects of obtaining a settlement or winning the case; and

c) if believed, are objectively capable of yielding a not insignificant improvement in the insured’s prospects of obtaining a settlement or better settlement.

However, Versloot Dredging BV v HDI Gerling [2017] 1 AC 1 abolished that doctrine, establishing that the fraudulent claims rule does not apply to collateral lies. Giving a dissenting judgment, Lord Mance indicated that he would have upheld the test in The Aegeon, subject to potentially raising the threshold of materiality from a requirement for 'a not insignificant improvement' to the insured's prospects, requiring instead ‘a significant improvement’.

After Versloot, policy provisions purportedly allowing an insurer to reject a claim pursuant to collateral lies go further than the common law position. In Malhotra Leisure, the Judge accepted the Claimant’s submission that - in the absence of very clear words to the contrary - fraud conditions which seek to write in a power to decline claims on the basis of collateral lies should be read as taking effect subject to the limitations of the old common law doctrine, as set out in The Aegeon and modified in Versloot.

The specific wording of the Fraud Condition

The Judge further considered whether, by referring to a 'false' as opposed to 'fraudulent' or 'dishonest' statement in the Fraud Condition, the parties were intending that any false statement, including a statement made carelessly or without knowing it to be untrue, should be enough to entitle Aviva to reject a claim.

In finding that this was not the intention, he referred to the language of the Fraud Condition, which makes clear that it is dealing with fraudulent claims and collateral lies. In other words, the Court held that the Fraud Condition intended to address a situation where there was dishonesty, and did not apply to false statements made carelessly or innocently. Further, the wording of the Fraud Condition required that any false statement support the Claimant’s claim. In other words, it only applied to false statements made to assist in persuading Aviva to pay the claim, consistent with the common law position (both before and after Versloot).

Since there was no evidence of dishonesty on behalf of Mr Malhotra or any of the Claimant’s employees and/or associates, the Judge held that the Fraud Condition had not been breached and the Claimant was entitled to an indemnity in respect of the claim.

Key takeaways for policyholders

The obiter guidance in Malhotra Leisure on the interpretation of fraud conditions in insurance policies provides welcome protection for policyholders and reads as a cautionary tale for insurers. Allegations of dishonesty and fraud cannot be pleaded lightly, and there are professional obligations on insurers to first ensure that reasonably credible evidence exists establishing a prima facie case of fraud.

Following Malhotra Leisure, it is clear that courts will interpret conditions seeking to provide an insurer with the power to decline claims on the basis of collateral lies, subject to limitations of the old common law doctrine. In short, any collateral lie covered by a fraud condition must directly relate to the claim, be intended to improve the insured’s prospects and be capable of yielding a significant improvement in the insured’s prospects of obtaining a settlement or better settlement. Many of the allegations made in this case, including immaterial points such as whether Mr Malhotra was celebrating his birthday, and whether he was told certain facts on one day or the next, were never going to pass that test, and only served to distract from what was an otherwise covered claim.

Citation: Malhotra Leisure Ltd v Aviva Insurance Limited [2025] EWHC 1090 (Comm)

Abiigail Smith is an Associate at Fenchurch Law

Fenchurch Law warns the clock is ticking for Covid-19 Business Interruption claims

Fenchurch Law, the UK’s leading firm for insurance policyholders, has issued a warning to brokers to ensure their clients file any Covid-19 business interruption (BI) claims now, before they are time-barred.

Five years on from the pandemic, experts at Fenchurch Law are highlighting that the limitation period for Covid-19 BI claims will expire in March 2026, leaving affected businesses with less than a year to act.

Over the last five years, a series of high-profile battles between insurers and policyholders in the UK over BI wordings have expanded the scope of BI policies. The result is that policyholders now have more potential opportunities to receive compensation for the loss of business during the early months of the pandemic.

Fenchurch Law’s Managing Partner, Joanna Grant, warns that brokers need to act now to give their clients the best chance of success:

“Many industries were decimated by the pandemic that swept the world in 2020, with few more severely impacted than the hospitality industry, the long periods of lockdown taking a significant toll.

“During the last five years, we’ve fought for clients to get a fair outcome from their insurers. Though the pandemic was unprecedented, insurance policy wordings should be fair, proportionate and transparent, and we have found time and time again, that this was not the case. We’re still coming up against legal challenges regarding how to apply policy wordings, most recently the Non-Damage Denial of Access appeal brought by Liberty, which found for policyholders in holding that in composite policies, 'any one loss' limits applied separately to each policyholder rather than in aggregate across all policyholders. We are also involved in new cases being issued in court, including most recently a claim brought by the owner of the Franco Manca chain of pizzerias against QIC in respect of their Covid-19 losses.

For some businesses, there may be a long road ahead, so we urge brokers start talking to clients now, long before the liability period runs out.”

Joanna Grant is the Managing Partner of Fenchurch Law UK

The Good, the Bad & the Ugly: #25 The Good turned Ugly: Lonham Group Ltd v Scotbeef Ltd & DS Storage Ltd (in liquidation) [2025] EWCA Civ 203

Welcome to the latest in the series of blogs from Fenchurch Law: 100 cases every policyholder needs to know. An opinionated and practical guide to the most important insurance decisions relating to the London / English insurance markets, all looked at from a pro-policyholder perspective.

Some cases are correctly decided and positive for policyholders. We celebrate those cases as The Good.

In our view, some cases are bad for policyholders, wrongly decided and in need of being overturned. We highlight those decisions as The Bad.

Other cases are bad for policyholders but seem (even to our policyholder-tinted eyes) to be correctly decided. Those cases can trip up even the most honest policyholder with the most genuine claim. We put the hazard lights on those cases as The Ugly.

#25 The Good turned Ugly: Lonham Group Limited v Scotbeef Limited & DS Storage Limited (in liquidation)

Introduction

In a highly anticipated appeal concerning the Insurance Act 2015 (“the Act”), the Court of Appeal has offered the first guidance on the operation of Parts 2 and 3, and the characterisation of representations, warranties and conditions precedent.

Background

D&S Storage Limited (“D&S”) provided refrigeration and transport services to Scotbeef Limited (“Scotbeef”), who are producers and distributors of meat. In October 2019, D&S transferred six pallets of mould contaminated meat to Scotbeef. The meat was unfit for consumption by humans and/or animals and was consequently destroyed, leading Scotbeef to issue a claim against D&S for £395,588.

Initially, D&S sought to limit its liability to £25,000 on the basis that the Food Storage and Distribution Federation terms (“FSDF Terms”) (which included a £250 per tonne liability limit for defective meat) had been incorporated into its contract with Scotbeef. The Court disagreed, finding that the FSDF Terms were not incorporated into the contract, and that Scotbeef’s claim was not limited in value.

The first instance decision triggered D&S’ insolvency, and Scotbeef sought to pursue the claim directly against D&S’ insurer, Lonham Group Limited (“the Insurer”) pursuant to the Third Parties (Rights Against Insurers) Act 2010.

The Insurer defended the claim on the basis that D&S had failed to comply with a condition precedent in the Policy by not incorporating the FSDF Terms into the contract.

The Policy

The Policy contained a “Duty of Assured” clause that read:

"Conditions

General Conditions, Exclusions, and Observance…

DUTY OF ASSURED CLAUSE

It is a condition precedent to liability of [the Insurer] hereunder:-

(i) that [D&S] makes a full declaration of all current trading conditions at inception of the policy period;

(ii) that during the currency of this policy [D&S] continuously trades under the conditions declared and approved by [the Insurer] in writing;

(iii) that [D&S] shall take all reasonable and practicable steps to ensure that their trading conditions are incorporated in all contracts entered into by [it]. Reasonable steps are considered by [the Insurer] to be the following but not limited to… [various examples relating to incorporation of terms and conditions were set out]…"

(Our emphasis)

The following term was also included elsewhere in the Policy:

"The effect of a breach of condition precedent is that [the Insurers] are entitled to avoid the claim in its entirety.”

The High Court decision

Section 9 of the Act expressly prohibits an Insurer from converting a representation into a warranty or a condition precedent, whether by declaring the representation to form the basis of the contract or otherwise.

The High Court found that although sub-clause (i) was expressed as a condition precedent, it was in fact a representation about the insured’s trading position at the inception of the Policy. As such, it fell to be considered under Part 2 of the Act, which deals with the fair presentation of the risk.

As the Insurer had not based their defence on a breach of the duty of fair presentation and had not claimed any of the Section 8 proportionate remedies (such as part reduction in the claim), they could not rely on sub-clause (i) to repudiate liability.

Adopting a pro-policyholder interpretation, the Court held that each of the sub-clauses in the Duty of Assured clause had to be read together, meaning that sub-clauses (ii) and (iii) could not be relied upon either.

The Insurer appealed.

The Court of Appeal decision

Whilst the Court of Appeal agreed that sub-clause (i) was a pre-contractual representation dealing with existing contracts at policy inception, they disagreed that sub-clauses (ii) and (iii) had to be classified in the same way, stating that “the way they are grouped together in the policy does not justify… the “all or nothing” collective approach that was adopted by the judge."

That being the case, the heart of the appeal went to the characterisation of sub-clauses (ii) and (iii), and whether they were warranties and/or conditions precedent.

Answering that question, the Court ruled that the wording was clear, and that on a proper construction, sub-clauses (ii) and (iii) were warranties and conditions precedent to liability covering D&S’ future business operations, because:

- They were included under the heading “General Conditions, Exclusions and Observance”.

- The heading of the clause included the word “duty”, synonymous with an ongoing responsibility, obligation or burden.

- It was stated, in no uncertain terms, that the clause was “a condition precedent to liability”.

- The Policy contained, elsewhere, the following wording: “The effect of a breach of condition precedent is that [the Insurers] are entitled to avoid the claim in its entirety”.