Insurance amid uncertainty: Implications of the Iran conflict for Policyholders

On 28 February 2026, the US and Israel launched a coordinated military operation against the Iranian regime. Iran has since responded with missile and drone attacks across the Gulf, creating risk across several major trading centres including Qatar, Bahrain, Oman, Saudi Arabia and the UAE.

In addition to the very real and devastating risk to life, the escalation of the conflict is causing significant disruption to global trade, transport and energy markets alongside extensive physical damage to insured property.

Below, we consider the implications of the conflict for policyholders across key classes of business, and the coverage disputes that may arise as claims emerge.

STANDARD WAR EXCLUSIONS IN PROPERTY INSURANCE POLICIES

Standard commercial property policies typically exclude damage or loss “directly or indirectly” caused by “war, invasion, acts of foreign enemies, hostilities (whether war be declared or not)…military or usurped power”, and whilst the parties to the conflict are yet to formally declare war, whether the conflict amounts to war under the rules of contractual interpretation is a separate question.

Since the 1930s, English courts have said that “war” does not have a technical meaning and should be interpreted in a “common sense way”. Since then, caselaw has provided deliberately wide guidance as to the definition of war, including the presence of opposing sides and the number of combatants involved.

The breadth of that definition, together with standard war exclusions which override the concept of proximate cause (by applying to damage / loss even indirectly caused by war), mean that many commercial insureds are without the benefit of war-related property cover under their standard property insurance policies. An unwelcome consequence of that is that significant business interruption losses following airport closures, port shutdowns, supply chain disruption and government restrictions are likely to fall outside of the scope of cover.

Much will depend on the precise wording of the exclusion and the factual matrix of the loss. We recommend that property and business interruption policies be scrutinised for war exclusions as soon as possible and, in addition, policyholders across the leisure and manufacturing industries assess their force majeure exposure under supply and services contracts.

THE “GRIP OF THE PERIL” DOCTRINE IN AVIATION AND MARINE INSURANCE

In light of the above, policyholders may look to recover under specific political violence / war risk insurance policies and extensions.

In June last year, we reported on the long awaited Russian aviation judgment handed down by the Commercial Court. The trial involved the detention of Western-leased aircraft following Russia’s invasion of the Ukraine in 2022. You can read our analysis of that decision here - Commercial Court grounds War Risks insurers in landmark Russian aircraft judgment - Fenchurch Law.

Of particular concern to policyholders was Mr Justice Butcher’s commentary on “the grip of the peril” doctrine. He held that:

“if an insured is, within the policy period, deprived of possession of the relevant property by the operation of a peril insured against and, in circumstances which the insured cannot reasonably prevent, that deprivation of possession develops after the end of the policy period into a permanent deprivation by way of a sequence of events following in the ordinary course from the peril insured against which has operated during the policy period, then the insured is entitled to an indemnity under the policy.”

He concluded that lessors whose cover had been terminated by insurers prior to the point at which the court considered they had been permanently deprived of the aircraft were entitled to cover, on the basis that the loss of the aircraft arose in a sequence of events that followed in the ordinary course of restraints and detentions that took place in the policy period. In other words, the aircraft were in the grip of the peril by the time the relevant policies were terminated.

That ruling may be of particular relevance to aviation and marine policyholders affected by the present conflict. As a result of the closure of airspace, airline fleets remain grounded across the Gulf. Those fleets are at considerable risk of being permanently lost as a result of missile strikes on airports in Dubai, Abu Dhabi, Bahrain and Kuwait. Whilst the market will no doubt issue review notices to terminate or vary cover in those instances (as they did in the Russian aviation case), its possible that insured aircraft may already be deemed in the grip of the peril depending on the precise factual and temporal sequence of events.

Similarly, in relation to marine insurance, standard hull and cargo policies also exclude war and political perils. As a result, shipowners and charterers trading in high‑risk areas typically rely on separate war risks policies which are cancellable on short notice, requiring vessels to leave designated danger zones within a defined period. We know that cancellation notices have already been issued in respect of the current conflict so, where those vessels are unable to leave for whatever reason (for example, as a result of port closures or government restrictions), the grip of the peril doctrine may become relevant.

Whilst that analysis may offer some comfort to certain policyholders with property in the conflict zone, political violence policies include their own standard exclusions, and losses caused by perils not purchased will be excluded in any event. If, for example, an insured has only purchased terrorism or civil unrest cover, they are likely to be uninsured for war-related losses.

We recommend that political violence and war risks cover be analysed immediately, alongside the delay provisions in any related sale and trade contracts.

AGGREGATION WORDING

Where losses are covered, significant disputes may arise in relation to aggregation. Iran’s missile and drone attacks have, to date, been segmented and geographically dispersed, raising questions as to whether losses arise from a single event, a series of related events, or multiple separate occurrences for the purposes of policy limits, deductibles and excess erosion.

Whilst the outcome of any dispute is likely to be driven by the aggregation wording in a specific policy, insurers are likely to argue for a narrow interpretation and policyholders should be alive to that issue.

POLITICAL RISK AND TRADE CREDIT INSURANCE

Finally, unlike political violence policies, political risk policies do not require physical damage to trigger cover. They insure against, for example, the confiscation or deprivation of assets and are concerned with the permanent or prolonged loss of rights in, or control over, those assets. Outcomes under these policies are likely to be driven by the definition of expropriation, whether the deprivation is permanent for the purpose of the policy terms, and any relevant waiting periods.

Also written within the political risk market is trade credit insurance. As the conflict progresses, disruption to energy sources and supply chains may impact a policyholder’s ability to perform its payment obligations under a contract. In those circumstances, whilst trade credit policies are likely to contain fewer war exclusions than property or marine policies, policyholders may still have challenges to overcome in relation to causation and aggregation.

CONCLUSION

Already, the market is taking steps to limit its exposure to the conflict by making amendments to certain wordings, and issuing cancellation notices in respect of hull and cargo. Policyholders would be well placed to undertake early analysis of policy terms, particularly in relation to relevant exclusions and the likely interpretation of aggregation wording. Early, careful engagement with policy wording and claims strategy will place policyholders in the strongest possible position as the insurance consequences of the conflict continue to unfold.

Author

Daniel Robin, Managing Partner

Abigail Smith, Associate

When Policies Collide – Untangling “Other Insurance” Clauses

At our recent London Symposium, Associate Abigail Smith discussed the potential challenges posed by other insurance clauses in insurance policies. The session covered:

- The genesis of these clauses;

- The types of other insurance clauses used to limit an insurer’s liability in the event of double insurance; and

- How competing other insurance clauses are interpreted, in practice.

What is double insurance?

Double insurance occurs when the same party is insured with two or more insurers in respect of the same interest on the same subject matter against the same risk. In other words, it occurs where an insured’s loss is covered under two or more separate policies. Whilst it can be a commercially prudent guard against insurer insolvency, it most often arises inadvertently (for example, where a composite policy overlaps with dedicated cover).

The common law position

Under common law, a policyholder that is double insured for its loss can claim against whichever policy or policies it chooses, in whichever order it chooses, subject to each policy’s limits. Then, to ensure the risk is fairly distributed between insurers, the paying insurer is entitled to claim a contribution from the non-paying insurer (a principle known as rateable contribution – Drake v Provident [2003]).

Industry challenges

Unfortunately, the common law position gives rise to some complicated issues.

The main issue is that, because there is no general rule or common law duty requiring a policyholder to disclose that it is double insured, unless an insurer asks the question directly, or notification of other insurance is a condition of the policy, a paying insurer may not be aware that they are entitled to claim a contribution.

Adding another layer of complexity, the limitation period for bringing a contribution claim is two years from the date that the right accrued under section 10(1) Limitation Act 1980. That date, which is likely to be the date of a judgment, settlement or arbitration award, is not necessarily when an insurer becomes aware that they are entitled to a contribution. In fact, with no duty to disclose, it is possible for limitation to expire without an insurer ever knowing that it had been entitled to a contribution.

Types of “other insurance” clauses

It was in recognising these challenges that the industry came up with a solution: other insurance clauses, which are standard clauses in insurance policies which limit an insurer’s liability in circumstances where another policy covers the same loss.

In The National Farmers Union Mutual Insurance Society Limited v HSBC Insurance (UK) Limited [2011], Gavin Kealey KC identified 3 main types of other insurance clauses, being:

- Escape Clauses – those that exclude cover altogether in the event that another policy covers the same loss.

- Excess Clauses – those that state that the policy will only respond in excess of any other insurance.

- Rateable Proportion Clauses – those that limit an insurer’s liability in proportion to the total cover available.

Abigail explored how each type of clause is interpreted, and how competing clauses interact, in practice.

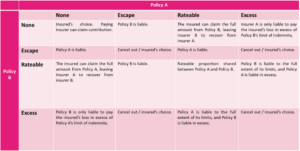

Escape Clauses

Owing to the fact that Escape Clauses seek to exclude cover altogether in the event of double insurance, there was at the outset the potential for policyholders to be left without any cover at all where two or more policies each included an Escape Clause.

That issue was addressed in Weddell v Road Transport [1932], with the Court ruling that it would be unreasonable to leave a policyholder without any primary cover in circumstances where multiple policies were in place and multiple premiums had been paid. As such, where two or more policies include an Escape Clause, they will cancel each other out so that the policyholder can claim against whichever policy (or policies) it chooses (essentially reverting to the common law position).

Excess Clauses

The same question was more recently considered in Watford Community Housing v Athur J Gallagher Insurance Brokers Limited [2025], this time in respect of Excess Clauses. Ultimately, the Commercial Court held that, because Excess Clauses also seek to avoid primary liability in the event of other insurance, they cancel each other out in the same way that Escape Clauses do.

Escape Clause v Excess Clause

Whilst there’s no English authority addressing a scenario in which two or more policies include competing Escape and Excess Clauses, Australian caselaw does provide some assistance.

In Allianz Insurance Australia Ltd v Certain Underwriters at Lloyds of London [2019] the New South Wales Court of Appeal held that competing Escape and Excess Clauses would also cancel each other out on the basis that both seek to avoid primary liability in the event of double insurance – an Escape Clause seeks to avoid any liability, whilst an Excess Clause recognises only a secondary one.

The New Zealand courts, by contrast Abigail noted, have on one occasion reached the conclusion that an Escape Clause will prevail (albeit relying heavily on the insurance provisions in an underlying contract). As such, the outcome will always come down to the specific policy wording and the wider context; “there is no universal hierarchy that automatically applies.”

Rateable Proportion Clauses

The final type of other insurance clause limits an insurer’s share of the loss in proportion to the policy limit. For example:

- An insured incurred £900,000 of loss covered under two separate policies.

- Policy A with a limit of £1m, and Policy B with a limit of £2m.

- Policy A’s insurer would be liable for 1/3 of the loss (their £1m portion of the total £3m insured), which is £300,000, and Policy B’s insurer would be liable for 2/3 which is £600,000.

If Policy A contained a Rateable Proportion Clause, and Policy B was silent, Policy B’s insurer would have to pay the whole of the loss and then claim a contribution from Policy A’s insurer.

Rateable Proportion Clause v Escape / Excess Clause

Unlike Escape and Excess Clauses, Rateable Proportion Clauses acknowledge that an insurer does have a primary liability in the event of other insurance, albeit a limited one. For that reason, an Escape or Excess Clause will prevail over a Rateable Proportion Clause.

If Policy A included a Rateable Proportion Clause whilst Policy B included an Escape Clause, the effect of the Escape Clause is that there would be no double insurance and Policy A’s insurer would be liable for the loss without being entitled to claim a contribution from Policy B’s insurer.

Whilst there has been some controversy over how an Excess Clauses might compete with a Rateable Proportion Clause (Austin v Zurich [1944]), in NFU v HSBC, Gavin Kealey KC sought to clarify the position. He remarked that, as a matter of construction, an Excess Clause should prevail over a Rateable Proportion Clause because a Rateable Proportion Clause recognises that an insurer has a primary liability in the event of double insurance, whereas an Excess Clause does not.

Abigail produced the table below as a starting guide for interpreting competing clauses, but was careful to note that the position will always depend on the policy wording, and the wider context.

Remaining questions

One issue that the courts are yet to address is whether, where an insured has multiple policies forming a horizontal primary layer of cover, followed by an excess layer that sits above, the entire horizontal layer must be exhausted before the excess policy responds.

The issue hasn’t arisen in caselaw to date, but Abigail remarked that it will be interesting to see how the courts approach the question when the times comes.

Key takeaways

The good news, for policyholders, is that the courts have so far refused to entertain any scenario in which an insured is left without primary cover.

That doesn’t mean, Abigail warns, that other insurance is an insurer’s problem. In circumstances where an Escape or Excess Clause prevails, an insured can be left without access to a policy that it paid a premium for, and which may well be preferable on its terms. Similarly, the disadvantage of Rateable Proportion Clauses from an insureds point of view is that the risk of insurer insolvency transfers back to the insured.

For those reasons, it is worth understanding whether there is another policy that responds to a risk and, if so, how any other insurance provisions might be interpreted.

Author

Abigail Smith, Associate

When Clauses Collide: Court of Appeal Backs MRC Over New York Arbitration

A recent Court of Appeal decision, Tyson International Company Ltd v GIC Re, India, Corporate Member Ltd [2026] EWCA Civ 40, provides valuable clarification on the approach taken by English courts when confronted with conflicting jurisdiction and arbitration provisions contained within layered reinsurance documentation.

Background:

Tyson International Company Ltd (“TICL”) is the Bermudan captive insurer for Tyson Foods, a major US‑based global food producer. In 2021, TICL arranged facultative reinsurance for its property risks with several reinsurers, including GIC Re, India, Corporate Member Ltd (“GIC”).

Two layers of facultative reinsurance were first placed on 30 June 2021 by way of a London Market Reform Contract (the “MRC”). The MRC provided for English governing law and contained a clause granting the courts of England and Wales exclusive jurisdiction over all matters relating to the reinsurance.

On 9 July 2021, this placement was supplemented by the execution of a second set of contracts in the form of the Market Uniform Reinsurance Agreement (the “Certificate”). The Certificate, instead, required disputes to be resolved by arbitration in New York under New York law. They also incorporated three amendments, the second of which stated that the MRC would “take precedence over reinsurance certificate in case of confusion” (the “Confusion Clause”).

A fire at a Tyson Foods facility in Hanceville, Alabama on 30 July 2021 gave rise to a claim under the captive policy. TICL accepted coverage and notified GIC. GIC later purported to rescind its reinsurance participation based on alleged misrepresentation relating to property valuations. TICL commenced proceedings in England relying on the jurisdiction clause in the MRC, while GIC sought to compel New York arbitration under the Certificate.

At first instance, the Commercial Court granted TICL a permanent anti‑suit injunction restraining GIC from pursuing the New York arbitration. In response, GIC appealed to the Court of Appeal.

Parties’ positions and key issues:

GIC’s principal argument was that the Confusion Clause was narrow in scope and applied only to internal drafting inconsistencies within the Certificate itself. GIC also maintained that, even if the clause applied more broadly, the English jurisdiction clause in the MRC and the New York arbitration clause in the Certificate should be read together in a manner that gave effect to both, with the English courts assuming a supervisory role over arbitration in New York.

TICL submitted that the Confusion Clause operated as a genuine hierarchy provision intended to resolve inconsistencies between the two documents. Once invoked, it required the English governing law and exclusive jurisdiction provisions in the MRC to prevail, leaving no room for the New York arbitration clause to operate.

Hence, the key issues for consideration were:

- The proper construction of the Confusion Clause; and

- Whether the English jurisdiction clause in the MRC and the New York arbitration clause in the Certificate could operate together

Analysis:

- The proper construction of the Confusion Clause:

GIC submitted that the Confusion Clause applied only where the Certificate itself contained internal inconsistencies and did not extend to conflicts between the Certificate and the MRC. The Court rejected this interpretation. It held that the natural and commercially coherent meaning of the wording was that it addressed inconsistency arising between the two documents. The MRC and Certificate were executed nine days apart and contained materially different provisions; it was, thus, far more plausible that the clause was intended to identify the document that should prevail where such differences arose.

Critically, the Court also commented that GIC’s narrow construction would be commercially unsound in rendering the clause ineffective when the most obvious form of “confusion” occurred; namely, a contradiction between the documents themselves.

- Whether the English jurisdiction clause and New York arbitration clause could operate together?

GIC argued that even if the MRC prevailed, the English jurisdiction clause could be read as supervisory or auxiliary to New York arbitration. The Court, however, rejected this in finding that the MRC conferred exclusive jurisdiction on the English courts in clear and unqualified terms, while the Certificates mandated binding arbitration in New York. To reinterpret the English clause as merely supervisory would invert the contractual hierarchy expressly agreed through the Confusion Clause and substantially distort the meaning of the exclusive jurisdiction provision.

The permanent anti‑suit injunction was, therefore, correctly granted.

Conclusion:

The decision provides clear confirmation that ordinary principles of contractual interpretation remain paramount in resolving disputes arising from inconsistent reinsurance documentation. The Court emphasised that where parties have chosen express language, particularly as to precedence, the courts will give effect to that language according to its natural and literal meaning. It is not the role of the court to retrospectively correct what may, in hindsight, be commercially disadvantageous to one party, nor to remodel the parties’ bargain by reading fundamentally inconsistent clauses together.

Authors

Michael Robin, Partner

Pawinder Manak, Trainee Solicitor

Motor Finance and the FCA Redress Scheme: Insurance Coverage implications for policyholders

Background and Supreme Court Decision

The UK Supreme Court’s judgment in Hopcraft v Close Brothers Ltd, together with Johnson & Wrench v FirstRand Bank Limited [2025] UKSC 33, clarified the law on secret commissions in motor finance. The Court held that car dealers arranging finance do not owe fiduciary duties to customers, which removed the foundation for claims based on breach of fiduciary duty. It also confirmed that English law does not recognise a free‑standing tort of “bribery” or secret commission absent a fiduciary relationship.

However, the Court significantly tightened the standard for commission disclosure. It held that a statement that “a commission may be paid” is inadequate: lenders and brokers must disclose both the fact and the amount, or the basis, of any commission prior to the finance agreement being signed. The Court reaffirmed that undisclosed or partially undisclosed commissions can render a lender–borrower relationship “unfair” under section 140A of the Consumer Credit Act 1974.

In Johnson, the Court found an unfair relationship where an entirely undisclosed commission – approximately 55% of the total loan– created a misleading impression and contributed to the unfairness. This was held to be sufficiently opaque and extreme to create an unfair relationship, leading to an order that the lender refund the commission together with interest. In the other joined cases, however, the commission arrangements were either less substantial or subject to some level of disclosure, and the borrowers did not obtain relief. The Court also held that lenders can only be liable as accessories to a dealer’s misconduct if they acted dishonestly, which was not established on the facts.

FCA Industry‑Wide Redress Scheme

In response to the judgment, the FCA announced an industry redress scheme under s.404 FSMA, covering motor finance agreements entered from April 2007 to November 2024. The FCA has estimated that approximately 14 million agreements involved undisclosed or excessive commissions, and that around 44% (about 6.2 million loans) may be considered unfair under the new standards.

The FCA published its consultation on the mechanics of the scheme in December 2025, with responses due in early 2026. The FCA has indicated that, subject to feedback, the final rules are expected to be issued in mid‑2026, with the redress scheme going live shortly thereafter

Compensation is expected to average £700 per loan, which implies a total payout of around £8.2 billion, with the possibility that it could reach £9–10 billion. Firms will additionally incur substantial operational expenditure, estimated at £2.8 billion, to administer the scheme. Any FCA fines for misconduct would be imposed separately and would not form part of the compensation pool.

The proposed scheme requires lenders to identify affected customers and provide compensation directly. Dealers and brokers will be expected to supply relevant information, and lenders may attempt to recover a portion of the cost from brokers via indemnity arrangements.

Application to FI Liability Policies:

Motor finance lenders and brokers will look primarily to their professional indemnity (PI) or civil liability policies, and, in certain circumstances, to D&O policies. Many of these policy wordings will be bespoke to Financial Institutions (FIs).

FI PI policies cover claims arising from wrongful acts in the insured’s provision of professional services, which is likely to include providing consumer credit and complying with regulatory disclosure obligations. Many FI PI policies define a “Claim” in broad terms, often including civil claims and regulatory proceedings that could result in an order requiring payment of compensation. An FCA-mandated redress scheme is likely to fall squarely within this definition.

Moreover, if a firm fails to make the payments required under s.404 redress scheme, the FCA can treat that failure as a breach of its rules under s.404F(7) and use the full range of its enforcement powers, including directions, financial penalties and public censure, to compel compliance, while consumers also have a direct right of action under s.404B(1) to sue for the compensation owed. Additionally, the FCA may apply to the courts under its general powers (including ss.380–382 FSMA) to obtain orders compelling a firm to remedy the breach, meaning that both the FCA and the courts ultimately can require an FI to pay compensation. Hence, any such proceedings would, likely, satisfy the definition of a “Claim” sufficient to engage the insuring clause for cover.

Notwithstanding, various coverage issues may still arise as follows.

Key Coverage Issues

Issue 1: Whether Commission Refunds Constitute an Insured “Loss”

A central coverage question is whether returning commission and interest constitutes an insured “Loss.” PI policies usually cover damages or compensation that the insured is legally liable to pay. A redress scheme under s.404 can only compensate customers where they have a private legal remedy so insureds who pay compensation should be able to demonstrate to insurers that they had a legal liability.

As regards loss, the proposed redress scheme generally seeks to restore consumers to the position they would have been in if commissions had been properly disclosed, which suggests a compensatory purpose. However, there is no causation requirement under the FCA’s proposals, in that consumers will not have to prove that they would not have entered into the loan if full disclosure had been made (although the presumption that non-disclosure caused loss is rebuttable by lenders in certain circumstances, e.g. if the consumer was deemed to be “sophisticated”).

Insurers may argue that part of the relief is restitutionary because it involves disgorging a commission that the insured (or its agent) earned. Many PI policies exclude loss consisting of the return of fees or commissions. Some policies include “carve‑backs” where commissions are linked to a wrongful act by an employee, which can restore cover. Courts and insurers often distinguish between returning an improper gain (normally uninsurable) and compensating a third party’s financial loss (insurable).

While there remains a grey area, especially under policies that expressly exclude “improper profit,” it is likely that courts will view these payments as compensatory and therefore insurable. Nonetheless, disputes may arise where policy language is particularly broad or where a settlement includes elements that resemble pure disgorgement.

Issue 2: Regulatory Fines and Penalties

Although consumer compensation would probably be covered, regulatory fines are not. FI PI policies universally exclude fines, penalties, and punitive damages, either expressly or on the basis that they are uninsurable by law. Any FCA fines imposed in parallel to the redress scheme will therefore fall outside insurance cover. Statutory interest added to customer compensation is generally considered part of the damages and is normally covered.

Issue 3: Claims‑Made Basis and Notification

FI PI policies operate on a claims-made basis, making notification a central coverage issue. Many claims will arise in 2025–2026 when consumers complain or are deemed to do so under the scheme. Policies in force at that time should respond unless exclusions for known circumstances apply.

Insurers may seek to frame a failure to disclose commission levels as a material non-disclosure. This would require an insurer to show (i) the information would have influenced a prudent insurer in setting terms, and (ii) the policyholder knew (or ought reasonably to have known) the information. Historically, however, commission setting practices in motor finance were industry‑standard, widely known, and the regulatory risk was already in the public domain due to the FCA’s 2019 work. All of that, will make it harder for insurers to say they were “unaware” of the risk, or that non‑disclosure was material in a fair‑presentation sense.

Insurers are closely examining such arguments but are aware that the hurdle is relatively high, particularly as many had opportunities during renewals to ask targeted questions and add exclusions specifically targeting motor finance commission issues, as occurred with Arch Cru and BSPS.[i]

The effectiveness of “circumstance notifications” is, therefore, critical. Notifying when the Court of Appeal judgment was issued or when the Supreme Court granted permission to appeal would have preserved cover in the corresponding policy period, but insurers may argue that any such notifications were too late and not in accordance with the policy provisions. There may be disputes over when circumstances crystallised to the point of being notifiable. English case law suggests that something more than a remote possibility of claims is required, and the Court of Appeal’s expansive judgment in relation to commission disclosure arguably met that threshold.

Issue 4: Aggregation

Given the potential number of claims, aggregation will have a major impact on available limits and deductibles. PI policies often state that a series of related or continuous acts or omissions will be treated as a single claim, or that claims arising from the same originating source are treated as a single claim.

Depending on the policy wording therefore, all instances of inadequate commission disclosure by a single lender may constitute one aggregated claim.

This approach would benefit insurers in that it would cap the insurer’s liability at a single policy limit (often £10–20 million), regardless of the scale of consumer redress.

However, it would also benefit insureds in that it would mean that only one deductible applies.

Issue 5: Allocation Issues

Where a regulatory proceeding includes both compensatory and non‑compensatory elements, policies usually require allocation between covered and uncovered parts. Although fines are excluded, defence costs for regulatory investigations are often almost fully covered because the work typically relates to the compensatory issues as well.

Further, if policies do not provide for allocation, in accordance with the principle expounded in Wayne Tank and Pump Co Ltd v Employers Liability Assurance Corp [1974] QB 57, where regulatory proceedings are proximately caused by both covered and excluded matters, insurers may argue that the exclusion will prevail to preclude cover. However, it is important to note that Wayne Tank is not in fact authority that defence costs caused by two concurrent and interdependent proximate causes will be excluded, and the actual position is likely to turn on careful analysis of the policy (and the facts, as regards the reasons defence costs were incurred).

Wider Implications for Insurers and Intermediaries

This episode has substantial implications for financial services and insurance markets. PI underwriters are likely to adopt more restrictive terms, including specific exclusions, reduced limits, and higher deductibles. There may also be increased scrutiny of other products involving commission structures, such as mortgage broking or insurance distribution.

The scale of the redress means insurers will need to increase reserves and manage potential disputes within insurance towers, especially regarding aggregation and allocation. Insurers may also look to pursue subrogated claims against brokers under indemnity agreements. Reinsurers will also be significantly affected.

The ruling and redress programme reinforces the importance of transparency in remuneration across all intermediary sectors. Insurance brokers and financial intermediaries should reassess commission disclosure practices in light of the FCA’s broader focus on consumer fairness and the new Consumer Duty. Firms that continue opaque practices may face both regulatory scrutiny and increased insurance restrictions.

Although D&O exposure will, hopefully, be limited, senior managers may also face FCA attention under the Senior Managers & Certification Regime.

Conclusion

The motor finance commission litigation and resulting FCA action create extensive compensatory liabilities for lenders. FI PI policies are likely to respond, subject to limits, aggregation, notification requirements, and exclusions for fines and proven dishonesty. Commission refunds are most likely to be treated as compensatory and therefore insurable. The case underscores the importance of transparent consumer practices, early notification under claims‑made policies, and careful review of policy wording in the context of large‑scale regulatory actions.

[i] Arch Cru was a mis‑selling scandal involving investment funds marketed as low‑risk but in fact exposed to high‑risk, illiquid assets. When the funds collapsed in 2009, the FCA established a consumer redress scheme, and although many PI insurers argued that firms had breached the duty of fair presentation by failing to flag emerging regulatory concerns, those arguments were largely unsuccessful because the issues had already been widely publicised. Insurers later introduced Arch Cru‑specific exclusions once the risks became well known.

BSPS involved unsuitable advice given to steelworkers to transfer out of the British Steel Pension Scheme into riskier personal pensions. The FCA subsequently implemented a statutory redress scheme, and PI insurers again sought to rely on fair‑presentation breaches, but these arguments similarly gained little traction because the regulatory concerns were already in the public domain by the time many policies renewed. Insurers ultimately responded by adopting BSPS‑specific exclusions as the scale of the issue became apparent.

Authors

Chris Ives, Partner (Head of Financial Institutions)

Jonathan Corman, Partner

Pawinder Manak, Trainee Solicitor

First decision on s11 Insurance Act (causation test for breach of warranty)

Ever since the introduction of the Insurance Act 2015, there has been debate about how causation works in the context of section 11 and in particular the provision in sub-section 11(3) whereby the policyholder is excused from the usual consequences of a breach of warranty if it can show that its “non-compliance with the [warranty] could not have increased the risk of the loss which actually occurred in the circumstances in which it occurred.”

Policyholders had thus argued, despite the Law Commission having said this was not what it had intended, that this introduced a strict causation test. For example, where the policyholder had warranted that it had a burglar alarm but it failed to set it, it would (it argued) be open to it to show that this particular burglary was undertaken by thieves so sophisticated that setting the alarm would have made no difference - even if setting the alarm would decrease the risk of burglary in general.

Likewise, a policyholder would wish to argue that, on the actual facts of its loss, a warranty had been breached in only a minor respect, which made no difference, even if a more serious non-compliance would unquestionably have affected the likelihood of that particular loss.

This argument has now been considered, and rejected, by Mrs Justice Dias in her decision on 26 July in Mok Petro v Argo. This was a highly complex case concerning contaminated commodities, and the breach of warranty issue features only briefly at the end of the judgment. On that issue, the Judge said as follows:

“There is nothing in the wording of the section to suggest that where a term can be breached in more than one way, it is only the particular breach which must be looked at. On the contrary, it seems to me that section 11 is directed at the effect of compliance with the entire term and not with the consequences of the specific breach. … I therefore conclude that [Counsel for the Insurers] is right about this. There was no serious dispute that compliance with the warranty as a whole was capable of minimising the risk of water contamination … and that therefore non-compliance could have increased the risk of the loss which actually occurred.”

The full judgment is here: https://www.bailii.org/ew/cases/EWHC/Comm/2024/1555.pdf

Jonathan Corman is a Partner at Fenchurch Law.

CrowdStrike Outage - Insurance Recoveries

Many businesses have suffered losses following a catastrophic IT failure when an update released on 19 July by US cybersecurity firm, CrowdStrike, caused crashes on Microsoft Windows systems globally.

We are recommending that policyholders review the scope of coverage available under their cyber and property damage/business interruption insurance.

What to look out for:

- Is there cyber cover for system failure that responds to accidental (i.e. non-malicious) events such as this?

- Are there any relevant business interruption waiting periods to consider?

- What other losses are covered – such as the cost of data restoration, incident response and voluntary shutdown?

- Is there cover for supply chain failure?

- In the context of PD/BI policies, the ‘damage’ trigger will need careful consideration.

What steps do you need to take?:

- Ensure timely compliance with notification provisions and other claims conditions

- Have steps been taken to mitigate losses so far as possible?

- Make sure accurate records are kept of the sequence of events and the losses that have been incurred as a result of the outage.

Please get in touch if we can be of any assistance, or if you have any queries.

Joanna Grant is the Managing Partner of Fenchurch Law

Climate Risks Series, Part 1: Climate litigation and severe weather fuelling insurance coverage disputes

The global rise in climate litigation looks set to continue, with oil and gas companies increasingly accused of causing environmental damage, failing to prevent losses occurring, and improperly managing or disclosing climate risks. Implementation of decarbonisation and climate strategies is subject to scrutiny across all industry sectors, with claims proceeding in many jurisdictions seeking compensation for environmental harm as well as strategic influence over future regulatory, corporate or investment decisions.

Evolving risks associated with rising temperatures have significant implications for the (re)insurance market as commercial policyholders seek to mitigate exposure to physical damage caused by severe weather events; financial loss arising from business interruption; liability claims for environmental pollution, harmful products or ‘greenwashing’; reputational risks; and challenges associated with the transition towards clean energy sources and net zero emissions.

Litigation Trends

Cases in which climate change or its impacts are disputed have been brought by a wide range of claimants, across a broad spectrum of legal actions including nuisance, product liability, negligence, fiduciary duty, human rights and statutory planning regimes. Approximately 75% of cases so far have been commenced in the US, alongside a large number in Australia, the EU and UK.

Science plays a central role and can be critical to determining whether litigants have standing to sue. The emerging field of climate physics allows for quantification of greenhouse gas (“GHG”) emitters’ responsibility, with around 90 private and state-owned entities found to be responsible for approximately two-thirds of global carbon dioxide and methane emissions. Recent advances in scientific attribution may provide evidence for legal causation in claims relating to loss from climate change or severe storms, flooding or drought.

Directors of high-profile companies may be personally targeted in such claims as liable for breach of fiduciary duties to the company or its members, in failing to take action to respond to climate change, or approving policies that contribute to harmful emissions.

Recent Cases

An explosion of ‘climate lawfare’ has kicked off in recent years, with the cases highlighted below indicative of key themes.

Smith v Fonterra [2024]

The New Zealand Supreme Court reinstated claims, struck out by lower courts, allowing the claimant Māori leader with an interest in customary land to proceed with tort claims against seven of the country’s largest GHG emitting corporations, including a novel cause of action involving a duty to cease materially contributing to damage to the climate system. This was an interlocutory application and the refusal to strike out does not mean that the pleaded claims will ultimately succeed on the merits. However, the judgment is significant in demonstrating appellate courts’ willingness to respond to the existential threat of climate change by allowing innovative claims to be advanced and tested through evidence at trials.

R v Surrey County Council [2024]

In a case brought by Sarah Finch fighting the construction of a new oil well in Surrey, the UK Supreme Court (by a 3:2 majority) ruled that authorities must consider downstream GHG emissions created by use of a company’s products, when evaluating planning approvals. The Council’s decision to grant permission to a developer was held to be unlawful because the environmental impact assessment for the project did not include consideration of these “Scope 3” emissions, when it was clear that oil from the wells would be burned.

Verein KlimaSeniorinnen [2024]

An association of over 2,000 older Swiss women complained that authorities had not acted appropriately to develop and implement legislation and measures to mitigate the effects of climate change. The Grand Chamber of the European Court of Human Rights held that Article 8 of the European Convention encompasses a right for individuals to effective protection by state authorities from serious adverse effects of climate change on their life, health and wellbeing. Grand Chamber rulings are final and cannot be appealed: Switzerland is now required to take suitable measures to comply. While not binding on national courts elsewhere, the decision will be influential.

ClientEarth v Shell [2023]

The English High Court dismissed ClientEarth’s attempt to launch a derivative action against the directors of Shell plc in respect of their alleged failure to properly address the risks of climate change, indicating that claims of this nature brought by minority shareholders will face significant challenges. The Court noted that directors (especially those of large multinationals) need to balance a myriad of competing considerations in seeking to promote the success of the company, and courts will be reluctant to interfere with that discretion, making it harder to establish that directors have breached their statutory duties.

US Big Oil lawsuits

Following lengthy disputes over forum, proceedings against oil and gas companies in the US are gaining momentum, paving the way for the claims to be substantively examined in state courts. Many actions against the fossil fuel industry seek to establish that defendants knew the dangers posed by their products and deliberately concealed and misrepresented the facts, akin to deceptive promotion and failure to warn arguments relied upon in other mass tort claims in the US, arising from the supply of tobacco, firearms or opioids.

Implications for Policyholders

With increasing volatility and accumulation risk, insurers will look to mitigate exposures through wordings, exclusions, sub-limits and endorsements. The duty to defend is the first issue for liability insurers, given the number of policyholders affected and the potential sums at stake in indemnity and defence costs.

In 2021, the Lloyd’s Market Association published a model Climate Change Exclusion clause (LMA5570). Property policies exclude gradual deterioration, with express wording or impliedly by the requirement of fortuity, and liability insurance typically excludes claims arising from pollution.

Lawsuits have been filed in the US over insurance coverage for climate harm, including Aloha Petroleum v NUF Insurance Co of Pittsburgh (2022), arising from claims by Honolulu and Maui, and Everest v Gulf Oil (2022), involving energy operations in Connecticut. Policy coverage may depend on whether an “occurrence” or accident has taken place, as opposed to intentional acts or their reasonably anticipated consequences (Steadfast v AES Corp (2011).

Policyholders should review their insurance programmes with the benefit of professional advice to ensure adequate cover for potential property damage, liability exposures and legal defence costs.

In the following instalments of our Climate Risks Series, we will examine the impact of reinsurance schemes and parametric solutions, and coverage for storm and flood-related perils in light of recent claims experience.

Authors

Amy Lacey, Partner

Ayo Babatunde, Associate

Queenie Wong, Associate

"Top Down" still top law: RSA & Ors v Textainer

In the recent decision of Royal & Sun Alliance & Ors v Textainer Group Holdings Limited & Ors [2024] EWCA Civ 542, the Court of Appeal rejected an attempt by Insurers to avoid the application of the (seemingly) well-established “top down” principle to the allocation of recoveries.

Background

The (much simplified) background was as follows.

Textainer is one of the largest owners/suppliers of shipping containers.

In 2016, approximately 113,000 of its containers were on lease to a Korean company, Hanjin Shipping Co Limited (“Hanjin”). Hanjin became insolvent, and Textainer incurred a significant loss, partly in relation to containers which were never recovered and partly in relation to the cost of retrieving/repairing the others, as well as lost rental income.

Textainer had a “container lessee default” insurance programme, written in layers up to (for present purposes) $75 million, with a $5m retention. Textainer’s overall loss, as a result of Hanjin’s default, was approximately $100m. It absorbed the first $5m through its retention, and its primary and excess layer insurers (“Insurers”) paid out policy limits amounting to $75m, leaving an uninsured loss of $20m.

Textainer subsequently recovered approximately $15m in Hanjin’s liquidation.

Under ordinary “top down” principles, all of that recovery would have inured to Textainer. Insurers nevertheless claimed that they were entitled to a proportionate element of it (amounting, on the above figures, to approximately 75%).

The top down principle, and Insurers’ attempt to circumvent it

The top down approach to the allocation of recoveries was established by the House of Lords’ decision in Lord Napier and Ettrick v Hunter[1993] AC 713. It equates to assuming that the recoveries are made simultaneously with the loss and then considering how the net loss would be borne (ie, first by the retention/deductible, then by the primary layer, then carrying up the excess layers, and finally to the uninsured element).

Insurers argued that the policies in the present case were distinguishable from the stop loss policies considered in Napier. The stop loss policies, they argued, applied to a single (or "unitary") financial loss for a specified period of underwriting by the name. In contrast, the container lessee default policies did not (they argued) insure a unitary loss, but “covered the physical loss of or damage to individual containers and related costs/loss of earnings as and when those losses were incurred, eroding first the retention, then the layers of cover, one by one”.

Insurers argued that there was a fundamental distinction between the case of a single or unitary loss (as considered in Napier) and that of multiple losses, such as the present case. They argued that, although in the former case subsequent recoveries would reduce that single loss top down, where there were “multiple losses of different items of property at different times, recoveries in respect of those specific items not only could but must be allocated to the insurer who had indemnified against their loss”.

However, those arguments were at odds with the decision by Langley J in Kuwait Airways Corporation v Kuwait Insurance Co S.A.K [2000] 1 Lloyd’s Rep 252 (“Kuwait Airways”).

Kuwait Airways

In that case, the policyholder, Kuwait Airways (“KAC”), had lost 15 aircraft when they were seized Iraqi forces during the 1990 invasion of Kuwait. The relevant aviation insurers paid KAC the policy limits of $300m, leaving it with $392m of uninsured losses.

Subsequently, 8 of the aircraft, valued at c $395m, were recovered. Under conventional top down principles, that recovery would have inured to KAC, leaving its residual loss covered by the insurance payout.

The aviation insurers nevertheless attempted to have the value of the recovered aircrafts apportioned pro rata between them and KAC, on the supposed basis that “each aircraft loss was a separate loss, exemplified by the fact that each had its own agreed value in the policy, the premium was based on that value and…the payment made of $300m was in effect a payment of 300/692 of the agreed value of each aircraft”.

Langley J rejected that argument. He held that there could not be:

“… any justification for “disaggregating” recoveries where there is an aggregate limit to the indemnity. Moreover the aggregate limit (in the case of one occurrence) applied regardless of the number of aircraft lost…whether or not there were a number of losses or only one loss (there was certainly only occurrence) is my judgment nothing to the point…”.

He also held that:

“… that conclusion accords with commercial good sense. Had KAC lost only the 7 aircraft which were in fact destroyed, its insurers would unarguably have had to pay up to the limit of the indemnity without any recovery. It would be remarkable if the policy was to be so construed that, because KAC lost those 7 aircraft but also 8 others which were later recovered intact, insurers became entitled to a credit for proportion of the value of the aircraft recovered”.

Faced with those comments, which seemed to apply so closely to the present case, Insurers were compelled to submit that Kuwaiti Airwayscould be distinguished or, failing that, was wrongly decided.

The Court of Appeal’s decision

Insurers had lost in the Commercial Court in front of David Railton KC, sitting as a Deputy Judge, and were no more successful when they appealed to the Court of Appeal.

The Court of Appeal’s judgment was given by Phillips LJ, with Arnold & Falk LJJ concurring.

The Court of Appeal agreed with the Deputy Judge that the true nature of Textainer’s insurance was cover “against particular layers of loss” and that, if recoveries were not applied top down but proportionately to the insured layers as well as to the uninsured losses, Textainer would not receive the extent of the indemnity for which it had contracted. Moreover, Textainer would, if Insurers were correct, have been in a worse position than if the recoveries had been achieved before Insurers had paid out. By contrast, Dillon LJ, in the Court of Appeal in Napier, was clear that the outcome should be the same “whether the underwriters have or have not already paid the amount for which they are liable for the time the recovery is achieved”.

In short, the Court of Appeal agreed with Textainer that the reality was that the insurance was not provided in relation to individual containers, most of which, if lost, would eventually be recovered, but that “the real subject of the insurance is the multiple strands of lost rental, costs and expenses which will be ongoing and intertwined…”

Accordingly Insurers’ challenge to the top down principle failed.

Other issues

The Court of Appeal’s judgment covered two other issues.

(a) Which losses were paid by whom?

This was a factual issue. Some of Textainer’s containers had been leased to Hanjin on operating leases and some on finance leases. However, the settlement by the liquidator only applied to the containers supplied on operating leases.

This required Insurers to show (assuming their challenge to the top down principle had succeeded) precisely which containers they had indemnified and which formed part of Textainer’s uninsured loss. Only then could one allocate the recovery.

Insurers argued that there should be a “pragmatic assumption” that the losses in respect of finance leases would have occurred at the same time as, or at least in proportion to, losses in respect of operating leases, so that there was nothing to stop a pro rataapportionment of the recovery between insured and uninsured losses.

The Court of Appeal rejected that approach. It said it had been open to Insurers to adduce evidence on this issue and that, having failed to do so, they could not resort to an assumption.

(b) Under-insurance

Finally, Insurers sought belatedly to argue that, because there had been an element of uninsured loss, this indicated that Textainer had been under-insured and that its loss should be reduced by the application of average.

That argument failed. Phillips LJ held the concept of under-valuation or under-insurance has no relevance to insurance written in layers. Unlike a single policy insuring (say) a ship, where under-insurance exposes the insurer to the same risk (up to the limit of cover) but the premium has been unfairly supressed, where cover is written in layers, the cover by definition matches precisely the value of the risk which the insurer has accepted.

Conclusion

It is gratifying that Insurers’ attempt to circumvent the top down principle was so robustly rejected by the Court of Appeal. Likewise, its clarification that under-insurance and average have no relevance to insurance written in layers will also be welcomed by policyholders.

Non-damage property cover in political violence insurance: Hamilton Corporate Member Ltd v Afghan Global Insurance Ltd

On 12 June, the Commercial Court handed down judgment in an important case for the political violence insurance market regarding the meaning of “direct physical loss” and also of the seizure exclusion.

Hamilton Corporate Member Ltd v Afghan Global Insurance Ltd [2024] EWHC 1426 (Comm) arose out of the Western withdrawal from Afghanistan and the subsequent assumption of control by the Taliban. In August 2021, Anham, the original insured, lost its warehouse at the Bagram airbase in Afghanistan when it was seized by the Taliban. Anham sought to recover the US$41m loss under its political violence policy which had been issued by an Afghani insurer, which in turn was reinsured by the Claimant reinsurers.

The Exclusion

The reinsurers denied the claim (and sought summary judgment for a declaration of non-liability), relying on the following exclusion:

“Loss or damage directly or indirectly caused by seizure, confiscation, nationalisation, requisition, expropriation, detention, legal or illegal occupation of any property insured hereunder, embargo, condemnation, nor loss or damage to the Buildings and/or Contents by law, order, decree or regulation of any governing authority, nor for loss or damage arising from acts of contraband or illegal transportation or illegal trade.”

Anham sought to argue that the exclusion was inapplicable, on the grounds that in the context of the exclusion the “seizure” had to be carried out by a governing authority, which could not be said of the Taliban at the material time. However, the court (Calver J) had little difficulty in holding that the exclusion did apply, on the basis that in both settled case law and ordinary language “seizure” means “all acts of taking forcible possession, either by a lawful authority or by overpowering force”. Clearly, the Taliban fell into the latter category. The court also rejected Anham’s submission that it should not reach a decision without first hearing expert evidence as to how the political violence insurance market understood this exclusion.

Direct physical loss

The Judgment also shed light on how the Courts in this context will construe the “physical loss” of property.

The policy contained the following Interest provision:

“In respect of Property Damage only as a result of Direct physical loss of or damage to the interest insured”.

Likewise, Insuring Clause 2 indemnified Anham against “Physical loss or physical damage to the Buildings and Contents”.

Anham submitted that the warehouse had been lost, on the grounds that it had been irretrievably deprived of possession of it because of the Taliban. In making this argument, Anham sought to rely on the definition in the Marine Insurance Act 1906 of constructive total loss (namely, that, where an insured is deprived of his property and there is little chance of recovery, the courts will consider that a constructive total loss). However, Calver J unhesitatingly held that, in the context of a political violence insurance policy, “direct physical loss” meant physical destruction, not mere deprivation of use.

Interestingly, the Judgment did not cite cases such as Moore v Evans [1917] 1 KB 458 (CA) [1918] AC 185 (HL) or Holmes v Payne [1930] 2 KB 301, which held that the word “loss” was not qualified by the word “physical”.

Summary

The Judgment in Hamilton is plainly unhelpful to policyholders insured under the AFB Political Violence wording, which is widely used in the London market. Unless successfully appealed, (re)insurers are likely now to reject any claim based on this wording for loss of property where the hostile forces have not caused any actual damage to the insured interest, notwithstanding that their actions deprived the insured of the use of or access to it.

Authors

Jonathan Corman, Partner and Dru Corfield, Associate

No clear mistake and no clear cure – disappointing result in the Court of Appeal for W&I policyholder

A recent decision of the Court of Appeal, Project Angel Bidco Ltd (In Administration) v Axis Managing Agency Ltd & Ors [2024] EWCA Civ 446, provides guidance in relation to the interpretation of exclusion clauses and alleged drafting errors in warranty and indemnity (“W&I”) policies.

Background

The Parties

The Appellant, Project Angel Bidco Ltd (“PABL”), was insured under a W&I policy (“the Policy”).

PABL had purchased the shares in Knowsley Contractors Limited (trading as King Construction) (“King”). The Share and Purchase Agreement (“SPA”) included a number of warranties, listed in a Cover Spreadsheet to the Policy, including in relation to anti-corruption legislation.

King in fact became embroiled in allegations of corruption. It went into liquidation and PABL itself went into administration. PABL had paid £16.65 million for the shares. It claimed that the warranties had been incorrect, such that the true value of the shares was negligible or at most £5.2 million, and accordingly made a claim against the Respondents, Axis Managing Agency Limited and others (“Insurers”), for an indemnity under the Policy.

The Cover Spreadsheet

The Cover Spreadsheet contained a list of “Insured Obligations” which included warranties 13.5 (a) to (h) (“Warranty 13.5”). The spreadsheet contained the following rubric:

“Notwithstanding that a particular Insured Obligation is marked as “Covered” or “Partially Covered”, certain Loss arising from a Breach of such Insured Obligation may be excluded from cover pursuant to Clause 5 of the Policy.”

The Insured Obligations at Warranty 13.5 were all marked as “Covered”.

ABC Liability

The Policy stated that:

“The Underwriters shall not be liable to pay any Loss to the extent that it arises out of…

5.2.15. any ABC Liability” (“the ABC Liability Exclusion”).

ABC Liability was defined as "any liability or actual or alleged non-compliance by any member of the Target Group or any agent, affiliate or other third party in respect of Anti-Bribery and Anti-Corruption Laws”. [Emphasis added.]

The Overarching Issue

This appeal was concerned with the conflict between the “Covered” Insured Obligations at Warranty 13.5 and the ABC Liability Exclusion.

PABL argued that the scope of the Insured Obligations at Warranty 13.5 contradicted the ABC Liability Exclusion, as no loss arising out of a breach of Warranty 13.5 would ever be covered by the Policy. The Court explored the alleged conflict by asking four questions:

- Was there an inconsistency as alleged by PABL?

- If there was inconsistency, did the Policy resolve it?

- Was there something wrong with the language of the ABC Liability Exclusion?

- If a mistake had been made, was there a clear cure?

Was there an inconsistency?

Insurers argued that Warranty 13.5(e) (that the company maintained a record of all entertainment, hospitality and gifts received from a third party) and 13.5(h) (in relation to the award of contracts under the Public Contracts Regulations 2006) fell outside the exclusion. However, the Court of Appeal accepted there was a conflict between the entirety of Warranty 13.5 and the ABC Liability Exclusion.

Did the Policy resolve the inconsistency?

Insurers argued the structure of the Policy meant that the Cover Spreadsheet was subordinate to the ABC Liability Exclusion. This relegated the Cover Spreadsheet to being a “summary document”, purely intended to show which warranties were in scope of the Policy. The Court of Appeal disagreed, noting that the definition of “Insured Obligations” was linked to the Cover Spreadsheet.

Secondly, Insurers argued that the ABC Liability Exclusion was a heavily negotiated term and therefore more significant than the Cover Spreadsheet. The Court of Appeal accepted this, since the definition of ABC Liability was “detailed and wide ranging”, whereas the classification of warranties as “Covered”, “Excluded” or Partially Covered” was much broader.

Thirdly, Insurers argued the rubric in the Cover Spreadsheet showed that the ABC Liability Exclusion would take precedence, and the Court of Appeal agreed.

Was there something wrong with the language?

The Court of Appeal emphasised that, in order to correct an alleged error in a contract, it has to be clear there has been a mistake. In the first instance decision, the Judge had interpreted the ABC Liability Exclusion as follows:

“As drafted the definition would appear to cover three different species of ABC liability being:

- i) Any liability … in respect of Anti-Bribery and Anti-Corruption Laws;

- ii) Any … alleged non-compliance by any member of the Target Group or any agent, affiliate or other third party in respect of Anti-Bribery and Anti-Corruption Laws; and

iii) Any … actual … non-compliance by any member of the Target Group or any agent, affiliate or other third party in respect of Anti-Bribery and Anti-Corruption Laws.”

PABL objected to this interpretation on the grounds that a reasonable reader would expect the word “liability” to be used in the sense of liability “for” something, suggesting that the word “or” had been included by mistake and the ABC Liability definition should be interpreted as "any liability [f]or actual or alleged non-compliance …”.

The Court of Appeal concluded that, although liability would often be referred to in the context of responsibility “for” something, it would not be unusual to refer to liability “in respect of”, “arising from” or “in connection with” an excluded peril. Therefore, despite the apparent contradiction, there was nothing wrong with the language of the ABC Liability Exclusion and no drafting error could be established.

Was there an obvious cure?

For completeness, the Court of Appeal went on to consider whether there was a “clear cure” for the alleged mistake. Assuming that there was a contradiction between the ABC Liability Exclusion and Warranty 13.5 because of a drafting mistake, Insurers had a coherent and rational reason for wanting to avoid liability for loss arising out of ABC Liability, and it was unclear whether any supposed error was in the drafting of the ABC Liability exclusion or the Cover Spreadsheet. It was held therefore that no clear cure existed for the alleged mistake.

The Decision

In summary, the Court of Appeal by majority (Lewison LJ, with whom Arnold LJ agreed) found in favour of Insurers and the appeal was dismissed.

In a dissenting judgment, Phillips LJ found in favour of PABL, concluding that there was a “fundamental inconsistency” between the ABC Liability Exclusion and Warranty 13.5. This was highlighted by the fact that the Policy exclusion did not define “liability” and losses arising from non-compliance were excluded.

Impact on policyholders

The decision illustrates the importance of careful drafting of policy wordings to avoid ambiguity, with particular attention to the interaction of potentially overlapping insured and excluded perils. The scope of coverage may be significantly impacted by minimal changes to punctuation or connecting words.

The English Courts are likely to uphold the literal effect of contract terms even in the face of apparent inconsistency, in the absence of compelling evidence for a clear cure in respect of an obvious drafting error.

Ayo Babatunde is an Associate at Fenchurch Law