When Policies Collide – Untangling “Other Insurance” Clauses

At our recent London Symposium, Associate Abigail Smith discussed the potential challenges posed by other insurance clauses in insurance policies. The session covered:

- The genesis of these clauses;

- The types of other insurance clauses used to limit an insurer’s liability in the event of double insurance; and

- How competing other insurance clauses are interpreted, in practice.

What is double insurance?

Double insurance occurs when the same party is insured with two or more insurers in respect of the same interest on the same subject matter against the same risk. In other words, it occurs where an insured’s loss is covered under two or more separate policies. Whilst it can be a commercially prudent guard against insurer insolvency, it most often arises inadvertently (for example, where a composite policy overlaps with dedicated cover).

The common law position

Under common law, a policyholder that is double insured for its loss can claim against whichever policy or policies it chooses, in whichever order it chooses, subject to each policy’s limits. Then, to ensure the risk is fairly distributed between insurers, the paying insurer is entitled to claim a contribution from the non-paying insurer (a principle known as rateable contribution – Drake v Provident [2003]).

Industry challenges

Unfortunately, the common law position gives rise to some complicated issues.

The main issue is that, because there is no general rule or common law duty requiring a policyholder to disclose that it is double insured, unless an insurer asks the question directly, or notification of other insurance is a condition of the policy, a paying insurer may not be aware that they are entitled to claim a contribution.

Adding another layer of complexity, the limitation period for bringing a contribution claim is two years from the date that the right accrued under section 10(1) Limitation Act 1980. That date, which is likely to be the date of a judgment, settlement or arbitration award, is not necessarily when an insurer becomes aware that they are entitled to a contribution. In fact, with no duty to disclose, it is possible for limitation to expire without an insurer ever knowing that it had been entitled to a contribution.

Types of “other insurance” clauses

It was in recognising these challenges that the industry came up with a solution: other insurance clauses, which are standard clauses in insurance policies which limit an insurer’s liability in circumstances where another policy covers the same loss.

In The National Farmers Union Mutual Insurance Society Limited v HSBC Insurance (UK) Limited [2011], Gavin Kealey KC identified 3 main types of other insurance clauses, being:

- Escape Clauses – those that exclude cover altogether in the event that another policy covers the same loss.

- Excess Clauses – those that state that the policy will only respond in excess of any other insurance.

- Rateable Proportion Clauses – those that limit an insurer’s liability in proportion to the total cover available.

Abigail explored how each type of clause is interpreted, and how competing clauses interact, in practice.

Escape Clauses

Owing to the fact that Escape Clauses seek to exclude cover altogether in the event of double insurance, there was at the outset the potential for policyholders to be left without any cover at all where two or more policies each included an Escape Clause.

That issue was addressed in Weddell v Road Transport [1932], with the Court ruling that it would be unreasonable to leave a policyholder without any primary cover in circumstances where multiple policies were in place and multiple premiums had been paid. As such, where two or more policies include an Escape Clause, they will cancel each other out so that the policyholder can claim against whichever policy (or policies) it chooses (essentially reverting to the common law position).

Excess Clauses

The same question was more recently considered in Watford Community Housing v Athur J Gallagher Insurance Brokers Limited [2025], this time in respect of Excess Clauses. Ultimately, the Commercial Court held that, because Excess Clauses also seek to avoid primary liability in the event of other insurance, they cancel each other out in the same way that Escape Clauses do.

Escape Clause v Excess Clause

Whilst there’s no English authority addressing a scenario in which two or more policies include competing Escape and Excess Clauses, Australian caselaw does provide some assistance.

In Allianz Insurance Australia Ltd v Certain Underwriters at Lloyds of London [2019] the New South Wales Court of Appeal held that competing Escape and Excess Clauses would also cancel each other out on the basis that both seek to avoid primary liability in the event of double insurance – an Escape Clause seeks to avoid any liability, whilst an Excess Clause recognises only a secondary one.

The New Zealand courts, by contrast Abigail noted, have on one occasion reached the conclusion that an Escape Clause will prevail (albeit relying heavily on the insurance provisions in an underlying contract). As such, the outcome will always come down to the specific policy wording and the wider context; “there is no universal hierarchy that automatically applies.”

Rateable Proportion Clauses

The final type of other insurance clause limits an insurer’s share of the loss in proportion to the policy limit. For example:

- An insured incurred £900,000 of loss covered under two separate policies.

- Policy A with a limit of £1m, and Policy B with a limit of £2m.

- Policy A’s insurer would be liable for 1/3 of the loss (their £1m portion of the total £3m insured), which is £300,000, and Policy B’s insurer would be liable for 2/3 which is £600,000.

If Policy A contained a Rateable Proportion Clause, and Policy B was silent, Policy B’s insurer would have to pay the whole of the loss and then claim a contribution from Policy A’s insurer.

Rateable Proportion Clause v Escape / Excess Clause

Unlike Escape and Excess Clauses, Rateable Proportion Clauses acknowledge that an insurer does have a primary liability in the event of other insurance, albeit a limited one. For that reason, an Escape or Excess Clause will prevail over a Rateable Proportion Clause.

If Policy A included a Rateable Proportion Clause whilst Policy B included an Escape Clause, the effect of the Escape Clause is that there would be no double insurance and Policy A’s insurer would be liable for the loss without being entitled to claim a contribution from Policy B’s insurer.

Whilst there has been some controversy over how an Excess Clauses might compete with a Rateable Proportion Clause (Austin v Zurich [1944]), in NFU v HSBC, Gavin Kealey KC sought to clarify the position. He remarked that, as a matter of construction, an Excess Clause should prevail over a Rateable Proportion Clause because a Rateable Proportion Clause recognises that an insurer has a primary liability in the event of double insurance, whereas an Excess Clause does not.

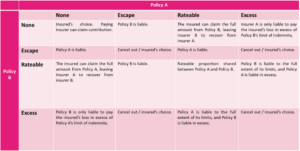

Abigail produced the table below as a starting guide for interpreting competing clauses, but was careful to note that the position will always depend on the policy wording, and the wider context.

Remaining questions

One issue that the courts are yet to address is whether, where an insured has multiple policies forming a horizontal primary layer of cover, followed by an excess layer that sits above, the entire horizontal layer must be exhausted before the excess policy responds.

The issue hasn’t arisen in caselaw to date, but Abigail remarked that it will be interesting to see how the courts approach the question when the times comes.

Key takeaways

The good news, for policyholders, is that the courts have so far refused to entertain any scenario in which an insured is left without primary cover.

That doesn’t mean, Abigail warns, that other insurance is an insurer’s problem. In circumstances where an Escape or Excess Clause prevails, an insured can be left without access to a policy that it paid a premium for, and which may well be preferable on its terms. Similarly, the disadvantage of Rateable Proportion Clauses from an insureds point of view is that the risk of insurer insolvency transfers back to the insured.

For those reasons, it is worth understanding whether there is another policy that responds to a risk and, if so, how any other insurance provisions might be interpreted.

Author

Abigail Smith, Associate

Other news

For better(ment) or for worse?

Allegations of “betterment” arise frequently in property claims, particularly where roofs, façades, cladding or other…

You may also be interested in: